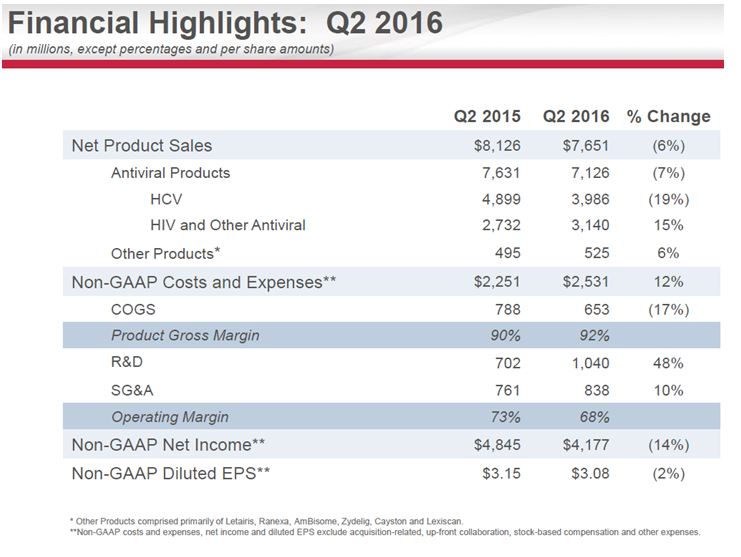

On July 26, after market close, Gilead Sciences (GILD) reported better than expected earnings despite a decline in sales of its hepatitis C drugs. However, Gilead's HIV drugs have continued to outperform increasing sales by 15% year-over-year.

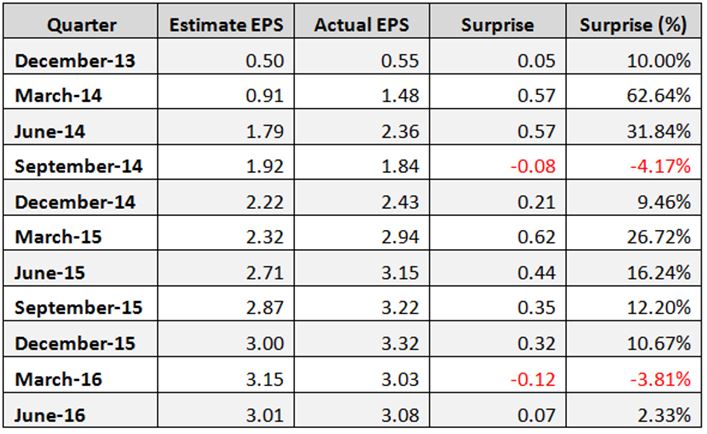

Second quarter adjusted earnings-per-share beat expectations by $0.07 (2.3%). Revenue declined 5.7% to $7.78 billion from a year earlier, missing the average analyst prediction of $7.85 billion. Gilead has shown earnings-per-share surprise in nine of its last eleven quarters, as shown in the table below.

Data: Yahoo Finance

Source: Second Quarter 2016 Earnings Slides

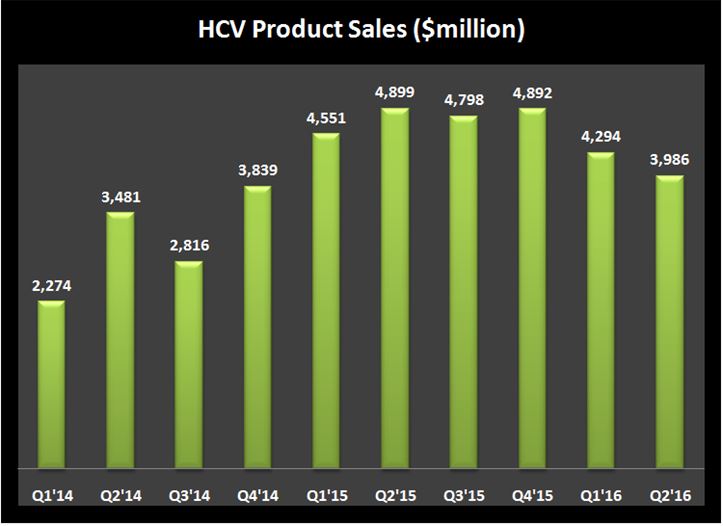

Sales of Gilead’s blockbuster hepatitis C drugs Harvoni, Sovaldi and the new drug Epclusa which was approved at the end of the quarter fell 7.2% compared to the previous quarter and 18.6% year-over-year to $3,986 million. The decline in Gilead’s HCV revenue has been mostly due to the deep discount it had to offer to maintain its high market share due to the competition from AbbVie's (ABBV) HCV drug Viekira, and Merck‘s (MRK) HCV drug Zepatier.

