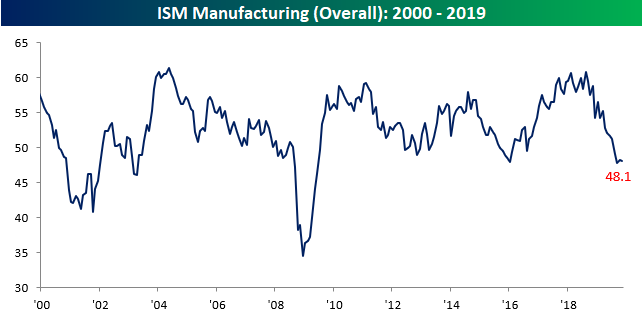

Manufacturing activity contracted more than expected last month as the ISM Manufacturing report for November came in weaker than expected. While economists were expecting the headline index to come in at a level of 49.2, the actual reading was 48.1, which was a slight decline from October’s reading of 48.3. While November’s reading didn’t mark a new short-term low for the ISM Manufacturing index, it’s not far from September’s low of 47.8.

(Click on image to enlarge)

Breadth in this month’s report was also weak. Of the report’s ten subcomponents, six declined on an m/m basis while four increased, but all but one are still in contraction territory for the fourth straight month, which is a trend we haven’t seen since late 2008/early 2009. The biggest increases this month were in Imports and Production, while Inventories showed the largest declines. Looking at the changes in each component relative to last year at this time, though, shows how quickly conditions have changed as all but one (Customer Inventories) are down on a y/y basis.

(Click on image to enlarge)

Two charts we wanted to highlight individually are Employment and Prices Paid. In the case of Employment, that component dropped to 46.6, which is still modestly above the recent low of 46.3 in September. Even still, this doesn’t bode particularly well for Friday’s employment report. More important to watch, though, will be the ISM Services report on Wednesday.

(Click on image to enlarge)

Similar to Employment, Prices Paid also turned back lower this month and is right near its recent lows. This indicator serves as a reminder that inflation readings are still showing no signs of accelerating to the upside. That coupled with the fact that the Fed has suggested on multiple occasions that it is willing to remain on hold until well after inflation rates reach or exceed their target levels indicates that any rate hikes by the FOMC are a way off.

(Click on image to enlarge)

Comments

Log in or sign up to join the conversation.