While there was a big downside NFP surprise (194K vs. Bloomberg consensus of 500K), the overall picture is not much altered:

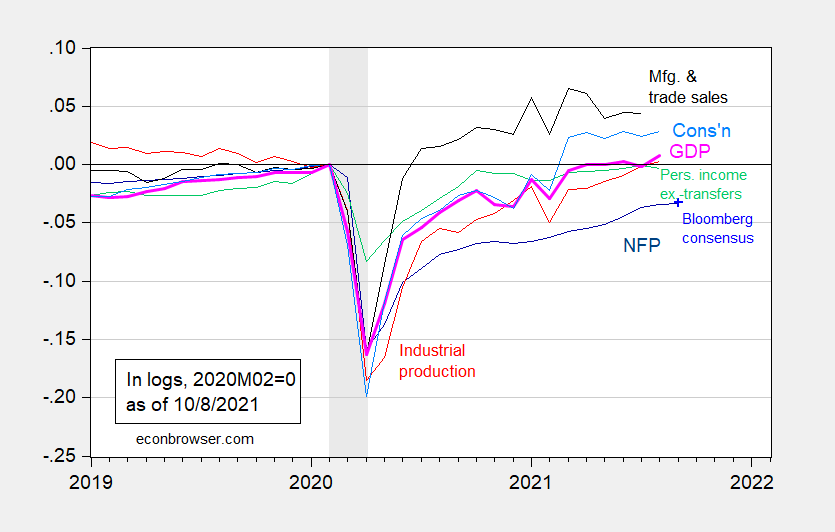

Figure 1: Nonfarm payroll employment from August release (dark blue), industrial production (red), personal income excluding transfers in Ch.2012$ (green), manufacturing and trade sales in Ch.2012$ (black), consumption in Ch.2012$ (light blue), and monthly GDP in Ch.2012$ (pink), all log normalized to 2020M02=0. NBER defined recession dates shaded gray. Source: BLS, Federal Reserve, BEA, via FRED, IHS Markit (nee Macroeconomic Advisers) (10/1/2021 release), NBER, and author’s calculations.

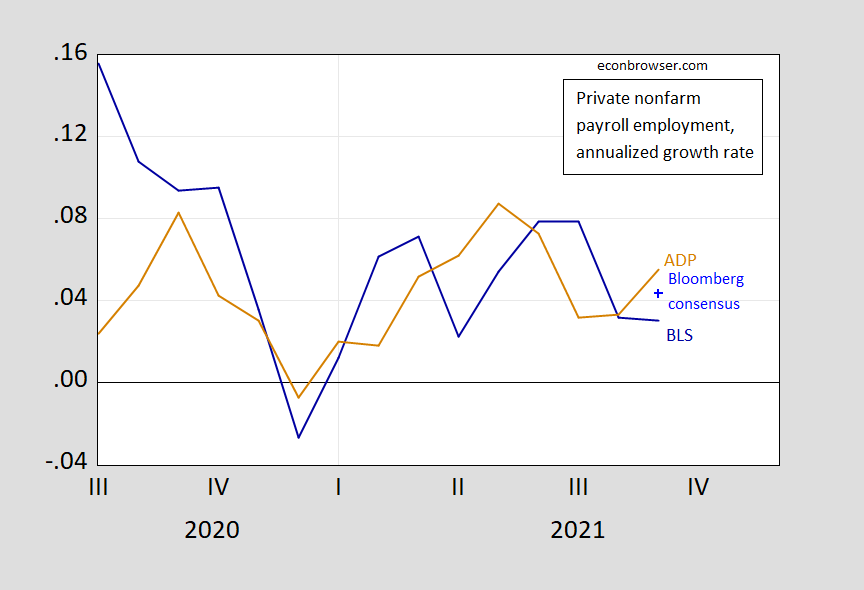

There are reasons to believe that the September figures are perhaps distorted somewhat by seasonal issues (including school-related), as well as real-world factors like the rise of the delta variant’s impact, to be discussed in the next post. For now, it’s useful to consider private employment, which experienced a smaller miss (317K actual vs. 455K consensus).

Figure 2: Annualized growth rate of official private nonfarm payroll employment (blue), ADP private NFP (brown), and Bloomberg consensus (blue +). Growth rates calculated as log differences. Source: BLS, ADP via FRED, and author’s calculations.

What is true is that growth seems to be decelerating. Current nowcasts for Q3 GDP are 1.4% (IHS-MarkIt), 1.3% (Atlanta Fed), and 3.25% (Goldman Sachs). As reported by CR, Merrill2%.

Comments

Log in or sign up to join the conversation.