The Fed is clearly more hawkish than they were at the last meeting. Accordingly, with the Fed Funds market now pricing in two rate hikes by year’s end, we should be armed with data showing how the first Fed Funds rate hike in a cycle is processed by the equity markets. Moreover, with higher rates being forecasted, how could a flattening yield curve impact stocks and the economy?

History doesn’t offer a definitive answer. The initial instinct of many investors is to sell, as we witnessed right after Wednesday’s FOMC meeting. The reaction is reasonable as a rate hike portends tightening liquidity conditions, which lead to weaker economic activity. The S&P 500 performance in the three months following an initial rate hike is typically weak or negative, reflecting investor uncertainty.

The following six and twelve-month windows are more complicated. As we share below, in four of the six major hiking cycles since 1994, equities performed well, sustaining positive performance even as rates rose. For instance, during the 1994 cycle, the Fed doubled the Fed Funds rate from 3% to 6%. While it led to a quick 10% S&P 500 drawdown, losses were reversed quickly, and it ultimately sparked one of the great bull runs from 1995 to 2000.

The recent 2022 cycle provides a cautionary counterpoint. The Fed Funds rate hikes resulted in negative returns that worsened across the three, six, and twelve-month forward periods, as extreme valuations and highly speculative trading confronted rapidly rising rates and inflation.

Today’s setup is somewhat similar to 2022, with valuations high and speculative activity rampant. But unlike then, when Fed Funds were near zero as they first hiked rates, interest rates are starting from a relatively high level. The prospect of multiple rate hikes today is much less than in 2022.

We think a rate hike or two may prompt cautious sentiment, but its impact on economic activity and markets could prompt a quick flip to a dovish posture, which has historically been good for stocks.

What To Watch Today

Earnings

No notable releases today.

Economy

No notable releases today.

Market Trading Update

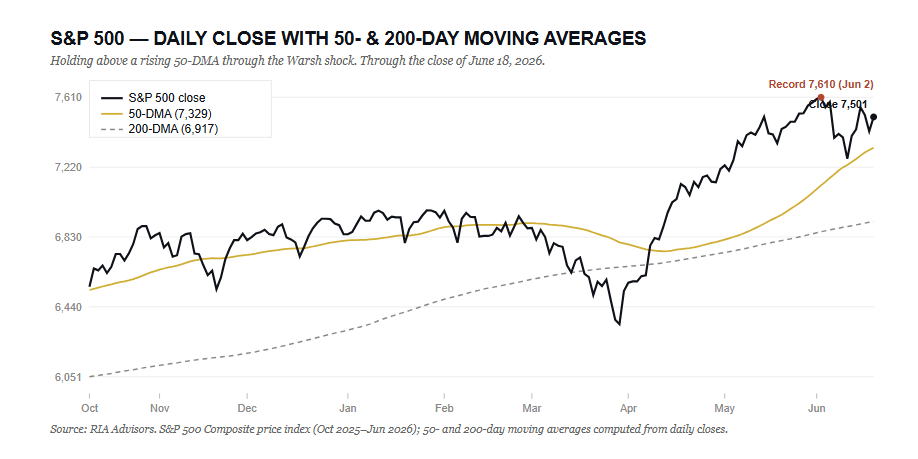

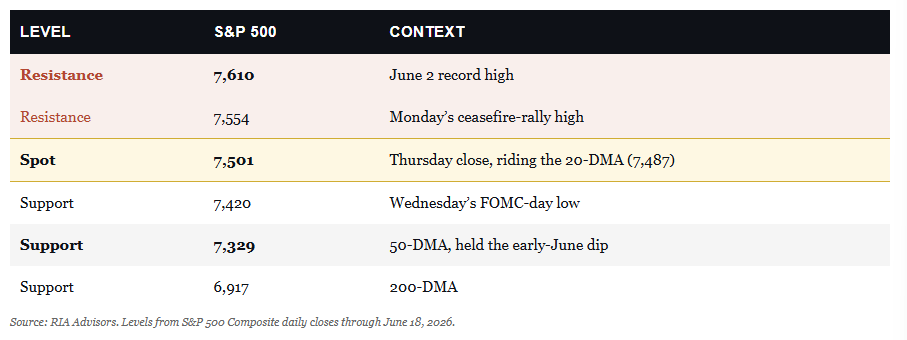

With Friday being a holiday, our last update discussed the surge of inflows into US markets. On Thursday, the S&P 500 closed the holiday-shortened week at 7,500.58, up 0.93%, a number that looks almost dull until you trace the path that produced it. The index ripped to 7,554 on Monday on the US-Iran ceasefire, handed most of it back into Wednesday’s 7,420 low as Kevin Warsh’s hawkish debut landed, then rallied Thursday through the largest options expiration on record to finish the week green and only 1.4% below the June 2 record of 7,609.78.

The trend structure is still constructive. Price sits just above a flattening 20-DMA at 7,487, 2.4% above a rising 50-DMA at 7,329, and 8.4% above the 200-DMA at 6,917. That 50-DMA is the same line that absorbed the 4.5% dip we walked through in last week’s report, and it has not been seriously tested since. RSI at 54.9 is squarely neutral, with room to run in either direction. The lone caution flag is momentum. MACD is still below its signal line with a negative histogram, the leftover of an early-June pullback that price has recovered, but momentum has not.

