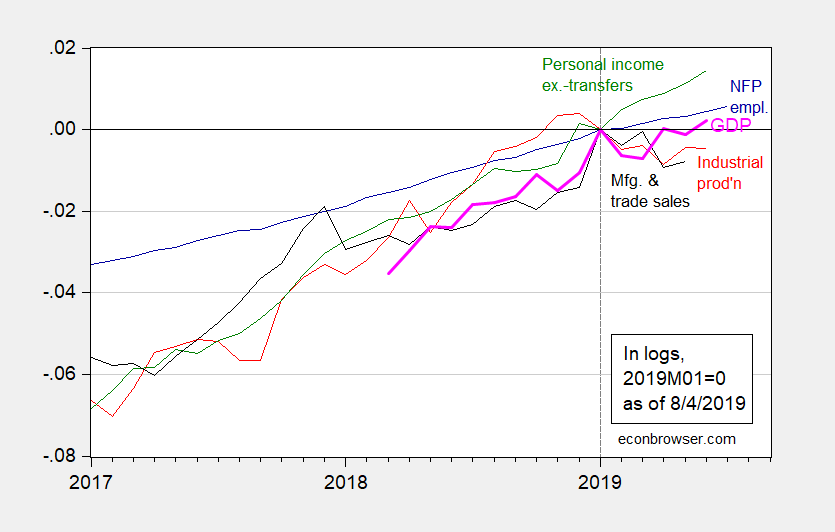

Still rising, so likely no recession as of June 2019.

(Click on image to enlarge)

Figure 1: Nonfarm payroll employment (blue), industrial production (red), personal income excluding transfers in Ch.2012$ (green), manufacturing and trade sales in Ch.2012$ (black), and monthly GDP in Ch.2012$ (pink bold), all log normalized to 2019M01=0.Source: BLS, Federal Reserve, BEA, via FRED, Macroeconomic Advisers (7/25 release), and author’s calculations.

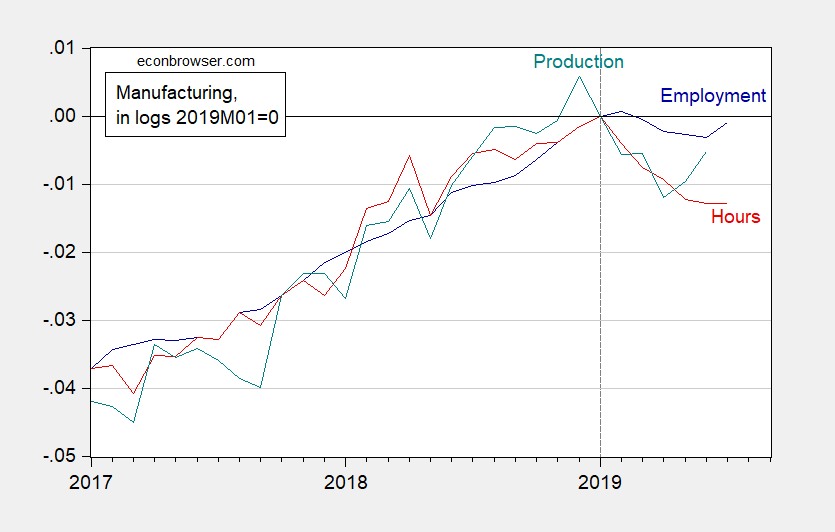

On the other hand, we need to think about how much punishment the manufacturing sector can take without spillover to the rest of the economy. Employment is resilient, but hours and production indices have dropped, with little evidence of recovery in the former.

(Click on image to enlarge)

Figure 2: Manufacturing employment (blue), aggregate hours of production and nonsupervisory workers (red) and production (teal), in logs 2019M01=0. Source: BLS, Federal Reserve via FRED, and author’s calculations.

When one considers the backdrop to worldwide trade, and the tradables sector, it’s pretty worrisome. We have slowing world trade growth, we have an incipient currency war between the US and China, and the possibility of a major conflict in a US Section 232 action on automobiles, centered on Europe. And with no clear end-date to the resolution of these issues, we can assume trade policy (and economic) uncertainty will continue to hover over every decision.

Comments

Log in or sign up to join the conversation.