As the coronavirus moves into a pandemic stage and stock markets around the world slump badly, we are hearing a chorus from the trading floor interest rate cuts to stem the bleeding. Central bankers, Powell (the Fed), Lagarde (ECB) and Kuroda (BoJ) have spoken about their commitment to “standby ready” to support their respective economies. And, Fed funds futures are building in two or more rate cuts this year, in response to the anticipated slowdown in growth. However, rate cuts will have no meaningful impact. Rates are designed to influence consumers to spend and business to respond with more output. Rate cuts are not the tools designed to confront the challenge we are facing today. Rate cuts do not restore global supply chain disruptions.

Rate cuts are aimed at preventing an economic downturn by making it cheaper to borrow money, assuming that this will stimulate the economy. That is what the Fed did in the financial crisis in 2008 when it lowered rates to near zero and initiated its purchase of government bonds to encourage risk-taking by businesses and consumers. However, monetary policy works relatively slowly and it usually takes 6-9 months for a rate change to achieve its full impact. Unlike the financial crisis of 2008, the Federal Reserve and other central banks are not the cavalries just over the next hill coming to rescue of the besieged. Consider how this supply shock is taking its toll:

- Workers are suddenly told to stay home and production comes to a halt;

- business and personal travel grinds to a trickle as businesses forbid any non-essential travel;

- large entertainment and sporting events are held without fans present;

- the streets are barren of normal traffic; and,

- no longer is business as usual.

In China, the economy essentially just froze up as hundreds of millions of its citizens were quarantined.

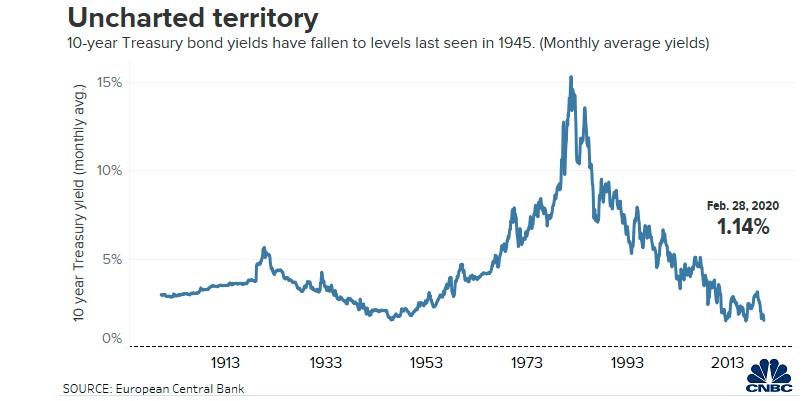

So, now the primary concern is the disruption of the global supply chain, originating in China, South Korea, and Japan, and its impact on world trade and the U.S. economy. It is hard not to conclude the pandemic will push the U.S. economy into a recession later this year. Signs are already apparent as the entire U.S. yield curve has collapsed and long-term rates have already blown by historic lows. The marketplace is already doing what it can by pushing long term rates closer to zero. It is not just a flight to safety, but more importantly, there is a realization that recession and disinflation are coming our way.

The disruption in the global supply changes has prompted numerous multinational corporations to lower sales and profit forecasts and this process of re-adjustment is not over yet. The corporate sector is highly vulnerable, owing $13.5 trillion in debt at the end of 2019, an all-time high. Debt-laden companies need to keep up with payments all the while supply is disrupted and work stoppages threaten default. Rising corporate defaults pose the greatest systematic threat.

What can the monetary authorities do? Central banks need to make sure the financial system has adequate liquidity to help consumers and businesses weather these supply disruptions. They must not, however, provide liquidity that finds its way into the financial markets so stock market investors can return to the party atmosphere prior to the outbreak of the coronavirus. Supplying liquidity to the financial markets does nothing to re-open factories or re-institute transportation and travel services. The one positive aspect coming out of this tragic public health threat is the prospect that the equity markets will be re-priced to reflect the realities of future profits growth.

Comments

Log in or sign up to join the conversation.