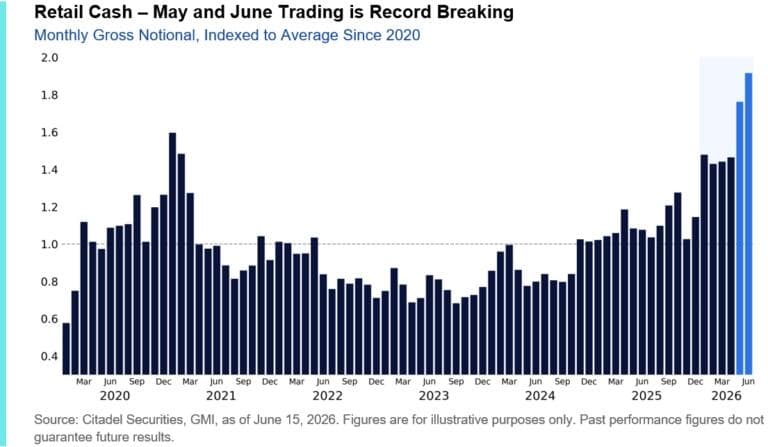

The mechanics are the story for the next two weeks. As Citadel Securities’ Scott Rubner notes, Thursday’s roughly $8.3 trillion quadruple-witching expiration, the largest in history, cleared a substantial block of gamma and leaves the tape more sensitive to flows into month- and quarter-end. Rubner’s read past the reset is constructive: record retail demand, a buy-the-dip reflex that holds while the VIX sits in the mid-teens, and one of the strongest seasonal windows of the year as July’s allocation cycle begins.

“May shattered previous activity records in cash equities, surpassing the prior monthly high set in January 2021 by more than 10%. Retail cash equity volumes ran 60% above the 2025 average and more than twice the 2024 average. From this peak, activity has accelerated further in June, with volumes this month tracking 9% above May’s record. Nine of the ten largest retail trading days ever observed on our platform have occurred in just the last month, including seven during the first half of June alone. Friday (June 12) marked the largest single day of retail net buying in our dataset, surpassing the previous record by 50%.” – Citadel

We splice that flow tailwind against the main story below. The path of least resistance may well be higher, but Warsh just pulled out the guidance cushion, and an OPEX-thinned tape reacts harder to surprises. Respect 7,329 and the 50-DMA as support; treat the 7,610 record as the level to clear; and let price, rather than the narrative, set your exposure.

Trade accordingly.

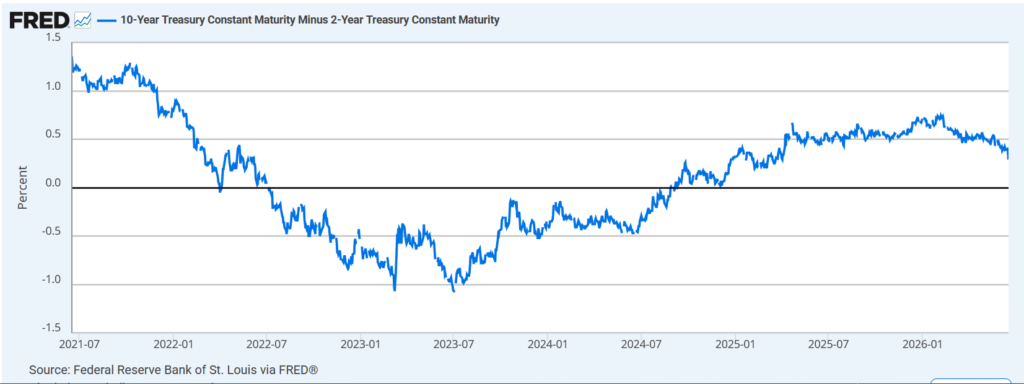

What Does A Flattening Yield Curve Portend For Stocks?

The yield curve, as measured by the difference between the 10-year UST yield and the 2-year yield, fell by nearly 10 bps after the Fed meeting. Furthermore, as we share below, the yield curve has dropped from 72bps to 29bps since the start of the year.

The curve is steepening because shorter rates are rising faster than long rates, as markets priced out rate cuts and are now pricing in Fed Funds rate hikes. Yesterday’s FOMC meeting accelerated that trend.

A bear flattener, where short yields rise more than long yields, tends to coincide with hawkish policy. Interest rate-sensitive equities, such as small caps and financials, are typically the most affected. Financials struggle because the spread between their borrowing costs and lending rates compresses. Small caps suffer because they are disproportionately dependent on floating rate debt that reprices immediately with short rates.

The flattening curve does not guarantee a recession, as we witnessed in 2022-2023. But combined with a Fed now openly discussing rate hikes, a consumer under pressure, significant IPO and secondary-offering equity supply, mid-term elections, and equity valuations near historic highs, this adds another headwind for stock investors.

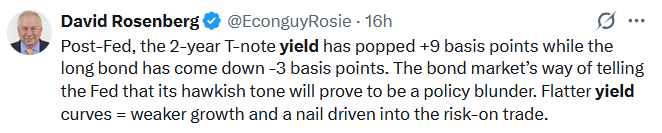

Tweet of the Day

Comments

Log in or sign up to join the conversation.