I frequently criticize the ECB’s weird inflation target. To their credit, ECB policymakers have finally seen the light:

After years of failing to lift inflation up to its objective, the ECB has ditched its target of “close to, but below, 2 per cent”, which policymakers concluded was too opaque and implied a cap on price growth.

The central bank said its new target of 2 per cent was symmetric, “meaning negative and positive deviations of inflation from the target are equally undesirable”. The new target is a medium-term objective with flexibility to fluctuate in either direction in the short term.

This will provide more clarity and transparency to ECB policymaking.

Throughout history, central bank policymakers have often debated two issues at the same time: What rate of inflation is the appropriate goal, and what is the best way to achieve that goal? This caused policymakers to split up into “hawks” and “doves”, which added uncertainty about the future course of monetary policy. If all policymakers can agree to the same goal, then the only differences are technical, not ideological. Markets would face less uncertainty.

I’m not so naive to think the ECB has entirely moved past hawks and doves, but this is a step in the right direction. The next step should be some sort of level targeting (or AIT), which would further move the bank away from the hawk/dove split and toward a more enlightened approach to monetary policy.

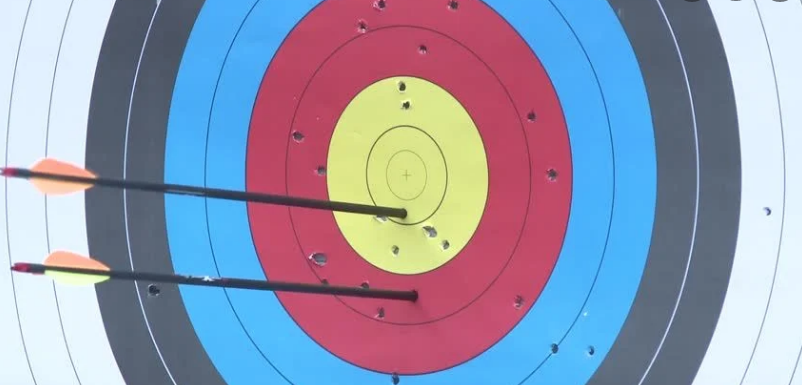

Which arrow is “close, but just below the bullseye”? The Italians would say the top arrow whereas the Germans would say the bottom arrow.

Both groups can agree that this is a bullseye:

Comments

Log in or sign up to join the conversation.