Fed Chair Kevin Warsh used his first major public appearance, a panel at the ECB’s annual forum in Portugal, to formally bury one of the Fed’s most relied-upon tools of the last 25 years: forward guidance. Warsh could not be more direct about his opinion of forward guidance. To wit, when the moderator repeatedly pressed for guidance on how the Fed may adjust monetary policy, Warsh rebutted:

“You’re back to forward guidance. I’m going to disabuse you of trying to extract that. No forward guidance, no forward guidance.”

Interestingly, he was not alone. ECB President Christine Lagarde, Bank of England Governor Andrew Bailey, and Bank of Canada Governor Tiff Macklem all expressed similar reservations about continuing with forward guidance. Lagarde stated that her “one regret” was feeling “bound and compelled” by forward guidance in the past.

Monetary policy is at a crossroads, with Fed officials mixed over next steps. As we learned at the last meeting, some Fed members are on hold, some are leaning toward a rate hike, and one would prefer to cut rates. Thus, Warsh has neither the votes nor the inclination to ease. That said, he stressed his inflation commitment plainly:

We’re going to deliver price stability in the US.

Beyond his stern messaging against forward guidance, his discussion on productivity was interesting. Warsh noted that AI-driven productivity gains over the past four quarters give him reason for optimism, stopping well short of a promise but leaving the door open to cuts if that trend continues. To wit:

But if the last four quarters are an indication… there’s reason to be optimistic now.”

The takeaway from his first speech is clear. Warsh will not telegraph his next move. Investors who relied on speeches, Fed dot plots, and the FOMC press conference for signals on how to position ahead of rate decisions are operating in a new regime. Going forward, the markets will help lead the Fed, not the other way around.

What To Watch Today

Earnings

No notable earnings today.

Economy

Market Trading Update

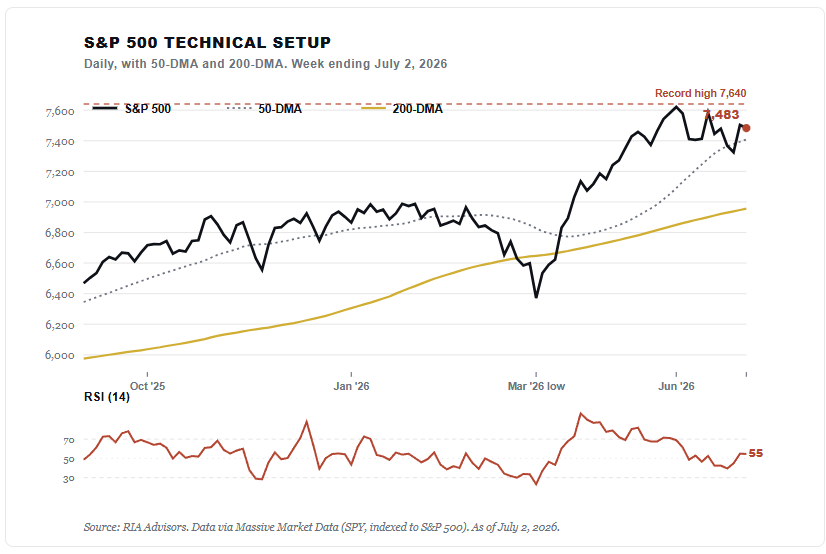

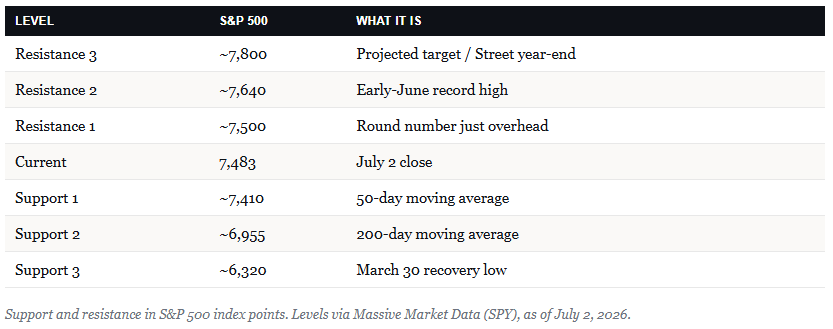

The S&P 500 heads into this week in a strong technical position, though stretched in spots. At roughly 7,483, the index sits about 2% below its early-June record near 7,640. It trades above its 50-day moving average around 7,410 and well above its 200-day average near 6,955. The trend is up, plainly.

