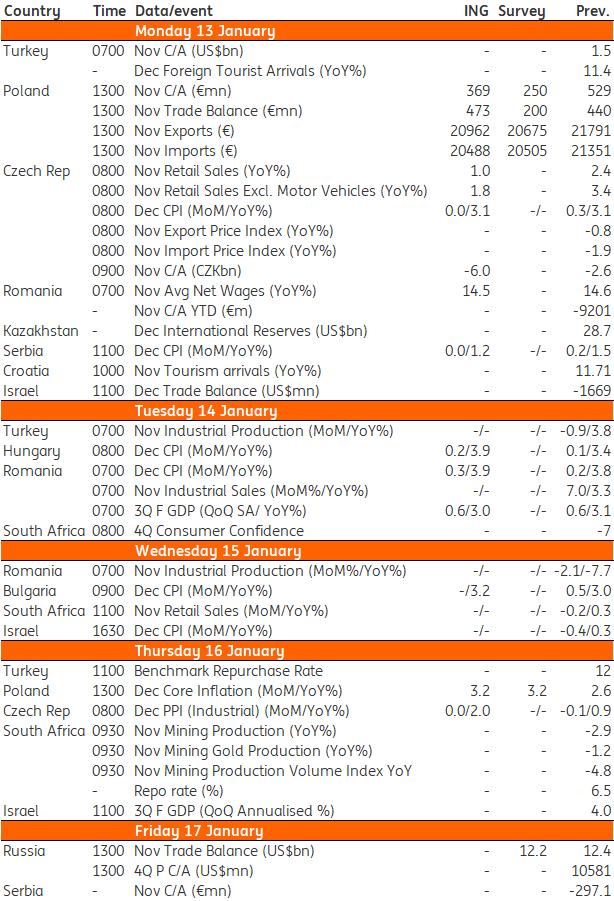

A busy week in EMEA. The focus will be on inflation numbers, which are expected to follow an upward trend in December as a result of higher energy prices, among other factors.

Hungary: CPI to jump on the back of energy prices

Hungary will join the trend in terms of what we’ve seen lately in the main inflation readings across Europe.

We expect headline CPI to jump to 3.9% year on year, matching the highest level seen in 2019. The main reason behind the significant acceleration is the change in energy prices, namely the combination of the recent rise and the lowering base from a year ago. In the meantime, the non-volatile elements might show only moderate inflation, especially the durables, dragging the core CPI reading a touch below 4% again. If our forecast proves to be correct, it would also mean that incoming data is lower than the central bank’s forecast, so there won’t be any reason to even start thinking about a hawkish turn in the near future.

Turkey: Benchmark rate on hold but risks are tilted to the downside

The decline in (ex-post) real interest rate with large rate reductions and the recent rise in inflation entails a risk to TRY stability while geopolitical developments are likely to make the central bank more cautious in the near term. But risks are on the downside, depending on the performance of the TRY, further easing cannot be ruled out given the central bank’s ongoing easing bias.

Poland: Final CPI data to explain the rise in core inflation

The final CPI release for December (likely 3.4%YoY) should shed more light on the drivers of a surprising core inflation increase from 2.6% to 3.2% YoY. Still, even in case of a demand-driven shock related to the minimum wage hike, we expect the central bank to continue communicating an unwillingness to change rates.

Czech inflation to follow the upward trend

December inflation will be the most-watched release after the previous print surprised on the upside and exceeded the 3% upper tolerance band of the inflation target. So far the December CPIs that have been released in the region have also accelerated above expectations. The main uncertainty is concentrated in food prices again, which was the main factor behind the November CPI acceleration.

However, some preliminary figures suggest that food prices might grow just slightly in December (+0.4% month on month), while fuel prices fell by 0.5%. As such, we expect stagnation of CPI at 3.1%. Retail sales will be affected by the working day bias, so unadjusted figures will be weaker compared to the year-to-day average growth, though we expect some slowdown beyond the calendar effect due to weaker consumer confidence and Black-Friday timing, which partially shifted to December.

EMEA and Latam Economic Calendar

(Click on image to enlarge)

Source: ING, Bloomberg

Comments

Log in or sign up to join the conversation.