A spade of good economic news came Canada`s way this past quarter, yet one should be careful in drawing conclusions that the economy is on a solid growth path. Since mid-2016, Canada has grown at a 4.3 per cent annual rate, the fastest pace since the early stages of the recovery after the financial crisis of 2008. Responding to these results, a recent BMO newsletter claimed that `` we have liftoff``.[1] Forecasters are now anticipating that we will see 2.50 -3.0 per cent growth for all of 2017 and some go as far as to claim this will outpace U.S. performance.

Before we get ready to pop the Champagne bottles, we should take a more measured look at the recent performance. A more sobering assessment is provided by the Bank of Canada in recent speeches by Governor Poloz. The Bank makes its point very clearly when it states that `` while there have been recent gains in employment, subdued growth in wages and hours worked continue to reflect persistent economic slack in Canada, in contrast to the United States. ``

What lies behind this very guarded outlook? Let’s look at some of the more important underlying economic conditions affecting incomes and growth. To begin with, the Bank places considerable weight to various measures that determine potential GDP. At issue is the output gap which is the cumulative difference between how fast an economy can grow, and its actual rate of expansion. The Bank rate is set to promote growth that will ultimately close the gap. And, the results in the past 6 months have shown that there is movement towards closing this gap. That is, the economy is growing somewhat faster than its potential which gives rise to the reference that we have “liftoff”.

The average worker, however, continues to feel the great pull of gravity. Chart 1 compares wage growth in the two countries. The Canadian worker has seen his/her wage growth decline to 1 per cent annually in the first quarter of 2017 from 3 per cent experienced 6 months earlier. Time and again, Bank officials express concern that wages are not expanding sufficiently and argue that this is a sign that the labour market has considerable slack which reflected in the output gap.

Chart 1 Comparison of Average Hourly Earnings, U.S. and Canada

The only consolation for the Canadian worker is that inflation remains quite subdued (Chart 2). All 3 measures used by the Bank indicate that the inflation rate declined during this period and, as such, average real wages held up somewhat.

Chart 2 Canadian Consumer Prices

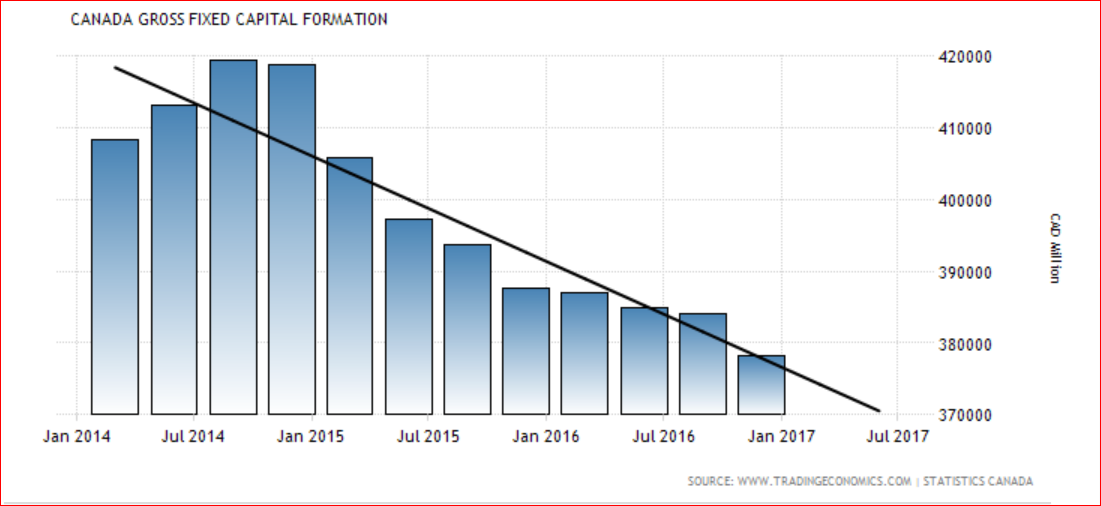

To my mind, the most worrisome aspect of the Canadian economy is the abysmal record of business capital investment (Chart 3). Starting with the collapse of oil prices in 2014, gross fixed investment in Canada has been on a steady decline with no abatement. Most of the weakness in capital formation is directly traced to the huge drop in investment in energy production, causing spillover effects into many other sectors.

Chart 3 Canadian Gross Fixed Capital Formations

In the fact, the Bank makes it abundantly clear that:

Canada has a lot more room to grow, because we have not recovered fully from the oil price shock.... {and} we have a level difference between the two economies, more unemployment, more excess capacity, a cushion there, which means that we can grow faster than the U.S. for a while to use up that capacity[2].

In sum, just as the saying goes that “one swallow does not make a summer”, we should not jump to conclusions that one quarter’s growth makes for accelerated growth this summer.

[1] http://globalnews.ca/news/3348062/canadian-economy-could-outpace-u-s-in-2017-unless-americas-protectionism-kills-that-momentum/

[2] http://www.bankofcanada.ca/2017/03/canada-150-takes-world-raise-nation/canada

Comments

Log in or sign up to join the conversation.