BLS documents the extent of revisions going from 1st to 2nd, 1st to 3rd, 2nd to 3rd releases of NFP, here. Using the 2019 mean absolute revisions, the range of plausible values for employment growth (not percent growth) is shown below.

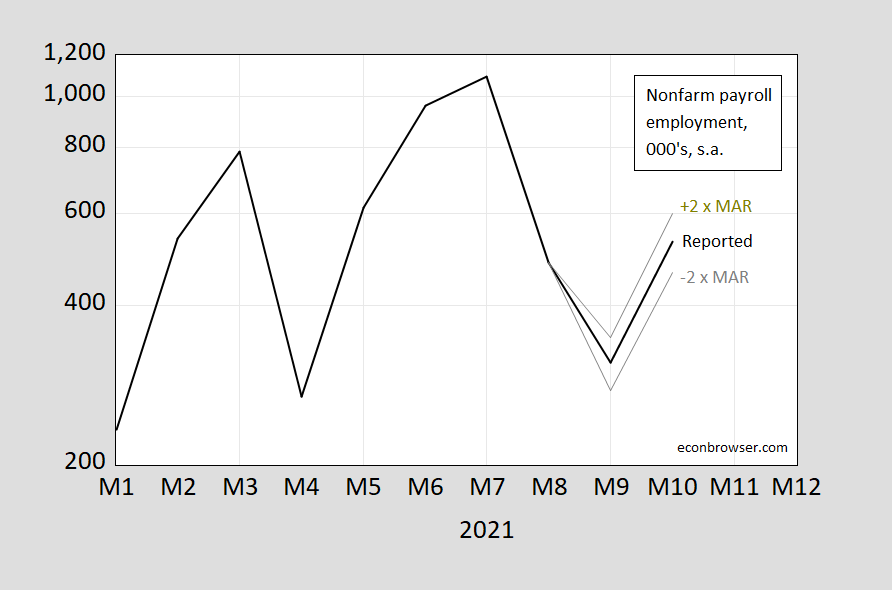

Figure 1: Change in nonfarm payroll employment (black), and 2 times Mean Absolute Revision (MAR) band (gray), using 1st to 3rd for October, and 2nd to 3rd for September.MARs are for 2019. Source: BLS Employment Situation October release, BLS, and author’s calculations.

So, even with this uncertainty regarding revisions (what Manski terms transitory statistical uncertainty), we know that employment is growing or shrinking (mean revision is 5, and 8). Now, 2019 was before the pandemic. What if we use the 2020 revisions? This yields Figure 2.

Figure 2: Change in nonfarm payroll employment (black), and 2 times Mean Absolute Revision (MAR) band (gray), using 1st to 3rd for October, and 2nd to 3rd for September.MARs are for 2020. Source: BLS Employment Situation October release, BLS, and author’s calculations.

So, if one uses some measure of spread regarding data revisions (BLS is using MAR, instead of a standard deviation because changes look non-Normal), we can guess that it’s likely that the September decline in growth will persist to the third revision, and the October increase in growth will persist to the third revision (this kind of addresses reader rsm‘s query, insofar as it can be made coherent).

Comments

Log in or sign up to join the conversation.