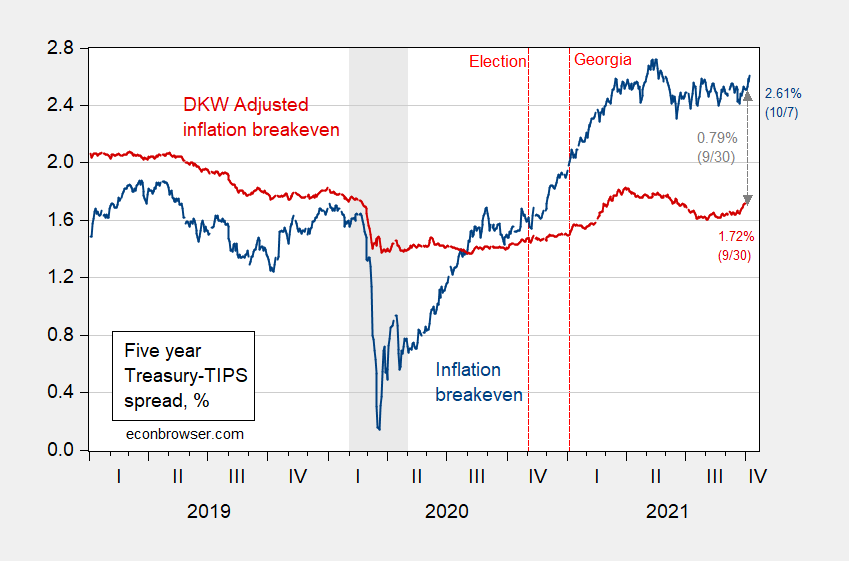

Still averaging around 1.7%, for the next five years.

As of today, the five-year inflation breakeven was 2.61%, down from 2.72% in mid-May. The estimated inflation risk and liquidity premia adjusted 5-year breakeven was 1.72% as of 9/30 (when the corresponding actual breakeven was 2.51%).

Figure 1: Five year inflation breakeven calculated as five year Treasury yield minus five year TIPS yield (blue), five year breakeven adjusted by inflation risk premium and liquidity premium per DKW (red), all in %. NBER defined recession dates shaded gray (from beginning of peak month to end of trough month). Source: FRB via FRED, Treasury, KWW following D’amico, Kim and Wei (DKW) accessed 10/7, NBER and author’s calculations.

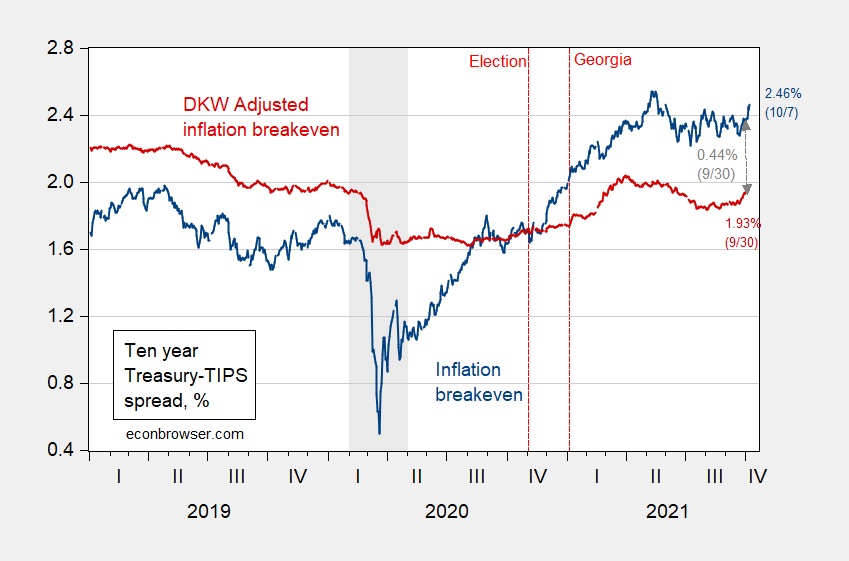

For the ten year horizon:

Figure 2: Ten year inflation breakeven calculated as ten year Treasury yield minus ten year TIPS yield (blue), ten year breakeven adjusted by inflation risk premium and liquidity premium per DKW (red), all in %. NBER defined recession dates shaded gray (from beginning of peak month to end of trough month). Source: FRB via FRED, Treasury, KWW following D’amico, Kim and Wei (DKW) accessed 10/7, NBER and author’s calculations.

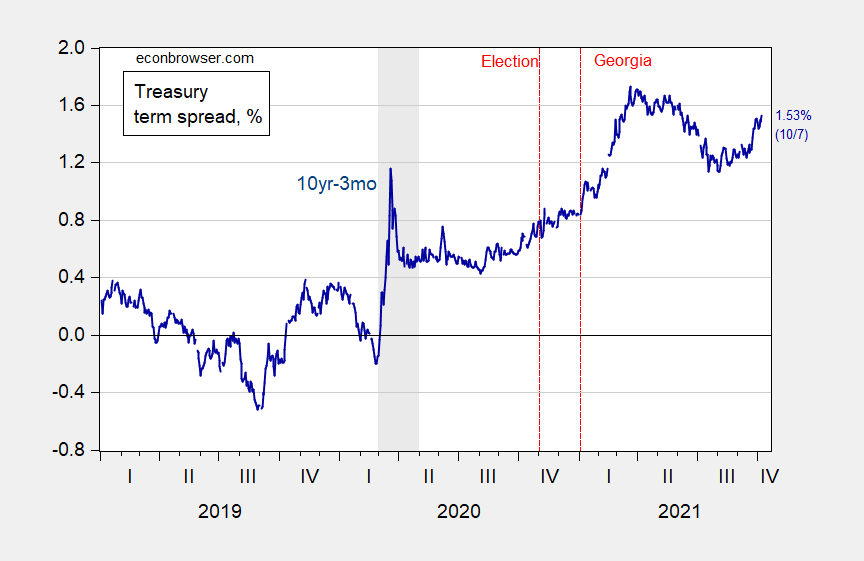

On a side note, the yield curve continues to steepen (10yr-3mo):

Figure 3: 10 year-3 month Treasury spread (blue), constant maturity yields, in %. NBER defined recession dates shaded gray (from beginning of peak month to end of trough month). Source: FRB via FRED,

Comments

Log in or sign up to join the conversation.