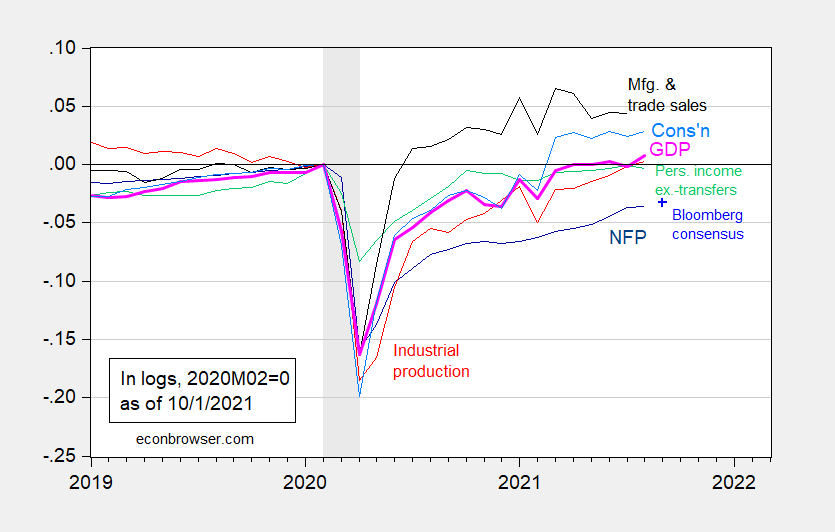

Consumption rises as personal income ex-transfers fall in August, and monthly GDP rebounds somewhat. Consumption remains 2.8% above 2020M02 levels (the latest NBER peak). Here’s the picture of the macroeconomy (for some key indicators followed by the NBER’s BCDC).

Figure 1: Nonfarm payroll employment from August release (dark blue), industrial production (red), personal income excluding transfers in Ch.2012$ (green), manufacturing and trade sales in Ch.2012$ (black), consumption in Ch.2012$ (light blue), and monthly GDP in Ch.2012$ (pink), all log normalized to 2020M02=0. NBER defined recession dates shaded gray. Source: BLS, Federal Reserve, BEA, via FRED, IHS Markit (nee Macroeconomic Advisers) (10/1/2021 release), NBER, and author’s calculations.

Combined with the consensus for September nonfarm payroll employment, recovery continues, but at a halting pace.

As of today, Q3 Nowcasts are 2.2% (IHS-MarkIt), 2.3% (Atlanta Fed), and 4.25% (Goldman Sachs).

Comments

Log in or sign up to join the conversation.