Momentum is constructive without being extreme. The 14-day RSI reads about 55, comfortably off the overbought levels it hit in April when the recovery was at full throttle. That leaves room to run. The rally off the March 30 low, roughly 6,300 on the index, has been one of the sharpest in years. Even so, the index is not flashing the momentum exhaustion that usually precedes a real top.

The more interesting action is beneath the surface. Leadership is changing hands. For months, the tape rewarded semiconductor stocks and punished mega-cap spenders. This week began to reverse. Apple, Alphabet, Meta, and Microsoft all rose while the chip complex sold off, with the SOXX down 4% and several memory names off 8% or more. That is the post-quarter-end un-rebalancing we wrote about, and it is now showing up in the price.

We are positioned for it. Last Wednesday, our Sector and Factor Rotation model shifted from a value tilt toward growth, adding mega-cap exposure on its recent weakness and reducing exposure to overbought value stocks. Overall, our net equity exposure barely changed. We are not calling an all-clear, but we will continue to follow the model.

Volatility stayed calm through it all. The VIX finished the week near 17, a level that reads as complacency rather than fear, and one worth respecting when everyone looks this comfortable. Breadth has quietly broadened, too. Energy, industrials, and financials have carried real weight in the recovery, so this is no longer a market propped up by a handful of names.

From here, watch the levels. A close above the June record near 7,640 would confirm the breakout and open room toward the 7,800 area. On the downside, the 50-day near 7,410 is the first line to hold. Lose it, and the 200-day near 6,955 becomes the line that matters. For now, buyers keep showing up on dips, and the burden of proof stays with the bears.

The Week Ahead

The FOMC minutes from the Fed’s June 17 meeting will be released on Wednesday. The notes will give investors their first detailed look at how hawkish the internal debate actually was. Was the committee unanimous in what the media perceived as a hawkish outlook, or fractured on the path forward?