Source: company reports

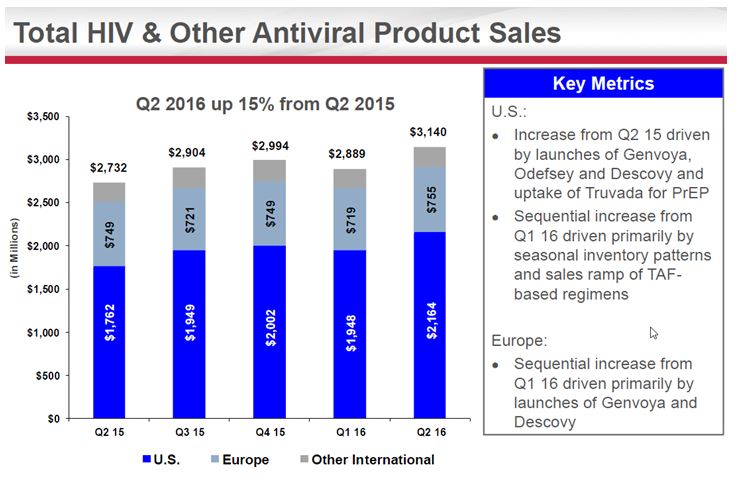

HIV and other antiviral product sales were $3.1 billion compared to $2.7 billion for the same period in 2015 primarily due to increases in sales of its newer and better-tolerated tenofovir alafenamide (TAF) based products. Genvoya, the first of these new HIV drugs achieved sales of $302 million in the second quarter and $158 million in the previous quarter which was the first quarter that the drug was available for sale after its approval in November 2015.

Source: Second Quarter 2016 Earnings Slides

Guidance

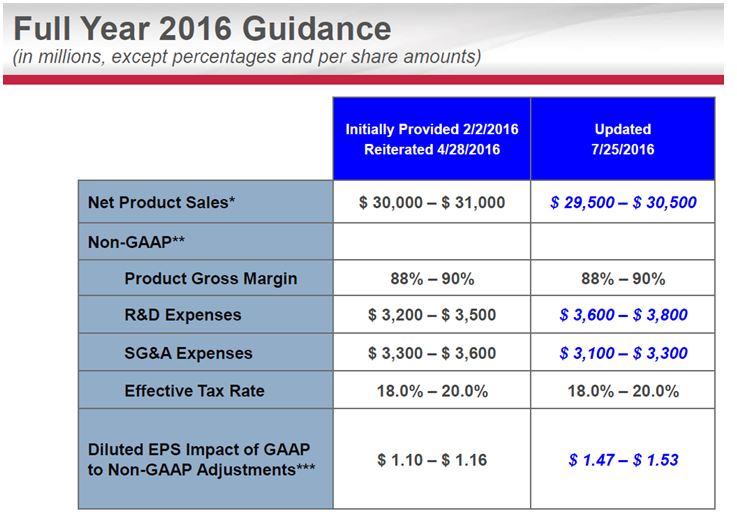

Gilead slightly decreased its full year 2016 net product sales guidance, which it initially provided on February 2, 2016, as shown in the company's table below.

The company expects now a decrease of about 1.6% of its net product sales for the full year 2016 compared to its previous guidance. However, I find it is very encouraging that, on one hand, the company now forecasts 7.2% lower SG&A Expenses and, on the contrary, it plans 10.4% higher R&D Expenses. Companies dedicating more funds for research and development will eventually achieve a better return from new developments. The midpoint of 2016 planned R&D Expenses of $3,700 million is 22.8% higher than the 2015 R&D Expenses of $3,014 million. In 2014 R&D Expenses were at $2,854 million, and in 2013 were at $2,120 million.

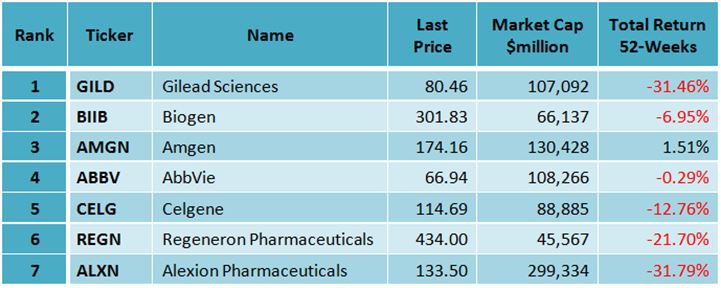

The decline in the Gilead's hepatitis C drugs sales has worried investors who have also been disappointed by the fact that the company has been very cautious taking a decision about new major acquisitions. As a result, GILD'S shares have given a negative return (including dividends) of -31.5% in the last 52 weeks, as shown in the table below, compared to the other large-cap biotech peers 52-weeks return.

