Our firm has received several questions recently about the strength of the U.S. economy and the risks surrounding software and semiconductor stocks. Some of this discussion has been influenced by a recent Seeking Alpha article, Worse Than 1999. While the comparison to the late-1990s technology bubble is attention‑grabbing, the reality today is more nuanced. Below I provide context on market concentration, valuations, AI‑driven disruption, and the broader economic environment.

A Highly Concentrated S&P 500 Index

Currently, we include a concentration chart in client reviews, and the trend remains clear: the S&P 500 has become increasingly dominated by a handful of mega‑cap technology companies. As these companies grow larger within the index, automatic flows from 401(k)s and other passive vehicles allocate a greater share of each invested dollar to them. This “autopilot” buying pushes their weights even higher.

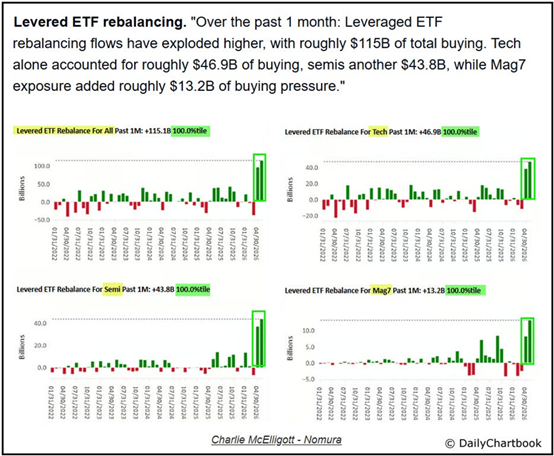

Another dynamic amplifying this trend is the rapid growth of leveraged ETFs, including single‑stock leveraged products. These vehicles mechanically buy into strength and sell into weakness, contributing to sharper price moves in the largest technology names. Recent investment flows into leveraged ETFs have been significant, and the performance of these products through May has been strong, further attracting investor interest. While passive flows are not inherently problematic, they can create conditions where index performance becomes overly dependent on a narrow group of companies.

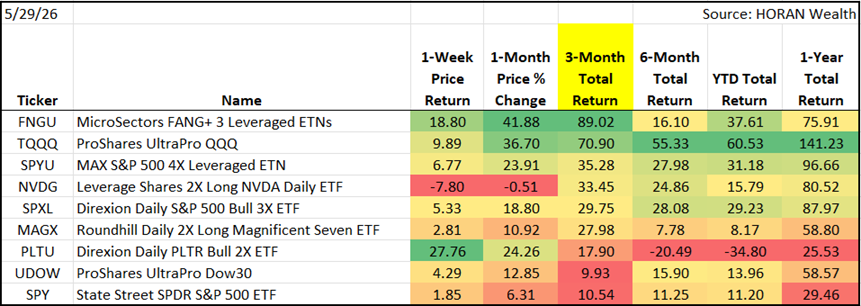

Below is a table showing the return of a select few of these leverage ETF’s through the end of May.

The key question is whether this concentration ultimately leads to weaker long‑term index returns, and if so, when that shift might occur.

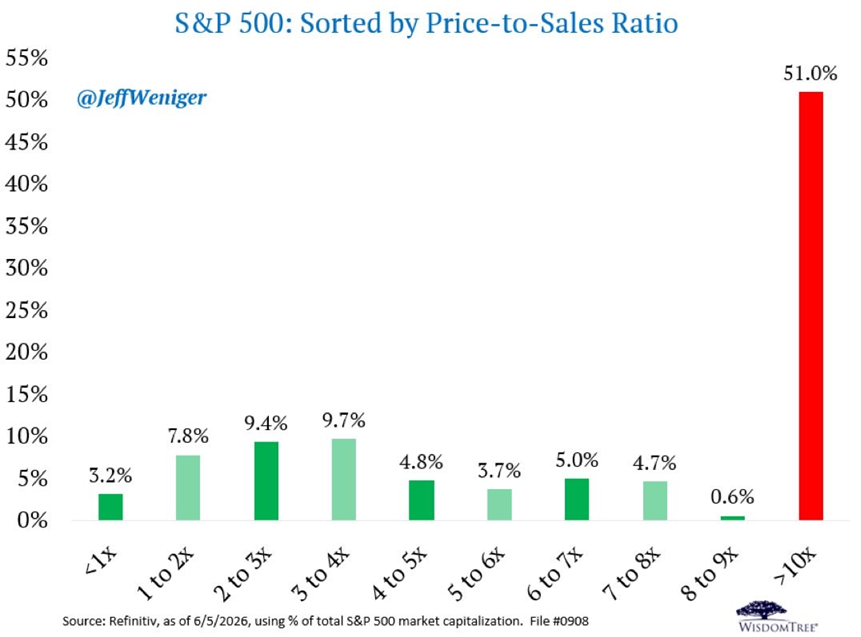

Valuations: Half the S&P 500 Trades at 10x Sales

Below is a chart from WisdomTree’s head of equity that shows 51% of S&P 500 stocks are trading at 10 times sales.

