After a decade of central bank experimenting with near-zero interest rates, economists are starting to lose patience with interest rates as the main tool to guide the economy. The Bank of Canada (BoC) has exclusively relied upon interest rate adjustments to manage economic growth and inflation. For example, the drop in the world price of oil in 2014 hit the Canadian economy sufficiently hard that the BoC decided to take out an insurance policy by lowering its overnight bank rate twice in the first seven months of 2015. The BoC is now very data-dependent when it comes to future rate adjustments and, in a world of great uncertainty, it may be forced to cut rates to near zero next year.

The use of interest rates as a stimulus tool is challenged in a new research note by Steve Ambler for the prestigious C.D. Howe Institute. His argument is not new to the economics profession. Those of a certain vintage will recall that the Volker Fed in the early 1980s tried to tame inflation by controlling the money supply, that is, credit available to the banks and, ultimately, to their customers. This approach had the underpinnings of the monetarist wing of the economic profession who advocated that all that was necessary to bring inflation into line was to adjust credit within the banking system, rather than manipulating interest rates. The Volker experiment with controlling the money supply failed and he reverted to pushing interest rates to unprecedent levels (the Canadian bank rate hit 21% in 1982). Ever since central bankers have used the bank rate to modulate inflation. The one major exception has been the use of quantitative easing (QE) by the Fed, the ECB and the Bank of Japan (the BoC has never employed QE). QE is another means of expanding the money supply, and in this case, it is aimed at bringing down long -term interest rates in the expectation that lower rates will boost capital investment.

Amber advocates that the BoC should introduce QE as a way to expand the size of the money stock. In its simplest form, QE involves the central bank purchasing government securities from the banking sector, thereby increasing commercial bank cash balances. Commercial banks would then use these balances to expand lending, which, in turn, expands the broader measures of the money supply. This expansion, in turn, encourages increased spending on goods and services without necessarily having to lower interest rates---- a classic monetarist approach. As Ambler puts it:

“During the inflation-targeting era {that existing now}, “conventional” monetary policy has come to mean influencing a short-term nominal interest rate in order to influence other market interest rates at short and longer horizons and thereby influence spending. By altering spending, the amount of slack in the economy (measured by the output gap) is affected, which puts upward or downward pressure on the rate of inflation. This view of how its monetary policy works as outlined in Bank of Canada.”

The more important point that Ambler makes concerns bank lending activities in a low- interest rate world. Drawing upon Milton Friedman’s understanding of banking behavior, Ambler notes that:

“In situations where the Bank’s overnight target rate and other short-term interest rates are very low, banks could have little incentive to expand their loans…... This situation has been termed a “liquidity trap” by a number of economists, alluding to Keynes’ use of the term … “.

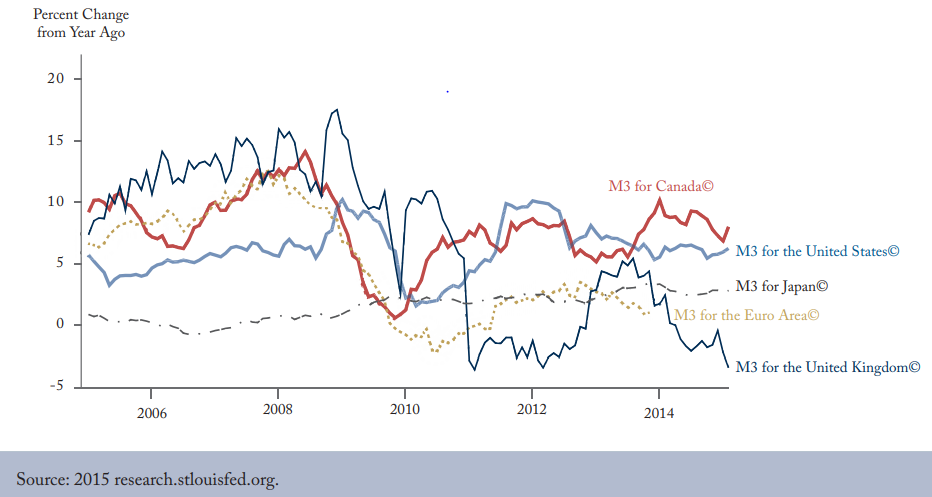

The accompanying chart confirms this warning about low-interest rates not succeeding. The broad measure of money supply (M3) have been very restrictive and has either been flat or declining in the major industrialized countries. Lowering the cost of borrowing has not created a greater demand for loans. Furthermore, the ECB experiment with negative rates has not spurred any meaningful money supply growth and, hence, no economic revival. The EU commercial banks prefer to support their reserve positions with the ECB, even when they are charged for doing so, rather than extend credit to their customers.

(Click on image to enlarge)

So, Ambler's arguments are worthy of consideration, when we consider that a decade of ultra-low rates has not performed as the conventional thinking would lead us to believe. But what still remains unresolved is, that despite central bank experimentation with QE, growth remains substandard. It may be necessary to pump up the money supply but is it sufficient to stimulate economic growth? No doubt the debate among economists will continue along these lines.

Comments

Log in or sign up to join the conversation.