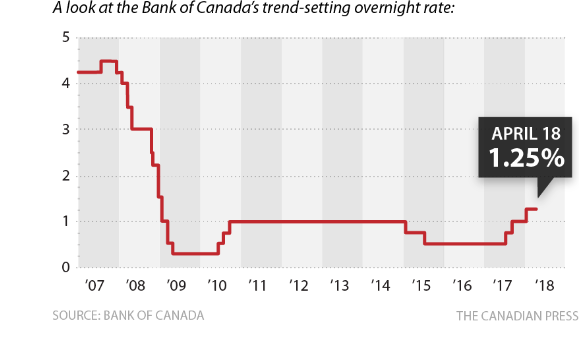

Recent policy statements by the Bank of Canada shows the difficulty in mapping out the path for future interest rates. Almost every statement by Governor Poloz is sprinkled with the reference to the need for a cautious approach to setting rates. Despite a relatively decent job growth, an economy operating near capacity and inflation around the benchmark 2%, the Bank is still very tentative when it comes to the way forward. Why is the Bank of Canada so cautious?

Sustainable Growth Still an Issue. The Governor makes it clear that interest rates remain very low “because the economy is not yet able to remain at full capacity on its own”[1] This is the first clue that we can expect very slow, moderate changes in rates. The Bank simply does feel that we are out of the woods yet, in the sense that we can live with higher interest rates now and in the near future. The Governor emphasizes that “sustainability of this level of activity is not assured”. He could not be more direct concerning his reason for caution going forward.

External Risks to the Economy. Just how much support the economy needs is revealed in his discussion of the “neutral “rate of interest. The neutral rate of interest is the rate that prevails when an economy’s output is at its potential level and inflation is at the central bank’s target of 2 per cent. The Bank calculates that neutral interest is between 2.5 to 3.5 per cent, given a 2 per cent inflation rate[2]. With the current bank rate set a half of the neutral rate, the Bank recognizes that there is so much “uncertainty around trade conflicts and escalating geopolitical risks” that we are long way from hitting the neutral rate.

Vulnerabilities at Home. Every discussion about interest rates is framed within a broader discussion of the level of household debt in Canada. Canadians have amassed a C$2-trillion mountain of household debt, including C$1.5 trillion in mortgages. As the Governor puts it, “its sheer size means that its risks will be with us for some time.”[3]

Interest Rate Sensitivity Greater Than Ever. Research at the Bank of Canada provides evidence that the economy is more sensitive to interest increases than in the past. Thus, the new, more stringent mortgage guidelines introduced this year are having a significant impact on home purchases coupled with increases in mortgage rates. The Bank cannot push aggressively ahead without generating more stress on the consumer.

It is little wonder that the Bank of Canada is uneasy these days when asked about the future path of interest rates.

[1] Monetary Policy Report Press Conference Opening Statement, April 18, 2018 ( italics are mine).

[2] ibid

[3] Stephen Poloz, Canada’s Economy and Household Debt: How Big Is the Problem? Yellowknife Chamber of Commerce, Yellowknife, NWT, May 1, 2018

Comments

Log in or sign up to join the conversation.