As highlighted by a Switzerland investment firm, in 2002, after Sun Microsystems crashed 90%, CEO Scott McNealy famously said this about his own stock at 10x sales "At 10x revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends. Zero costs. Zero R&D. Zero taxes. Zero employees. What were you thinking?" His point was simple: paying 10× sales requires perfection. Today, half the index trades at that level.

Earnings Growth: A key Difference From 2000

Despite valuation concerns, one important distinction between today and the 2000 tech bubble is earnings. Technology companies are generating real profits and growing them rapidly.

S&P 500 earnings are up ~29% year‑over‑year in Q1 2026.

The index is up 7.9% year‑to‑date, meaning the P/E ratio has actually contracted.

For 2026, S&P 500 earnings are expected to grow 25%.

Information Technology sector earnings are up 56.8% in Q1.

This type of earnings acceleration is typically seen coming out of a recession—not in the middle of a non‑recessionary bull market.

However, investors are increasingly looking ahead to 2027. Earnings growth is expected to slow to 16.4%, down from 25.2% in 2026. When the rate of growth slows (the “second derivative”), markets can face headwinds—especially if AI and data‑center spending fails to deliver the profitability currently expected.

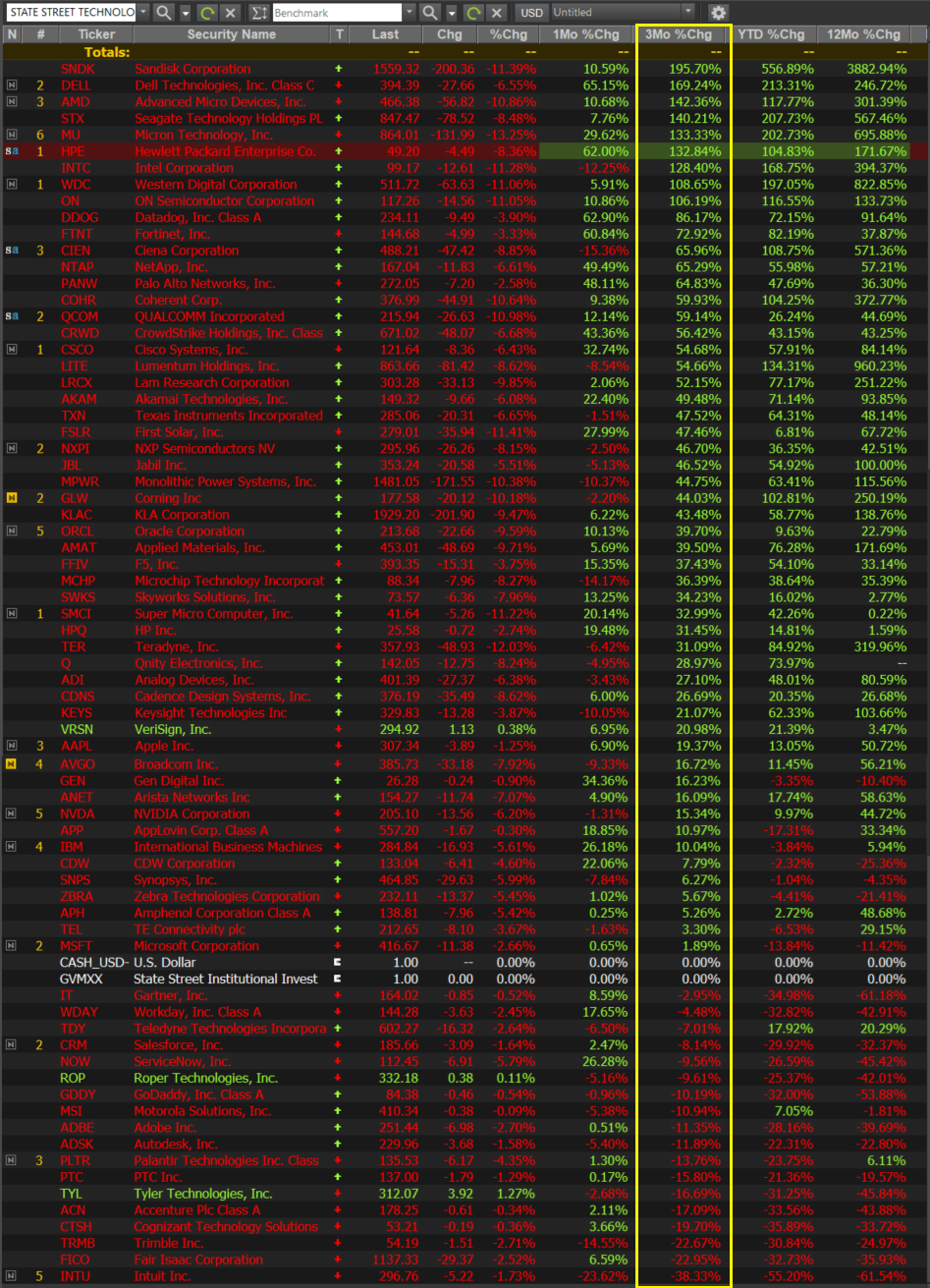

A.I's Impact on Software and Semiconductors

The recent weakness in software stocks is tied to concerns about agentic AI.

