While it may not rhyme quite as well as “Sell in May and Go Away”, sell in April and go away makes a point about the dominant force in today's global financial markets: the investment professional.

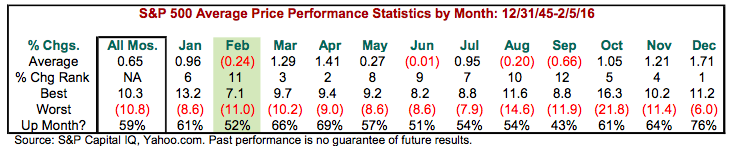

Since the global financial markets are dominated by professional investors, each trying to gain an edge over the other without going too far so as to endanger their careers, a certain amount of “front running” the seasonal tendency of the equity markets seems a likely outcome. Take, for example, past February.

History tells us that February is a month when stocks do less well than March. Yet, just two months ago stocks conducted a rather strong recovery, which one could argue was a result of many factors, including professional investors seeking to get a jump on matters in the more historically favorable month of March.

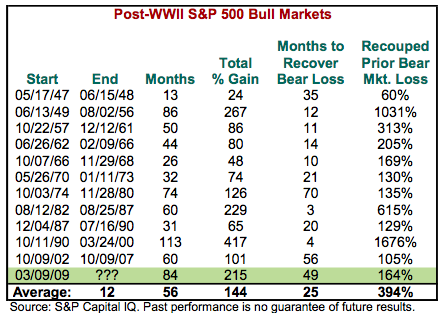

From a larger trend perspective, US equities (by far the single best performing major market in the world) are already very long in the tooth in bull market years, as the accompanying table above shows.

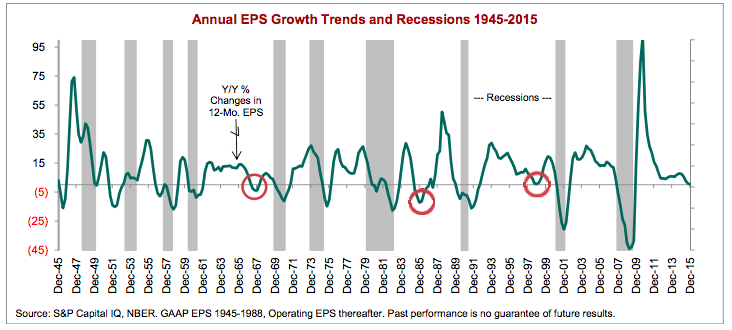

Moreover, with a profits recession underway and history showing that profits recessions often (but not always) precede or coincide with an actual recession, the investing climate is extra ripe for professional investors seeking to find a way to produce positive results whenever they can.

Investment Strategy Implications

Global financial markets are dominated by professional investors whose wants and needs go far beyond, merely trying to make money for their clients1. This reality needs to be taken into account when seeking to make investment decisions. One factor is knowing investment and economic history to help understand why professional investors might do what they do. This includes the seasonal factors via Wall Street axioms like “Don’t fight the Fed” and “Sell in May and Go Away”. If we all know these heuristics, then using them to exploit the tendencies is a useful exercise. Or as John Maynard Keynes once said when describing the stock market in beauty contest terms: "It is not a case of choosing those [faces] that, to the best of one's judgment, are really the prettiest, nor even those that average opinion genuinely thinks the prettiest. We have reached the third degree where we devote our intelligences to anticipating what average opinion expects the average opinion to be.”

***

1 A point I made in my book, “Sectors and Styles”, in which I describe the behavioral science need of self preservation in the story form of “keeping my house in Greenwich”.

Comments

Log in or sign up to join the conversation.