Central bank meetings, third-quarter GDP releases and October data releases from China and India – all make it a pretty busy week in Asia.

More central bank meetings

Among the Asian central banks, Thailand’s central bank finally gave in to easing pressure this week with a rate cut, but the Malaysian central bank continues to defy easing despite the increasingly weak state of the economy. Then there is New Zealand's central bank and the Philippines too, which both meet next week and both arguably near the end of their respective easing cycles. Perhaps ‘pause’ would be a better description than 'end' for these cycles, as both central banks may need to reassess the effects of their easing so far, while external uncertainty from the trade war between China and the US continues to linger.

For now, the policy pause may be justified on prospects for a Phase one of the trade deal, though that signing has now been pushed out to December from the much-touted mid-November schedule, reducing future certainty still further.

Pause, or out of policy space?

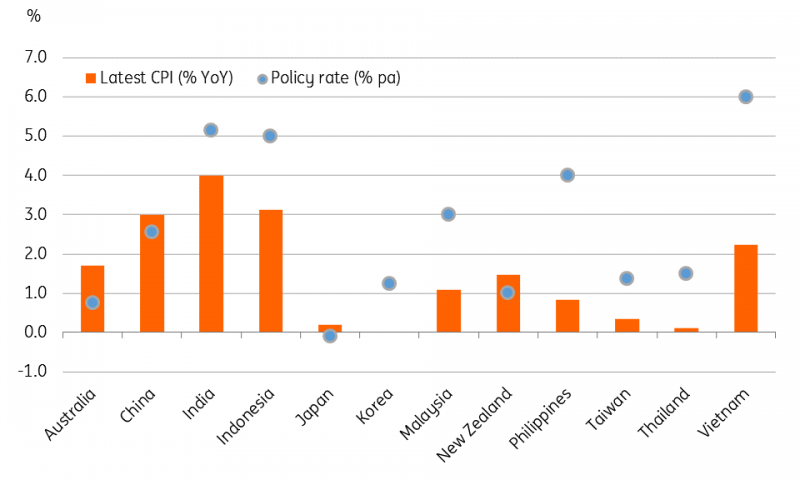

The key question is whether Asian central banks are left with any policy space in the event things really go south again.

Some of them have that space as reflected by their still-high real interest rates (Indonesia, Malaysia, Philippines, or Vietnam), while others have nearly exhausted it and, barring a significant economic deterioration ahead, are likely to stay on hold.

However, as our Asia Chief Economist Rob Carnell opines today, "... if we have learned anything from the period running up to and following the global financial crisis, it is that what we may have considered barriers to policy in the past no longer apply. Perhaps we should no longer consider negative real rates the "floor" to policy in Asia."

Any more space for monetary easing?

(Click on image to enlarge)

Source: Bloomberg, CEIC, ING

But, where is growth?

While it may be fair to say that the Asian central banks easing cycle has almost troughed, for now, there is little evidence of whatever easing they have implemented so far, actually has helped growth.

As the noise around a trade deal continues, Chinese data will be gleaned for the economy’s growth prospects in the current quarter. Our Greater China Economist, Iris Pang, sees some pick-up in momentum and has recently revised the 4Q growth forecast higher, but it all depends on a trade deal materializing.

Lots of data from India will likely bear out the continued weak growth trend, while inflation rising past the central bank’s 4% target reduces room for easing. Does the inflation target matter? We don’t think so. We see one more 25bp RBI rate cut in December.

Indonesia's GDP growth remains stuck at the 5% rate it’s been on since 2014. This is despite 100 basis points of central bank rate cuts. The October trade figures are unlikely to display any vigor coming into the final quarter of the year. In the Philippines, growth gained some traction in the third quarter, though that was all about pent-up government spending (due to the delayed budget) rather than monetary easing which, in fact, failed to pull investment growth out of the negative territory. Still, that's enough of a reason for the BSP to pause for now.

Japan and Malaysia report their 3Q GDP figures. Japan’s growth probably got a boost from the front-loading of spending before the consumption tax hike in October. That’s indeed going to be transitory. In Malaysia, an accelerated export decline probably dragged GDP growth lower, ending the economy’s relative outperformance in the first half of the year. We think this is a good enough trigger for the central bank to utilize some of the policy space it has at the next meeting in January.

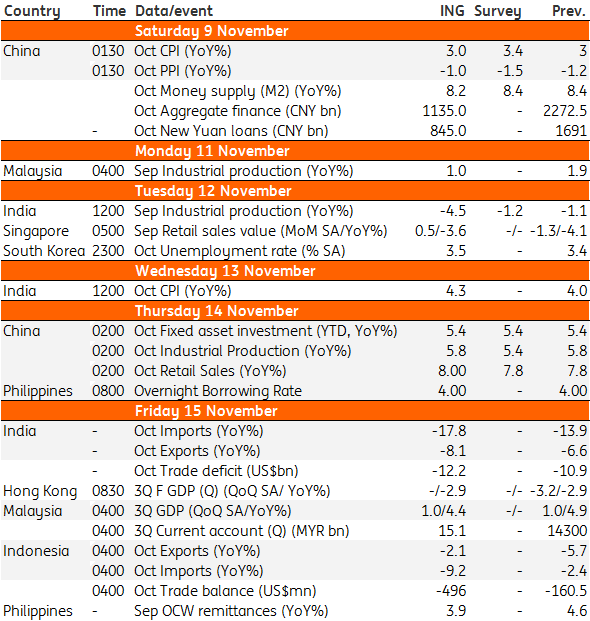

Asia Economic Calendar

(Click on image to enlarge)

Source: ING, Bloomberg, *GMT

Comments

Log in or sign up to join the conversation.