Agentic AI refers to autonomous artificial intelligence systems designed to achieve specific goals with minimal human supervision. Unlike traditional AI, which operates within predefined constraints and requires human intervention, agentic AI exhibits autonomy, adaptability, and goal-driven behavior. It uses AI agents, machine learning models that mimic human decision-making, to solve problems in real-time by interacting with their environment. These systems leverage large language models (LLMs) and generative AI techniques to function in dynamic environments. While generative AI focuses on creating content like text or images, agentic AI extends this by using generated outputs to perform complex tasks autonomously, such as booking flights or managing workflows.

Unlike traditional software, agentic AI can replicate or replace certain functions that companies currently monetize through subscription models. For example, if AI tools can perform tasks similar to Adobe Creative Suite or other enterprise software, the value of those subscription revenues may come under pressure. This dynamic is already contributing to stress in parts of the private credit market tied to leveraged software companies.

On the semiconductor side, hyperscalers are spending enormous sums on data‑center and AI‑related capex. Stocks like Micron, Broadcom, and Dell have seen parabolic moves: Dell was up 32% in a single day two weeks ago. While this reflects strong demand, it also raises the question: Will the return on AI capex justify the investment?

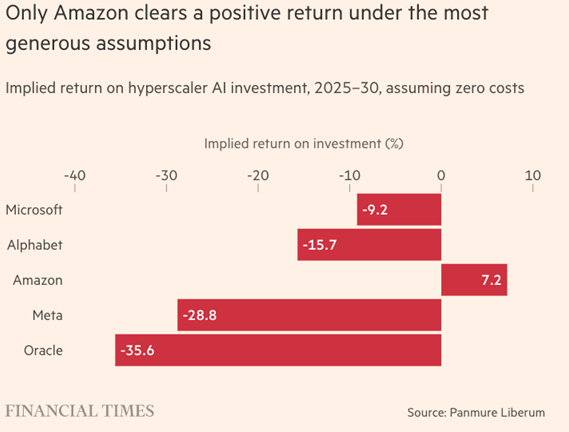

A recent Financial Times analysis noted estimated AI ROI as follows:

Microsoft: –9%

Google: –15%

Meta: –28%

Oracle: –35%

Amazon: slightly positive

These figures underscore the uncertainty around AI monetization.

Given the strong run‑up in many mega‑cap technology stocks, we believe it is reasonable for investors who are overweight these names to consider trimming positions, even if the position is held in a taxable account where capital gains are a factor. For example, Apple trades at 33× forward earnings with an expected 10% EPS growth rate. We continue to like many of these companies, but recent returns appear ahead of near-term fundamentals.

A.I. and the Job Market: A Net Positive Over Time

Despite concerns about job displacement, AI should ultimately be a net positive for the economy. It lowers barriers to entrepreneurship and increases productivity. Historically, new business formation has been a key driver of job creation, and AI may accelerate this trend.

Interest Rates and The Economic Backdrop

Higher long‑term interest rates remain a headwind for equity valuations. Rising energy prices and the recent uptick in yields have tightened financial conditions, giving the Federal Reserve room to maintain a neutral stance at its upcoming meeting. Friday’s market selloff was partly driven by higher rates following a strong payroll report.

Importantly, the economy and the stock market are not the same, though they tend to correlate over time. Economist Scott Grannis, writing at Calafia Beach Pundit, recently concluded that the macro environment is Still Looking Good. His view aligns with our assessment, and the article does not incorporate the positive impact of the OBBBA on corporate earnings, cash flow, and margins, as highlighted in a recent Wells Fargo article.

Conclusion

The U.S. economy remains healthy, supported by strong earnings growth and resilient consumer and business activity. However, the equity market faces several crosscurrents:

Elevated concentration in mega‑cap technology

Valuations that assume near‑perfect execution

Slowing earnings growth in 2027

Uncertainty around AI ROI

Higher long‑term interest rates

We continue to believe in the long‑term strength of many leading technology companies, but recent performance and valuations warrant thoughtful risk management, especially for investors with concentrated positions in some of these stocks.

Comments

Log in or sign up to join the conversation.