TM Editors' note: This article discusses a penny stock and/or microcap. Such stocks are easily manipulated; do your own careful due diligence.

I have been following Bark Inc. (BARK) since last year, and it has performed horribly. On Friday, the FTSE Russell company announced that BARK is on the preliminary list, based on data from April 30th, to be removed from the Russell 2000. London Stock Exchange Group (LSEG), which owns the FTSE Russell indexes, is changing things this year and rebalancing twice a year rather than once a year, as was announced in late April. There will be several more updates, including one in May and three in June, and the index will be reconstituted on June 26th after the market closes. While there is a chance that BARK will not get booted by the Russell 2000, it is likely to be removed. In this article, I review the company, discuss the outlook, take a look at the valuation, assess the chart and then set a target that suggests it is a Buy.

BARK Went Public in 2021

BARK, doing business then as Barkbox, was founded in NYC in 2011. It announced a merger with the SPAC Northern Star Acquisition Corp. in late 2020 and began trading in June 2021. The company is all about dogs:

Bark, Inc. sells toys and accessories as well as consumables, and it also has an airline for transporting dogs, BARK Air. It sells its products direct-to-consumer and also in over 50K stores and e-tailers.

The company is run by a co-founder, Matt Meeker, who serves as CEO and Executive Chairman. He co-founded Meetup in 2002. Two other co-founders work there as well.

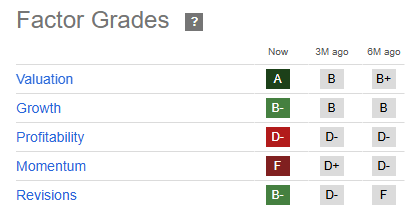

BARK has a Quantitative Rating at Seeking Alpha of just 1.81, which is a Sell. The weakness is mainly due to its poor price momentum, though the lack of profitability factors in as well:

There are just 5050 followers of BARK at Seeking Alpha, which is a tiny fraction of rival Chewy, Inc. (CHWY), which went public IN 2019 and has 38,180 followers there. Here at TalkMarkets, there have been no articles on BARK, while CHWY does have content.

Readers can learn more about BARK by visiting the website, checking out the investor relations page or reading its SEC filings.

BARK Has Seen Its Revenue Decline

Ahead of the SPAC merger, Bark indicated that FY2021 revenue for the year ending in March would be $365 million. For FY2026, which will have it financials announced on June 9th, the company is projected to have generated revenue of $404.6 million, which would be a decline for the year of 16%. In Q4, the outlook is for a decline of 17%. This is a pretty big decline. Since going public, the annual revenue was over $500 million in FY22, grew to $535 million in FY23 and then fell to $490 million in FY24 and then $484 million in FY25.

Chewy, Inc. (CHWY) is the closest publicly-traded provider of animal products. It is much larger and has already reported its FY26, which ended in January. Sales have been increasing there, with the last fiscal year up 6% to $12.6 billion. Even larger than CHWY but not an exact competitor to the company or BARK is Petco Health and Wellness (WOOF). Petco is a very large store, and it is a provider of veterinary care. WOOF is also on a January fiscal year-end, and it's revenue lifted 21% in what it calls FY25.

While it is discouraging to see sales slip, profitability has improved substantially. In FY25, the loss from operations decreased from -$45.5 million to -$35.1 million, and it was an even larger loss in FY23 at -$63.8 million. Including net interest income, the FY25 loss was -$32.9 million. Despite lower sales in FY25, gross profits fell just slightly, declining less than 1% to $302.0 million. Operating expenses fell by 3%, as SG&A fell while advertising and marketing increased. With a very strong Q4 that year, with adjusted EBITDA of $5.2 million, the company posted $5.4 million in adjusted EBITDA for the year. This compares to an adjusted EBITDA of -$10.6 million in the prior year.