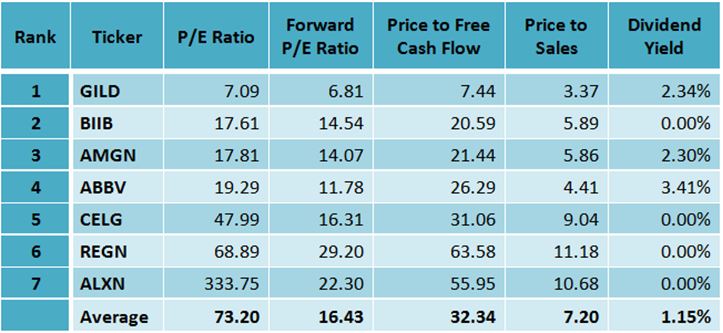

However, Gilead's shares trade at a significant discount to the other large-cap biotech peers, as shown in the table below. Gilead's trailing P/E ratio of 7.09 is way below the group average of 73.2, and its forward P/E of 6.81 is also much lower than the group average of 16.43. What's more, Gilead's price to free cash flow is very low at 7.44 compared to an average of 32.34 for the group, and its price to sales ratio of 3.37 is also much lower of the group average of 7.20.

Source: Portfolio123

In my opinion, such a significant discount cannot be sustainable, and sooner or later investors will find out that Gilead's stock is considerably undervalued which will cause its stock to rise sharply. After all, Gilead has a rich pipeline of over 25 different programs under development, and it is increasing its research and development expenses. Gilead's rich pipeline is creating opportunities that may allow the transformation of the treatment of many diseases, like NASH, HPV, inflammatory diseases, certain cancers, and cardiovascular conditions for which few, if any, options exist.

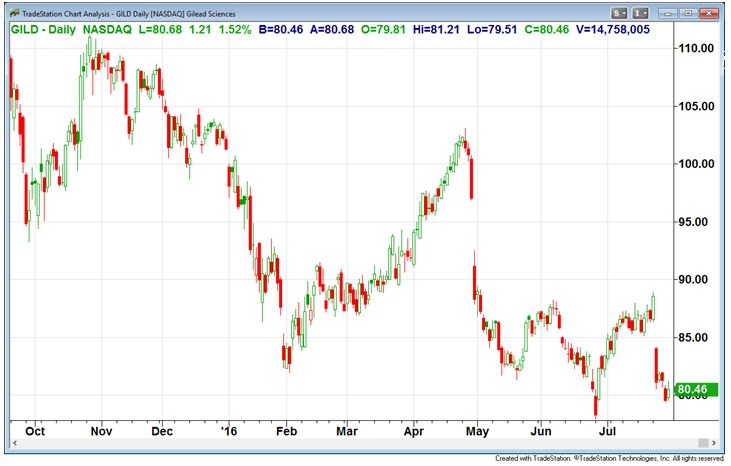

Since the beginning of the year, GILD's stock is down 20.5% while the S&P 500 Index has increased 6.2%, and the Nasdaq Composite Index has gained 3.5%. However, since the beginning of 2012, GILD's stock has gained an astounding 300%. In this period, the S&P 500 Index has increased 72.6%, and the Nasdaq Composite Index has risen 99%. According to TipRanks, the average target price of the top analysts is at $109.13, an upside of 35.6% from its August 1 close price, which appears reasonable, in my opinion.

GILD Daily Chart

Chart: TradeStation Group, Inc.

Conclusion

Gilead Sciences delivered better than expected second quarter earnings despite a decline in sales of its hepatitis C drugs. However, Gilead's HIV drugs have continued to outperform increasing sales by 15% year-over-year. Despite decreasing slightly net product sales guidance for the year, I find it is very encouraging that the company now forecasts 7.2% lower SG&A Expenses, and it plans 10.4% higher R&D Expenses. Gilead's shares trade at a significant discount to the other large-cap biotech peers, and in my opinion, such a significant discount cannot be sustainable, and sooner or later investors will find out that Gilead's stock is considerably undervalued which will cause its stock to rise sharply. The average target price of the top analysts is at $109.13, an upside of 35.6% from its August 1 close price, which appears reasonable, in my opinion.

Comments

Log in or sign up to join the conversation.