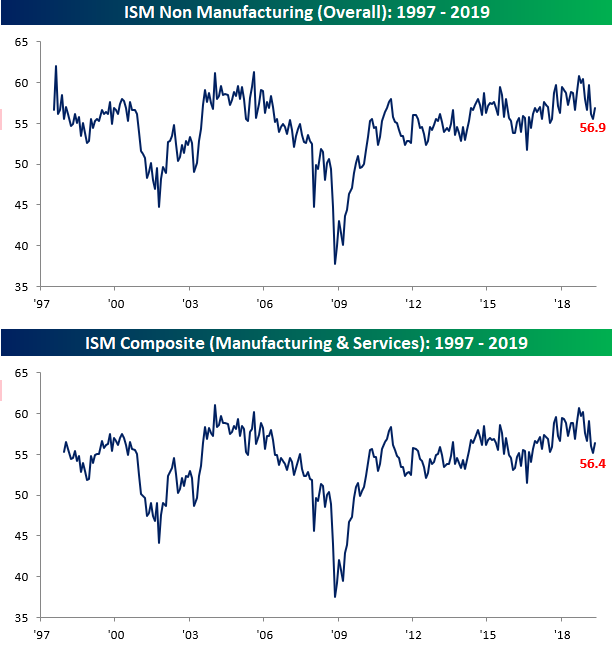

After the weakest ADP Private Payrolls report (in terms of the actual reading and relative to expectations) in close to a decade earlier this morning, investor anxiety heading into the ISM Services report for May was understandably high. While economists were expecting the headline index to decline slightly from 55.5 down to 55.4, it actually saw a modest increase rising to 56.9. On a combined basis and accounting for each sector’s share of the overall economy, the May ISM Composite PMI rose from 55.2 up to 56.4.

(Click on image to enlarge)

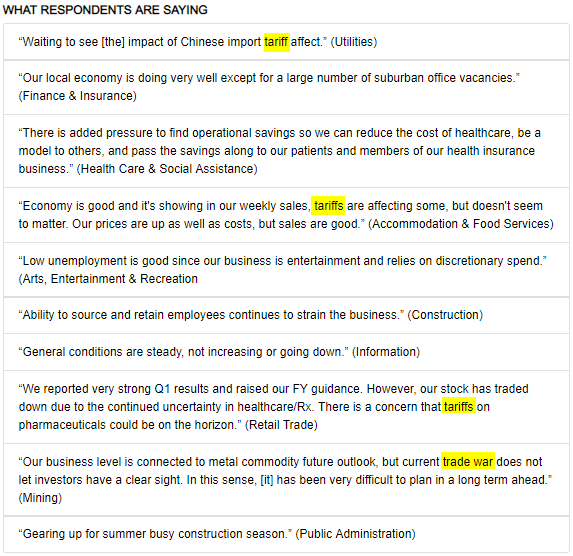

As you might recall, tariffs were a major issue in the commentary section of the ISM Manufacturing report, and while they were also an issue in the commentary section of the Services report, it wasn’t as prevalent. As shown in the graphic below, the issue only showed up in four of the ten comments, and in one of them it was saying that the issue of tariffs “doesn’t seem to matter.”

(Click on image to enlarge)

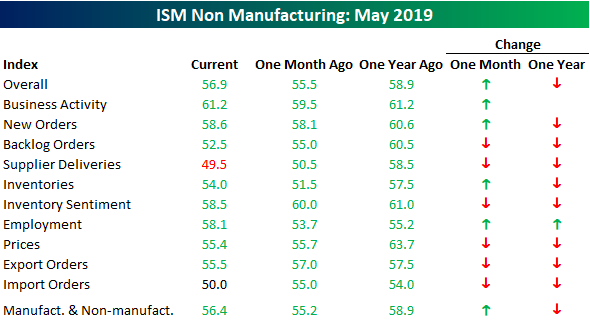

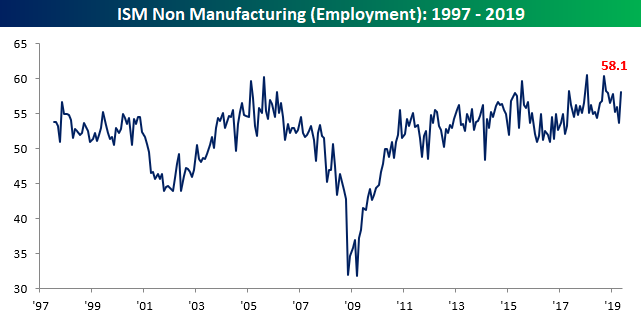

While the headline reading of the ISM Services report showed an m/m increase, breadth in this month’s report wasn’t particularly strong. Of the index’s ten subcomponents, six showed m/m declines in May and eight showed y/y declines. One positive outlier, though, was Employment, which increased from 53.7 up to 58.1. It figures that on the same day we saw the weakest ADP Private Payrolls report in nearly a decade, that we would also see the largest m/m increase in the Employment component of the ISM Services report in two years. Really clears things up!

(Click on image to enlarge)

(Click on image to enlarge)

Comments

Log in or sign up to join the conversation.