Looking at FY26 so far, through Q3, which ended in December, Direct to Consumer revenue has declined 16%, including a 28% decline in Toys and Accessories to $145.9 million and a 13% decrease to $95.6 million for Consumables. Gaining was the very small BARK Air, which increased 129% to $9.3 million. The bulk of revenue has been from Direct to Consumer, which has declined by 21% in FY26 so far to $250.9 million. The remaining revenue is from Commerce, and it has increased by 8% to $57.4 million. The gross margin has been 60.9%, down from 62.0%, and the operating loss has declined slightly to $28.0 million.

One thing that I like about BARK is the balance sheet. It ended Q3 with cash of $21.7 million and had no debt. The company paid debt of $42.9 million during the fiscal year. It did have a $35 million line of credit. Equity was $81.2 million. Operating cash flow has been -$21.8 million

For FY27, analysts currently project that revenue will increase 2% to $414.3 million, though EPS will remain negative, improving from -$1.70 to -$0.70. For FY28, a single analyst projects $1.40 as revenue increases 7% to $444.4 million. Adjusted EBITDA is projected to be $4.1 million in FY27 and then $9.4 million in FY28.

BARK Is Near an All-Time Low

BARK had a rough 2025, falling 28.1%, but it is down a lot in 2026 too:

Ending 2025 at $12.05, it shot up towards $20 (which was $1.00 at the time, before the reverse-split) after the company received a bid from Great Dane (discussed below). More recently, the stock gapped down on March 20th and hit an all-time low of $8.15 in April. It is up only marginally despite the strength in small-cap stocks since then. The reverse-split likely caused some selling.

Looking at it relative to CHWY and WOOF, it has substantially underperformed both of them over the past five years:

Over the past six months, BARK has dropped 36.8%, while CHWY has declined 37.9%.

BARK Seems Cheap

BARK is very beaten up. It's not the only company that went public through merging with a SPAC that has declined, and it's not the only company that saw a boom post-pandemic in its growth and in its shares only to see weakness after that. The stock, currently at $8.96, has a market cap of $77 million, which is slightly below book value. Peer CHWY trades at 17.7X book value. Great Dane Ventures, which includes founder and CEO Matt Meeker, bid $0.90 at the time ($18.00 after factoring in the reverse-spit) on January 9th that was non-definitive, and GNK Holdings LLC and Marcus Lemonis bid $1.10 a few days later ($22.00 factoring in the reverse-split). Meeker withdrew from Great Dane in early March, and the preliminary non-binding bid was discontinued. On March 20th, BARK rejected the bid from GNK/Lemonis. This reverse-split took place on April 1st.

While price to book value helps quantify downside risk, most investors are looking at metrics like PE ratio or enterprise value relative to adjusted EBITDA or revenue. The enterprise value of BARK is just $56 million, and this is very low relative to its revenue (less than 0.2X). CHWY trades at about 0.6X. Looking at BARK relative to EPS is tough due to negative EPS, but the projected adjusted EBITDA for FY2028 of $9.4 million, if hit, would leave the company very cheap at its current valuation.

BARK Is a Buy

While removal from the Russell 2000 could further pressure the stock, it is very beaten up and makes sense here trading below tangible book value. What will make it work, in my view, is continued improvement in profitability, which could actually see adjusted EBITDA go positive. Less of a cash burn would help too. My target for a year from now is based on tangible book value, currently at $79.5 million and likely to fall somewhat (perhaps $72 million a year from now). I envision the stock trading at 1.5X, which would be $108 million, which works out to $12.50. This is 39.5% above the current price.

While I think BARK looks pretty good from a chart and a valuation perspective, there are some things that concern me. First, it has been losing money for several years, and it may continue to do so. Second, there are not that many analysts following it yet, and this very low market cap, while potentially "cheap", reduces the number of investors that might be interested. Third, if the economy goes into a recession, it could pressure BARK customers. The CFO announced his exit the company (as of April 17th) during fiscal Q4, and that may be a negative.

We have already seen some potential interest in M&A, and it could come back at this lower price. Petco or Chewy are both partners to BARK and are both substantially larger. Either one of them might become a buyer of the company.

Conclusion

I think that BARK looks attractive here. While the removal from the Russell 2000 may lead to some selling, it has been sold down in price substantially already.

Comments

Log in or sign up to join the conversation.