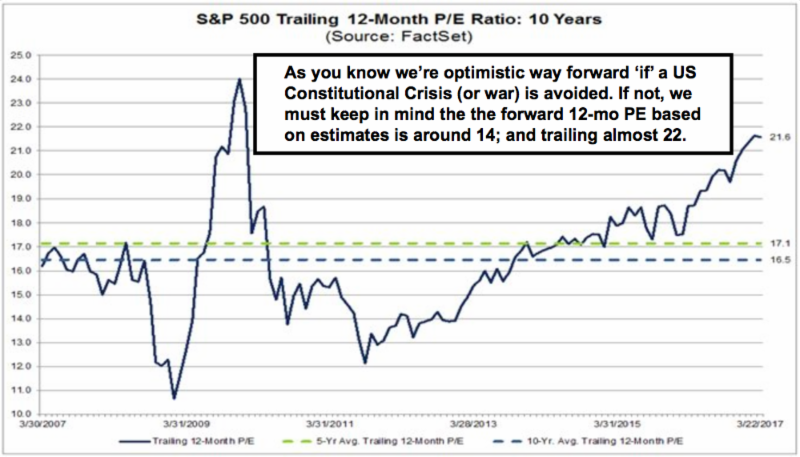

A maze of 'conspiracy theories' dominates the news background, as we enter the second quarter. These will actually expand in the very near future, as I delve into a bit in the main video. However, the other topic focuses on the Central Bank excessive dwelling on accomodative monetary policies for too long. That of course levitated the stock market previously; holding it together in a range for a couple years before the election; from which it soared.

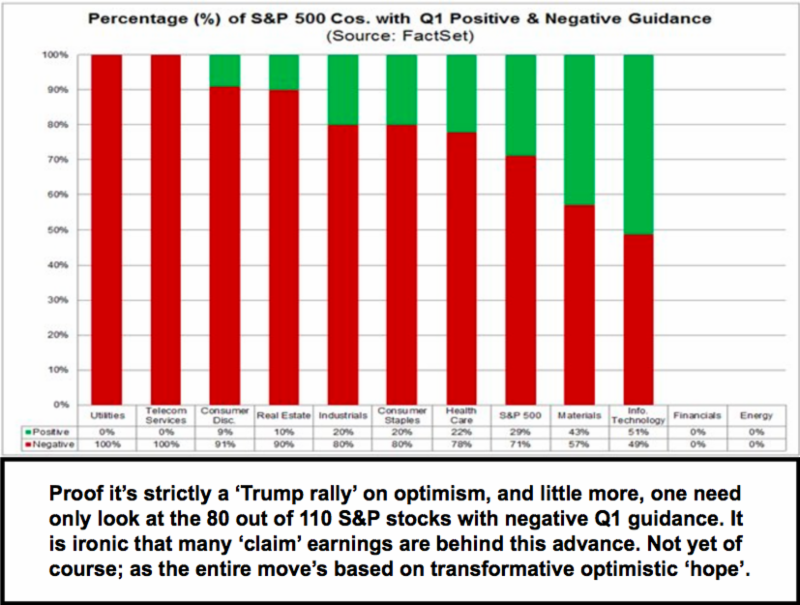

The post-Trump-win surge evolved as we continuously outlined; with minor pullbacks, and with short-sellers run in as regularly suggested probable. As we finish the first quarter with a majority of S&P component stocks issuing negative guidance (so they can beat their number in some cases; resulting I suppose in favorable reporter or pundit reactions), you're more likely to see selling into those reports, rather than buying. There are a few reasons.

One reason might be highlighted by the upcoming FOMC Minutes report; a hint provided by the NY Fed's Bill Dudley suggesting the Fed might 'roll-off' maturing paper, which means drain the balance sheet; which has put upward pressure on interest rates.

Of course the economy is not 'really' surging to any sort of prosperity for the broad society, and most of the 'hawkish' Fed commentary is engineered for the purpose of getting the U.S. off of the unacceptable emergency low rate levels, which give them essentially no maneuvering room in event of need. That also means the indirect assist to the equity market will diminish too.

