It seems that inflation has returned in many parts of the world. The Eurozone countries have pulled themselves out of a deflationary cycle of recent years and now are recording modest consumer price increases. The ECB is under some pressure from the Germans to prepare to exit from QE---- deflation has been vanquished so it seems. Japan, beset by falling prices for more than two decades, is now showing some glimmer of rising prices. The recovery in global commodities and the weakness in the yen have given the Abe government a shot in the arm in meeting its inflation goals. Lastly, the United States is now coming closer to meeting the Fed’s 2 per cent target. The Fed feels more confident that it can continue to increase the funds rate in an orderly fashion this year.

Certainly, the equity markets concur with the view that growth and inflation will pick up considerably in 2017 and 2018. The so-called “reflation” trade ---- the belief that deflation is dead and the world economies are growing again---has been touted by equity analysts as they position their clients to take advantage of greater profits.

The question is just how sustainable is inflation?

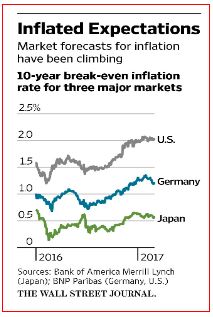

Inflationary expectations are clearly on the rise. A good measure of expectations is the 10 –year breakeven inflation rate. Since the U.S. presidential elections, inflationary expectations have risen ever where (Chart 1).

Chart 1 Inflationary Expectations

Actual inflation numbers have been influenced greatly by the higher prices for oil. Oil hit a 13 –year low in January 2016 and is now nearly doubled. Hence, the year-over-year comparisons are greatly influenced by this low starting point. If inflation is to accelerate it is not likely to be the fault of rising oil prices, since that market appears to be settling in at the current prices of $52-55 /bbl. The source of future inflation must come from other arenas.

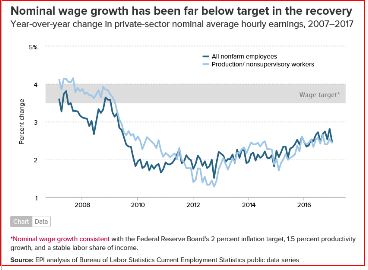

Inflation, especially if it is persistent, usually has a strong wage pressure component. Worker’s compensation can reach as much as 80 per cent of the cost of production. Any sustained increase in wages will eventually work its way into the overall cost of production and ultimately into higher final sale prices.

Nominal wages in the United States have improved, albeit slowly and somewhat inconsistently (Chart 2). Private sector wage growth has bounced around the 2-2.5 per cent range since 2008 and is nowhere near approaching the growth rates in the pre-crisis years. Despite an unemployment rate of less than 5 per cent, the wage sector has largely stagnated. Many reasons abound for the lack of wage pressure, such as greater automation, competition from lower wage economies and lower productivity growth. Whatever the cause may be, there is no apparent real pressure on the wage front.

Chart 2 Nominal Wage Growths in the United States

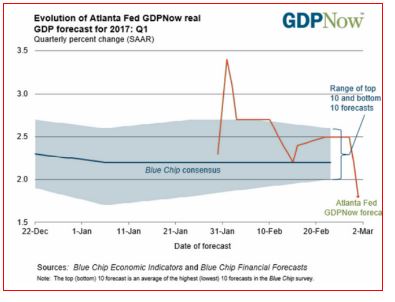

There has been a lot of “soft” data driving the optimism regarding higher prices. Surveys of consumer sentiment and business intentions are all on the upswing. However, the hard data, that is, actual production and consumption numbers tell a different story. The Blue Chip Consensus forecast anticipates GDP growth in the 2.0-2.5 per cent range (Chart 3). The Atlantic Fed’s forecast, based on existing data, is now anticipating that the first quarter of 2017 will be less than 2 per cent, not much better than all of 2016. From a pure growth perspective, it is hard to find reasons to argue that inflation is back and here to stay.

Chart 3 Blue Chip Consensus Forecast

The bond market is one place that does not buy into the reflation trade. The U.S. yield curve ----the relationship between short –term and long-term yields---- has flattened considerably. The difference between the 2 and 30-year Treasury yields stands at 176 bps, not far from its historic low of 146 bp. The 10- and 30- year segments of the curve are most sensitive to inflationary expectations. At this time, those buying long-dated bonds are far from convinced that the recent run in consumer prices will stick. For many bond holders, the factors that pushed yields down to the ground are still operating. Ironically, this low cost of funds contributes to the rally in stocks and commodities, when, in fact, the bond market is saying quite the opposite regarding the economic outlook.

Too much of the inflation optimism rests on the Trump administration enacting its pro-growth policies. While equity markets are buoyed by the prospects of de-regulation and tax cuts, there is so little evidence of specific policies and spending plans to justify this euphoria. The jury presiding on the inflation case is still out deliberating.

Comments

Log in or sign up to join the conversation.