Coming in on Tuesday morning, investors were expecting to sift through earnings from the largest banks and the CPI data. Instead, IBM stunned investors by pre-releasing its earnings 8 days in advance. Its earnings were much weaker than expected, with revenue well below expectations and EPS declining 2% year over year. As shown below, IBM fell by nearly 25% in pre-market trading.

Its CEO, Arvind Krishna, was blunt in his assessment of the quarter, stating, “This quarter we faltered.”

Beyond IBM’s earnings-specific details, they had an industry-wide message with potentially far-reaching implications for other companies. Specifically, IBM said clients shifted:

their quarterly capex spend toward servers, storage, and memory purchases to secure supply-constrained infrastructure ahead of expected price increases, adding it did not anticipate the magnitude of the capex reprioritization.

Per IBM, enterprises are now hoarding inventory to front-run the surge in memory prices and some hardware devices. Such behavior is typical shortage psychology, and it is self-reinforcing: panic buying tightens supply further, which raises prices further, which triggers more panic buying.

The implications of these actions benefit some companies to the detriment of others. Memory and hardware suppliers like Micron and SanDisk are seeing a surge in demand from the industry. However, a pull-forward today often becomes an air pocket tomorrow. Thus, earnings over the next few years may remain unaffected in aggregate, but the timing may be significantly altered. Meanwhile, IT budgets at large enterprises are largely fixed, so every dollar diverted toward memory and scarce hardware is a dollar taken from software and consulting, precisely IBM’s core business.

What To Watch Today

Earnings

Economy

Fed Speakers

Chair Kevin Warsh delivers day two of the semiannual monetary policy testimony, before the Senate Banking Committee at 10:00 a.m. ET, following Tuesday’s House appearance. The Fed is not yet in its pre-FOMC blackout, so his tone on the cooler June CPI and sticky PPI is the read to watch.

Market Trading Update

Yesterday, Michael walked through the KOSPI bubble and the concentration risk hiding inside a country index. Today I want to read the other tape that mattered: big bank earnings kicked off the season, and as I argued in this past weekend’s Bull Bear Report, the number that forecasts the economy isn’t the headline beat. It’s the credit book.

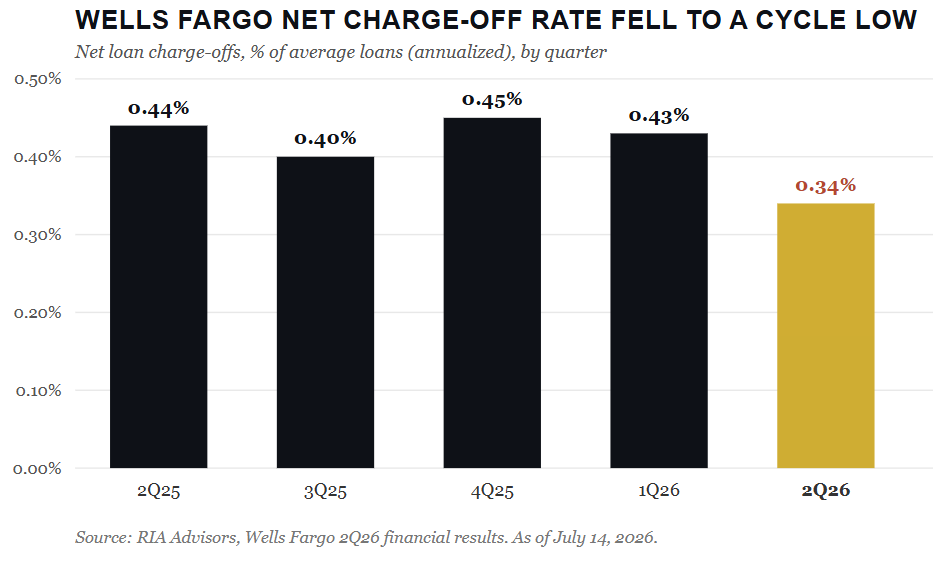

So did the four tells I told you to watch actually trip? Not yet. Wells Fargo posted the cleanest read of the group. Net charge-offs fell to $876 million, just 0.34% of average loans, down from 0.44% a year ago, as consumer losses dropped to 74 basis points due to lower auto and card write-offs. Deposits grew 10%. New card accounts jumped 46%. That is not a household balance sheet cracking.

JPMorgan told the same story. Its Card Services charge-off rate printed 3.34%, right on management’s roughly 3.4% guide, and the consumer bank’s reserves were flat. The $149 million reserve build Jamie Dimon’s team did take landed in the WHOLESALE book, not the consumer. Firmwide charge-offs actually fell $44 million from a year ago. Citi’s card delinquencies sit near 2.3%, the low end of the peer group. Read the footnotes, and the consumer passed this test.

Here’s the catch, which is worth paying close attention to. These beats didn’t come from Main Street. They came from the trading floor. JPMorgan’s equity-markets revenue exploded 86%, Citi’s equities desk rose 45%, and investment-banking fees ran 30% higher across the group. The bank bulls, Mike Mayo among them, will tell you the franchises have never been better capitalized. Fine. The consumer held, but he didn’t drive the quarter. The deal desk did.

