Deceleration continues, according to some key indicators noted by the NBER’s Business Cycle Dating Committee (BCDC).

(Click on image to enlarge)

Figure 1: Nonfarm payroll employment (dark blue), Bloomberg consensus for September as of 10/1 (light blue square), industrial production (red), personal income excluding transfers in Ch.2012$ (green), manufacturing and trade sales in Ch.2012$ (black), and monthly GDP in Ch.2012$ (pink), all log normalized to 2019M02=0. Source: BLS, Federal Reserve, BEA, via FRED, Macroeconomic Advisers (10/1 release), NBER, Bloomberg, and author’s calculations.

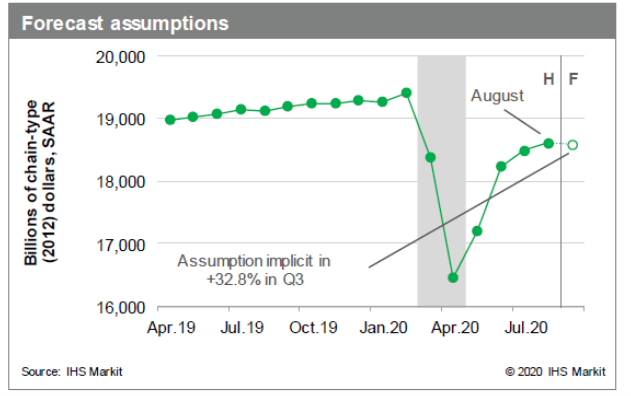

IHS/MarkIt provides a projection of the September GDP number consistent with their forecast for Q3: essentially 0% growth in September.

(Click on image to enlarge)

Source: IHS/MarkIt, October 1, 2020.

So, we are already decelerating rapidly along a number of dimensions, as passage of a pre-election package becomes ever more unlikely. Deutsche Bank’s conditional forecast is zero growth on Q4. With the political — and hence policy — uncertainty possible in the election’s wake, don’t rule out another leg downward in economic activity.

Comments

Log in or sign up to join the conversation.