By John Benjamin

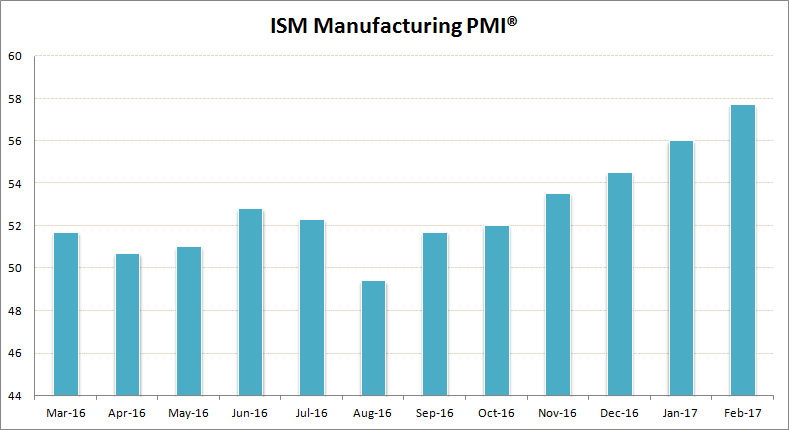

If investors were looking for another reason to be bullish on the U.S. dollar and the Fed rate hike, then last week’s ISM manufacturing data was another reason. The Institute for Supply Management reported last Wednesday that the headline PMI index rose to the highest levels since August 2014 at 57.7 in February, this was an increase from January’s 56.0 print. February’s data also showed that the manufacturing PMI rose for the sixth consecutive month, adding further to the optimism.

Looking into the details, data showed that new orders increased to 65.1 while production jumped to 62.9 in February, up from 60.4 and 61.4 respectively in January. The new orders component was incidentally the largest contributing factor to the higher PMI reading for February. The new orders index at 65.1 was also the highest on record since 2009 when the U.S. economy was seen coming out of recession.

There was, however, some downside as the prices paid index fell to 68.0 in the reporting month, down from 69.0 in January. The employment index was also seen weaker, falling to 54.2 in February from 56.1 the month before.

February ISM manufacturing PMI

With the exception of the above to weak readings on the sub-indexes, overall data continued to point towards expansion in the manufacturing sector which continues to be promising for the economy. The data spurred optimistic comments as the turnaround has been remarkable. It was only in August last year (2015) that the ISM manufacturing PMI was treading the contraction mode of readings below 50 and the sentiment saw a rapid turn-around since October.

The February ISM manufacturing data showed a broad based strength with 17 out of the 18 sectors reporting growth over the last month. This was a significant pick up from just 12 sectors that reported growth previously in January. Most of the upside activity came from domestic demand, but the export orders index showed that there was demand from abroad as well. The index (export orders) was seen rising to 55.0.

Despite strong signals, GDP outlook warrants caution

The strong figures for February, following an increase from January, is pushing investors to a hawkish outlook on the GDP during the first quarter of the year, although the enthusiasm is still early. But it does confirm the fact that the U.S. manufacturing sector had jumped to firmer ground since December last year. However, with the exception of the ISM manufacturing data, other gauges of the economy remained rather flat with real consumption seen falling 0.3% on a monthly basis and construction spending falling by 1% which warrants caution on the optimism.

In the near term, investors will be looking to this Friday’s jobs report, and in this aspect, the weaker reading on the employment index is likely to raise some eyebrows. However, the data remains supportive of another 160k+ job growth print expected for February. Manufacturing payrolls were consistent, rising at a pace of 15,000 on a monthly basis.

On Friday, the ISM non-manufacturing PMI was seen rising to 57.6, easily beating the market expectations of 56.5, signaling continued expansion in the sector. The business activity index rose to 63.6 from 60.3 in January while new orders index rose to 612 from 58.6 previously.

The data combined showed that there were signs of the economy chugging ahead in full steam. The Fed Chair, Janet Yellen in her speech on Friday said that the Fed was not falling behind the curve but cautioned the markets to be prepared for another rate hike, indicating that the next rate hike could come in March and the payrolls unlikely to be an obstacle.

While the Fed has so far maintained a hawkish view on the March FOMC meeting, a lot will be hanging on the outcome of this Friday’s jobs report. As long as the February payrolls don't disappoint by a big margin, the likelihood for the Fed hiking interest rates in March 2017 remains very strong.

Comments

Log in or sign up to join the conversation.