As to a steam-rolling concept (which a prominent money manager conveyed to me this morning as his view of what's transpired); it's margin requirements at at least one or two firms that he thinks suppresses trader capacity .. and in the cases where there is little or not leverage available, may explain 'why' the shareholders of a number of small-caps (tech or otherwise with restrictions) in fact behaved poorly, regardless of their fundamental news progress (of course worse if no news or bad news; but good news didn't get much response). I hadn't given this much thought previously, as aside not advocating leveraged speculation in-general, I had commented about 'cross-asset' selling involving a series of Bitcoin / crypto breakdowns earlier this year, which subsequently did become more visible in regular equities suggesting people were selling a broader assortment of assets to meet margin (or bank borrowing) demands. |

|

Also when a stock has a 100% margin coverage requirement; many traders just won't play the ticker, or might gravitate towards Call options. And that's a partial explanation for high premiums on Calls with such restricted directives from a brokerage firm. Plus some of these stocks rally 'anyway' and that can be institutions taking advantage by 'writing' Covered Calls as income strategy. You may well see some of this during next week's April Expiration when such players will try to suppress share prices below round number with the highest open-interest; and then perhaps (if the overall market atmosphere allows) you get a fairly spirited rally. You might anyway should 'fair' progress ensue from a delayed meeting in Pakistan; on the other hand won't help if that falters. I'd rather not outline which firms have imposed the most stringent 70 to 100% margin requirements; but I note that Schwab has some tighter restrictions on several stocks than for-instance Merrill Lynch or Fidelity; probably because some big firms cater to more conservative investors than a Schwab or surely a Robinhood.. or maybe Interactive Brokers that solicits business by noting lower margin interest rates, but then fails to mention limitations on leverage. I don't want to be specific because I have not survey any of them; just pointing out a money manager believes this discrepancy among brokers contributes to the lethargic action; because some big individual traders were compelled to back-off or sell stocks because of increasingly strict margin parameters. Also he noted that these brokers make lots of money off the interest paid on such accounts by the clients (besides order-flow payments); there is incentive for brokers to normalize the margin requirements 'once' they feel conditions are a bit less risky (for the brokerage firms as trader partners; not the clients). So the implication is 'when' that inevitably occurs you get some spirited rallies, especially in stocks that remain promising, but had limited available margin. |

|

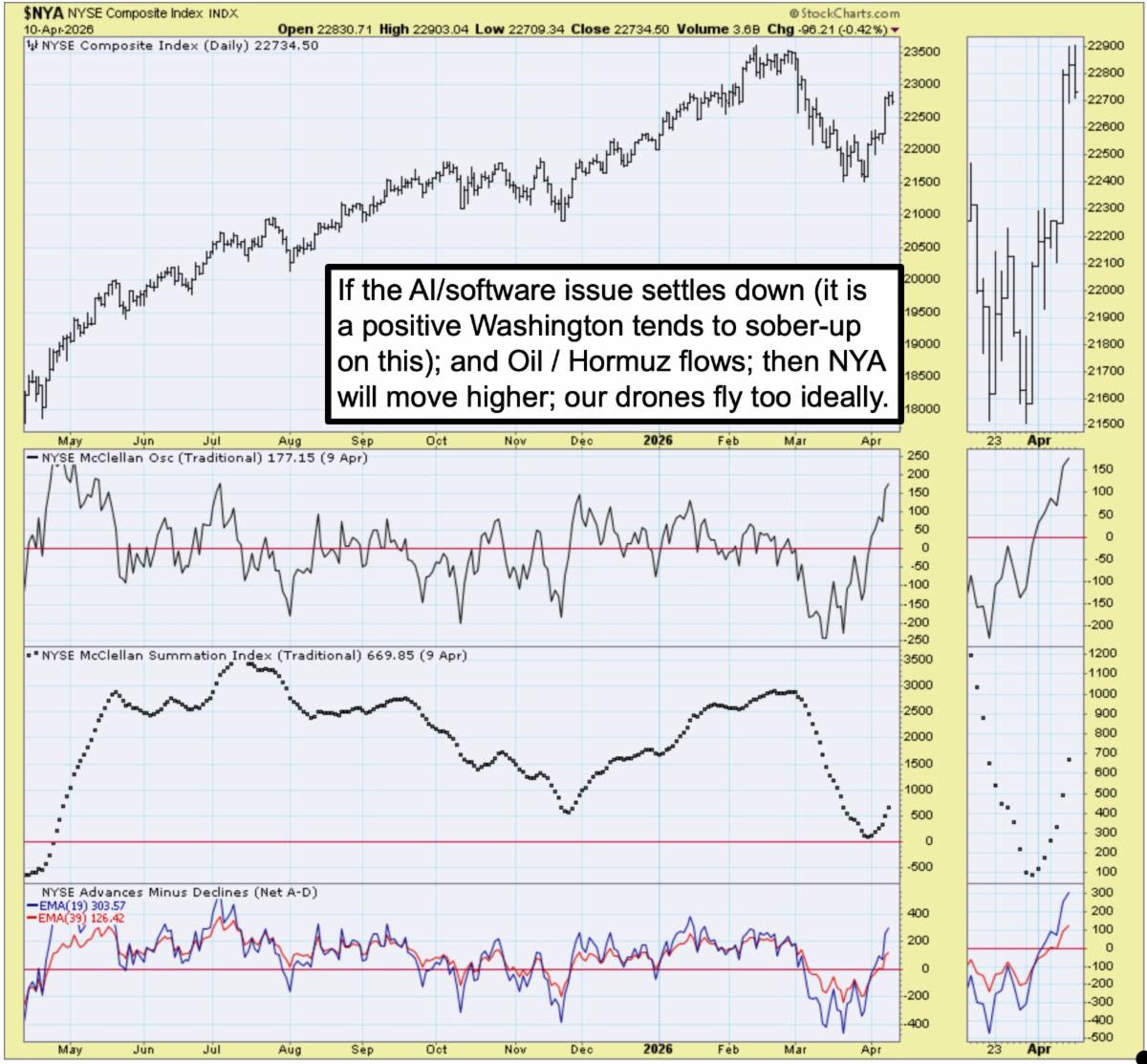

Market X-ray: aside some partial explanation provided above regarding some tighter margin requirements, most stocks remain neutral; shuffling to-and-fro based on institutional accumulation during dips; while postulating that a rally of significance will occur whether from positive macro news; and of course if contracts arrive for particular new-era tickers, and so on. And that's aside the discussion about brokerage-firm restrictions that are not industry-wide (brokers 'want' clients on margin when comfortable with it, again for purposes of the firm's income). In any event the overall S&P market holds an essentially lateral pattern after moving up and leaving a yawning gap that may or may not get filled, perhaps depending on what happens with Iran over the near-term; and longer-term worries about a 'White Collar' Ai-based crisis. Trump late Friday says 'we will have the Strait open very soon'. For now that's the key to the recent market low proving to be a pivot for Spring rally. Sure, it's not easy nor certain; but that's the challenge of investing in this 'fun' market :). |

|

Comments

Log in or sign up to join the conversation.