The shares of Micron Technology (MU) have fallen sharply from their eighteen years high at the end of May 2018, but have started to recover in the last three weeks. Micron's stock last price of $36.01 on January 11, is 44.31% down from its 52 weeks high of $64.66 at intraday trade on May 29, 2018, but it is already 26.84% up from its 52 weeks low of $28.39 at intraday trade December 26, 2018. As I see it, the drop in its price creates an excellent opportunity to buy this great company's stock at a very attractive price, mainly due to its superb valuation and high growth prospects.

Micron is the only American major producer of memory chips. 68% of the overall company revenue in the first quarter of fiscal 2019 came from DRAM. Unlike flash memory, DRAM is volatile memory which means that information is lost when power is lost. The DRAM is commonly used in mobile devices, desktop computers, smart televisions, automotive systems, cameras, and much more. Three companies dominate the global DRAM market producing about 96% of the total world production of DRAM. South Korea based Samsung has about 45% of the global output, and the other South Korea based SK Hynix has about 29%, while Micron has about 22% of the world DRAM production.

28% of the overall company revenue in the first quarter of fiscal 2019 came from NAND flash memory; Micron is the third largest NAND manufacturer in the world. Samsung holds a market share of about 35.6%, Western Digital (WDC) has about 14.9% market share, Micron about 13.1%, and SK Hynix 10.8% of the global NAND production. NAND flash memory is non-volatile storage that does not require power to retain data. It is used in devices to which large files are frequently uploaded and replaced. It is found in most modern cell phones as the main and even as the secondary storage, in memory cards, and solid-state drives as computer storage.

Micron's fundamentals are excellent, and its valuation ratios indicate an undervalued stock. Micron's trailing price to earnings is extremely low at 2.97, and its forward P/E is also very low at 5.11. The price to free cash flow ratio is exceptionally low at 4.89, and its price to earnings to growth ratio PEG is also very low at 0.18.

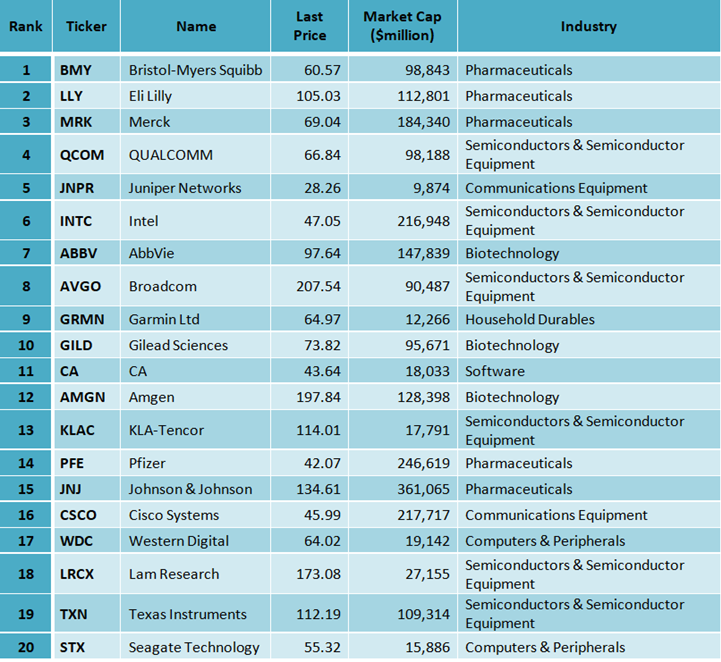

Micron's Enterprise Value/EBITDA ratio is extremely low at 1.93. In fact, its EV/EBITDA ratio is the lowest among all S&P 500 companies, as shown in the table below of the twenty S&P 500 companies with the lowest EV/EBITDA ratio. According to James P. O'Shaughnessy, the Enterprise Value/EBITDA ratio is the best-performing single value factor. In his impressive book "What Works on Wall Street," Mr. O'Shaughnessy demonstrates that 46 years backtesting, from 1963 to 2009, have shown that companies with the lowest EV/EBITDA ratio have given the best return.

Moreover, Micron has recorded substantial growth in the last few years. The company's annual average sales growth over the last five years was extremely high at 27.3%, and the average EPS growth was very high at 58.8%. The average annual estimated EPS growth for the next five years is also high at 25%.

Summary

New applications like the Internet of Things (IoT), Artificial intelligence (AI), Big Data and Cloud will need an increasing amount of memory which will benefit Micron Technology. The company's fundamentals are excellent, its valuation ratios indicate an undervalued stock, and it has high growth prospects.

According to TipRanks, the average target price of the top analysts is at $49.22, an upside of 36.7% from its January 11 close price, however, in my opinion, shares could go even higher. As I see it, the recent drop in its price creates an excellent opportunity to buy MU's stock at an attractive price.

Comments

Log in or sign up to join the conversation.