.jpg")

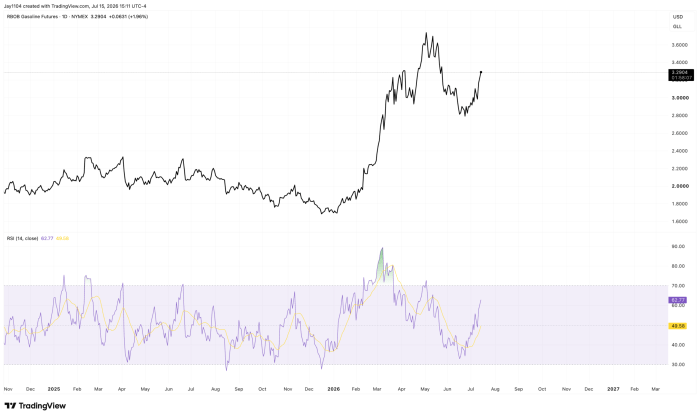

To no surprise, the June PPI reading also came in below expectations. The problem with both the CPI and PPI reports is that gasoline prices are rising, so the June CPI and PPI readings may not matter much if that trend continues. With RBOB gasoline back around $3.30, I believe inflation is likely to turn higher again in July.

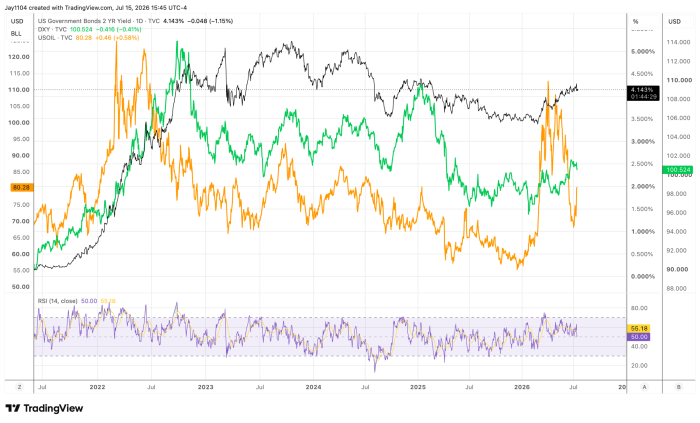

Still, rates fell, and the dollar weakened, as markets tend to respond. One month of data will not determine whether there has been a material shift in policy-rate expectations. In his Senate testimony today, Kevin Warsh sounded no less hawkish than he has in the past and remained consistent in expressing his views. I do not see how inflation can be brought down without maintaining a restrictive monetary policy. Cutting rates certainly would not accomplish that at this point.

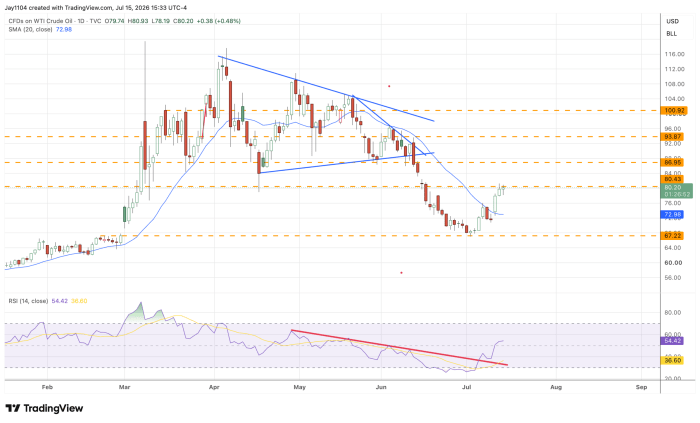

Oil, on the other hand, has found support at the gap created in early March. It has moved above its 20-day moving average and broken its RSI downtrend. Oil prices could therefore move higher from current levels, break through resistance at $80, and begin moving toward the $87 region.

If oil moves higher, interest rates and the dollar may follow. The three have historically exhibited a strong relationship, with higher oil prices adding to inflationary pressures and, in turn, supporting tighter monetary policy.

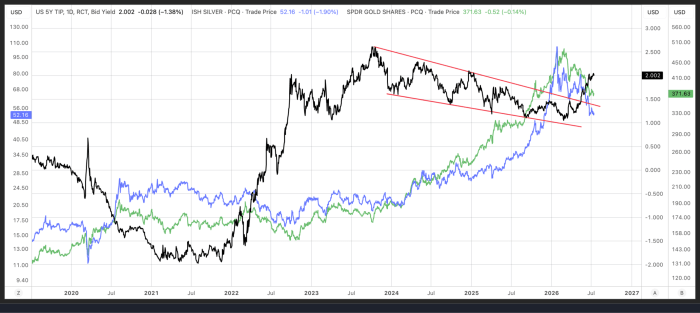

In the meantime, the 5-year real yield rose to 2% today, marking the first time in quite a while it has reached that level. Looking closely, gold and silver peaked around the same time the 5-year real yield bottomed. The further real yields rise, the more likely it is that both metals will fall.

Comments

Log in or sign up to join the conversation.