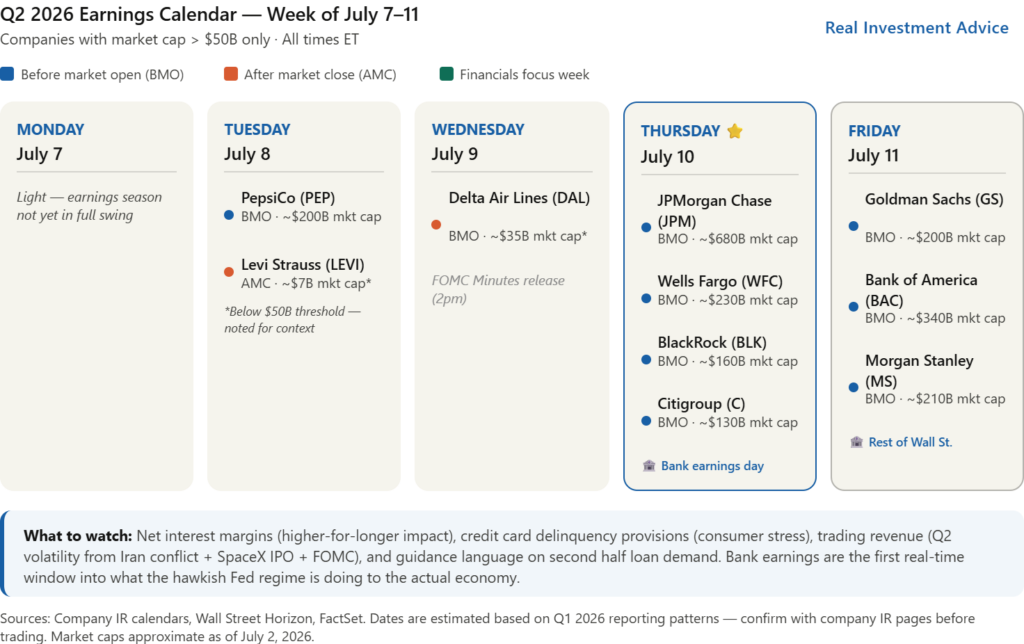

The earnings calendar, shown below, is relatively quiet. Q2 earnings season peaks in the second and third full weeks of July, with the busiest reporting period expected around July 14-18. Most hyperscalers, along with many of the largest technology companies, report closer to month-end. The early reporters this week are primarily financials, including JPMorgan, Wells Fargo, and Citigroup. The bank’s net interest margin trends will tell us what higher rates-for-longer have done to lending profitability, which impacts credit availability and financial conditions. Further, credit loss provisions signal whether the consumer stress we’ve been tracking in delinquency data and from comments from some retail outlets is accelerating,

The Employment Situation

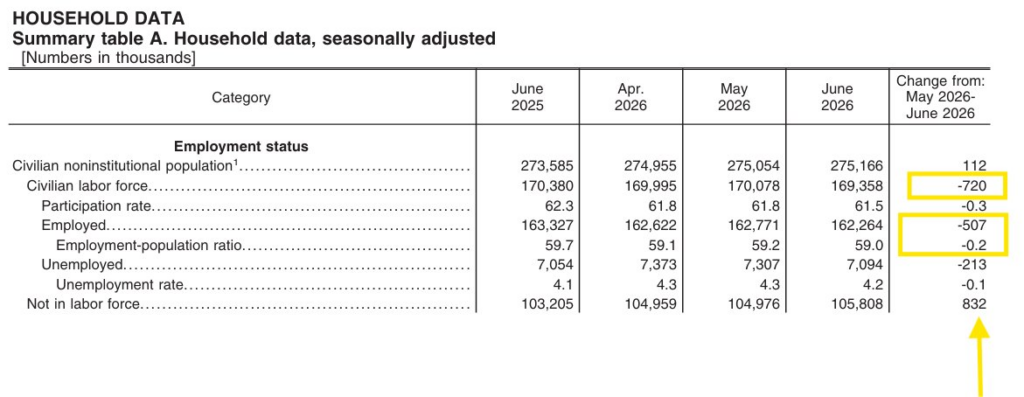

The labor market added 57k jobs last month, about half of what was expected. Moreover, it revised May’s 172k to 129k and April’s 31k lower. The unemployment rate ticked lower but for the wrong reason. As we highlight below, the participation rate fell by 0.3% because the labor force declined by 720k jobs.

The data points to a tepid jobs market. While better than we saw earlier in the year, it, on its own merits, doesn’t warrant Fed concern about higher wages feeding inflation. The report likely provides some comfort to many Fed members who may be on the fence about hiking rates.

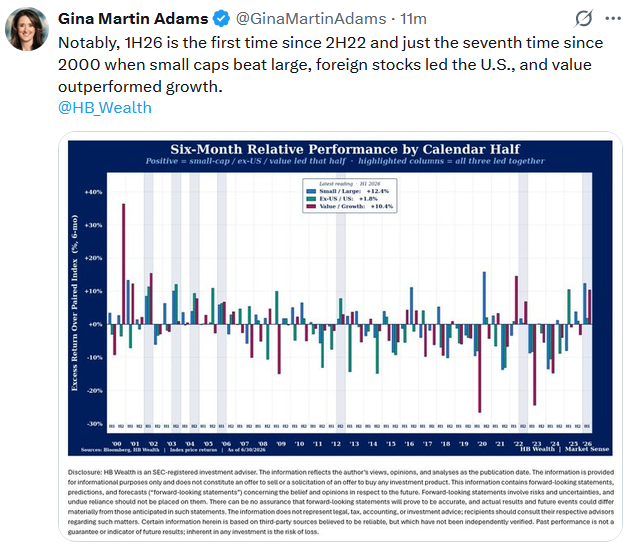

Tweet of the Day

Comments

Log in or sign up to join the conversation.