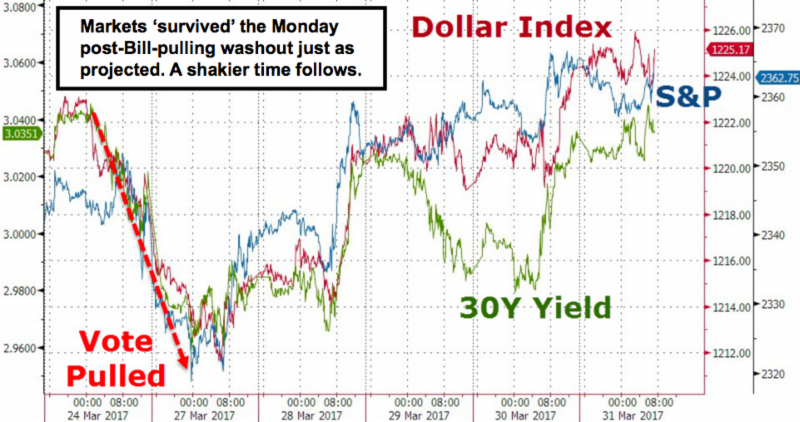

In sum, the market pattern continues evolving as outlined, with satisfactory upward performance in recent weeks, and coming off washout-Monday, in the wake of the Healthcare Bill being pulled.

Should a variation suddenly be put to a vote next week or thereafter, and if it were to pass, yes, the market would suddenly leap forward, with the idea of a new 'lease on life' for pushing forward Trump's economic initiatives.

All of this can be fascinating; with the markets overshadowed by concerns related to the ongoing investigations and so on. Looks like both sides have egg on their faces about leaks, hacking and so on; none of which inspires a great degree of confidence among our citizens.

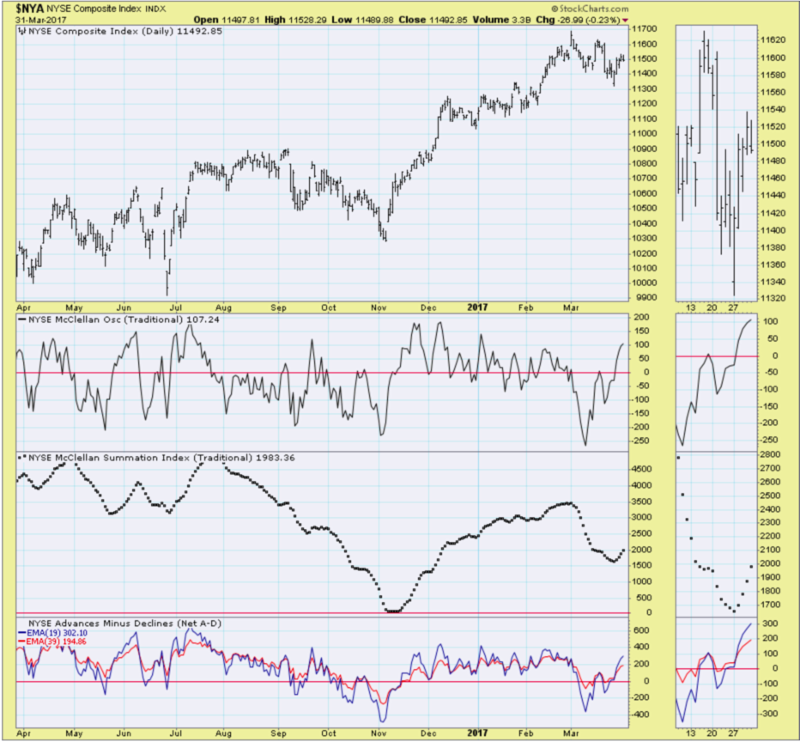

Daily action

So far the stock market has largely ignored the politics, but it is about at the point where we're either going to get some affirmation of the underlying bullish consumer and business optimism (not too much yet that's quantifiable like consumer spending or CapEx, which we don't have); or the market will (and may anyway) have a correction hitting within the April-May time-frame that I've thought likely.

The extent of decline can be mitigated by economic progress; by favorable outcomes of the U.S.-Chinese Summit in Palm Beach, or by passage of a surprise Health Bill, or some other surprise; like an announcement of when Trump gets to meet Putin.

Meanwhile, Monday may start out defensively; but not aggressively. Then I am looking for another intraweek rally; but suspect it might not have a great deal of 'punch' to it, unless we get some accompanying good news from the political side of things (and I doubt we will). The efforts that may be revealed by Clinton/Obama 'rejectionists' to undermine (or ruin) the administration, if affirmed in any way, would undoubtedly be sad, and not calm these issues. I spoke about some of this additionally just coming out in the main video, and would presume some networks will minimize it; while others like FOX jump on it. How it impacts the markets (if at all), is difficult to predict just as yet.

Comments

Log in or sign up to join the conversation.