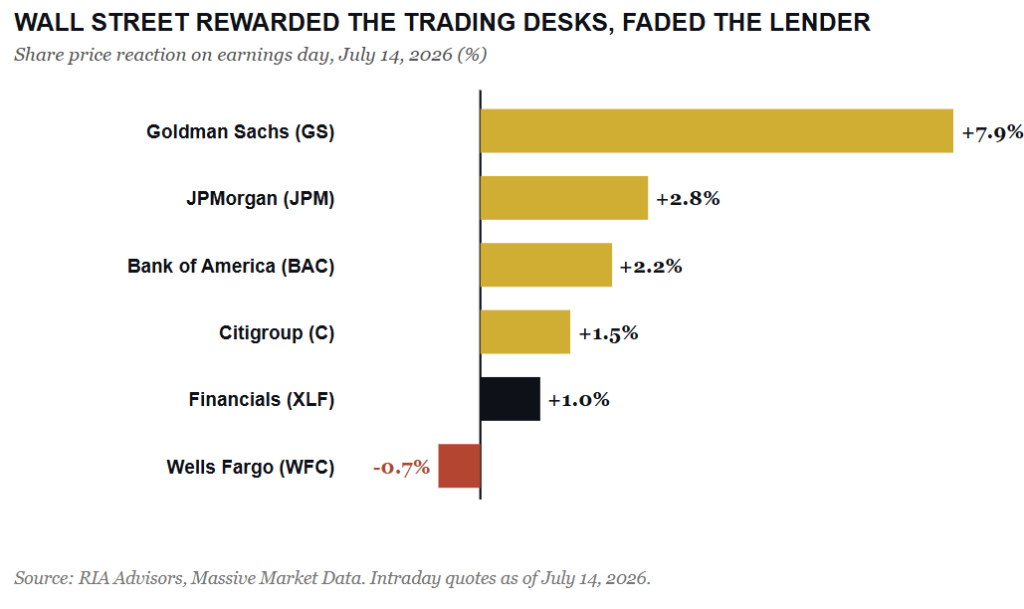

The tape sniffed that out. Goldman ripped 7.9% on its capital-markets haul, JPMorgan added 2.8%, and financials (XLF) led the day. But Wells Fargo, the purest lender in the bunch, slipped 0.7% on a clean beat. That’s a sell-the-news fade on the one name most tied to the household, and it tells you how much good news is already priced into a group our own work flags as overbought.

The consumer earned the soft-landing benefit of the doubt for now. But the one thing nobody could verify this week is the private-credit and nonbank-lending exposure buried in these balance sheets, and that’s the reserve line I’ll read first next quarter. Bank the strength in the market, but don’t chase it.

CPI Surprises

June’s CPI report delivered the biggest downside surprise in years as the oil disinflation trade hit the data. Headline CPI fell 0.4% in June, versus forecasts of 0.0%. As a result, the annual rate fell sharply from 4.2% to 3.5%. The monthly decline was the largest since April 2020. Core CPI, excluding food and energy, was flat on the month against expectations for a 0.2% rise, pulling the annual core rate down to 2.6% from 2.9%. Core goods declined for the second straight month, down 0.09%; housing was up just 0.12%; and core services ex-housing was -0.2%, the lowest in four years. The graph below shows that the share of CPI components rising above the Fed’s 2% goal is 59.2%, the lowest since inflation started rising in 2021.

Energy prices fell 5.7% after rising 3.9% in May, with gasoline prices down 9.7% and fuel oil down 9.2%. The data confirms that the BLS’s three-week measurement lag finally caught up with the oil decline from $110 to the high $60s.

The Fed’s newly hawkish tilt is likely to remain intact despite today’s soft headline. A July hike is probably off the table, but September will likely keep rate-hike odds alive.

JPMorgan and Bank of America: Trading Profits Take Earnings Higher

JPMorgan (JPM) delivered a strong earnings report Tuesday morning. Revenue of $58.02 billion easily beat estimates by 13%, and its GAAP EPS of $7.70 crushed the $5.85 consensus. There are caveats, however. Its earnings jumped 41% to $21.2 billion, but excluding $5.6 billion in non-recurring one-time gains, growth was a more modest 13%. The standout line item was its trading departments. Equities revenue surged 86% to $6 billion, $2.11 billion above expectations. This is a payoff from the volatility markets experienced throughout the quarter, increased speculative retail trading behaviors, and the SpaceX IPO. JPM’s net interest income slightly missed estimates of $25.65 billion, though it still grew 9.9% year over year.

Bank of America’s (BAC) earnings were not as strong, but it, too, had impressive trading revenue. Net interest income came in at $16.2 billion, up 9%, driven by global markets activity and higher loan and deposit balances. It matched Wall Street’s consensus.

The macro takeaway for investors is that second-quarter profits were bolstered by trading activity. Trading revenues and earnings are highly volatile and less dependable than the core banking services. To wit, net interest income, a bank’s core earnings metric, suggests that the two banks’ lending business is stable rather than rapidly accelerating. That helps explain the lackluster price activity, as we share below.

Tweet of the Day

Comments

Log in or sign up to join the conversation.