I have been following Adobe (ADBE) on my watchlist for stocks since March, after it plunged following its Q1 report and a bit after the meltdown in software stocks that prompted me to write about State Street SPDR S&P Software & Services (XSW), which in late February I had rated as a Buy.

Well, since I initiated coverage of XSW, which I downgraded to Hold in May, it has increased by about 8%. ADBE, which just reported its Q2, has declined by 27% since then to a multi-year low. There has been a lot written about Adobe recently, and I think that even those that are bearish do acknowledge that the stock appears to be very attractive in terms of valuation. I have not been so bullish on the stock, but I have been and remain bearish on stocks broadly, especially Technology stocks. I did own ADBE briefly after the report and I want to explain why I like it and to share something that the company should do to broaden its investor base.

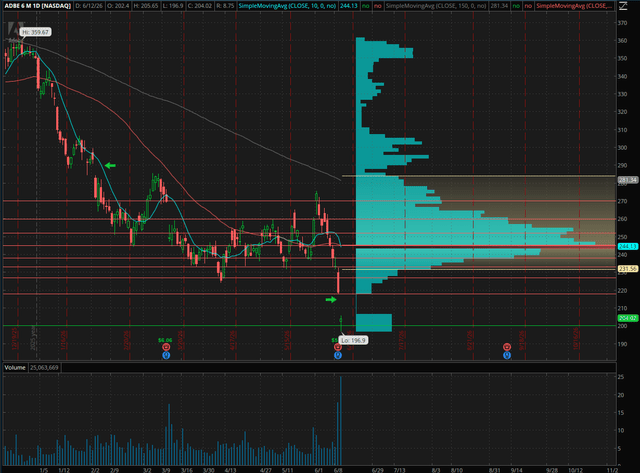

ADBE Has Plunged

Adobe has sold off 41.7% so far in 2026, well behind the advance of the market. Here is a look at the last six months:

The stock gapped down after its Q2 earnings report that came out after the close on Thursday. The stock traded below $200 and bounced, closing at $204.02, down almost 15%. The stock had gapped down in March, when it reported its Q1, though that gap was filled in June. There is an open gap from early February that remains open.

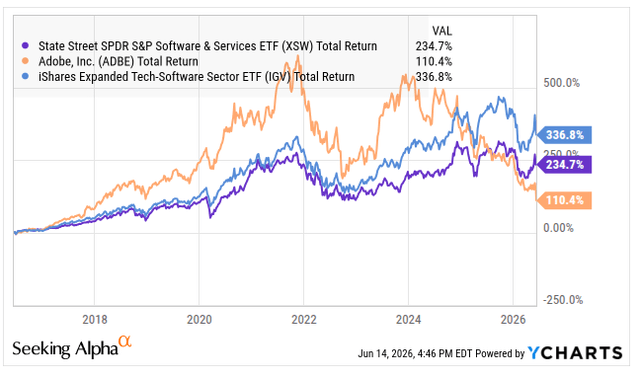

Looking at the past 10 years, ADBE has provided a total return of 110% (7.7% annual compound growth), but this has lagged XSW as well as the iShares Expanded Tech Software Sector ETF (IGV):

Of course, it lags greatly the S&P 500, which has increased 319% with dividends over the past decade.

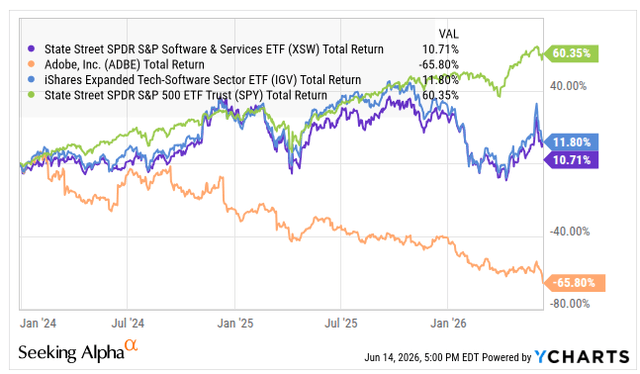

Looking at action since the end of 2023 paints a much uglier picture, as software has greatly underperformed the S&P 500, while ADBE has been crushed:

Adobe Does Face Some Challenges

The company did not miss on the revenue or earnings expectations for Q2, but it does face some big obstacles. The CEO, Shantanu Narayen, announced that he is retiring on March 12th, when the company reported its Q1 financial results. He has been CEO for 18 years. The company is looking for a new CEO, and Narayen will remain Chairman of the firm, a role he holds in addition to CEO.

On Thursday night, when the company reported financials for Q2, it announced that the CFO has left to take a job as CFO of Marvell (MRVL). Dan Durn announced that he will exit on June 15th. Durn served in the role for four years after joining Adobe in 2006.

Management change at the senior level can be a yellow flag or even a red flag, and too see the CEO and the CFO depart as the stock has been so weak can leave investors cautious. Adobe and all software companies face both risks and opportunities related to artificial intelligence. How will Adobe fight competition from AI? it really depends upon who the new CEO will be.

Another challenge has been the share repurchases. I think that having a lot of cash and a cheap stock can be a recipe for a company using that cash, but taking on debt to buy stock can be risky. Adobe has been very aggressive on repurchasing its stock. The good thing is that it used cash and did not take on debt. The bad thing is that it paid a very high price. Of course, in hindsight, this is very easy to say after a stock crashes, but I never thought that the valuation the company was buying its stock at was attractive. In FY25, the company spent about $2.5 billion repurchasing 7.2 million shares in fiscal Q4 at a price of about $343. During the entire fiscal year, it spent $11.28 billion repurchasing stock. This was after a decision in March 2024 to buy back up to $25 billion of stock before March 14, 2028. There was $5.9 billion that remained authorized to repurchase as of late 2025.

The Q1 10-Q revealed that the company had bought 8.1 million shares during Q1 at prices that averaged $305.86. The overall dollars spent was similar to Q4 at just under $2.5 billion. The company had $3.89 billion that remained authorized. The company has not yet released its 10-Q for Q2, but the press release for its Q2 financials stated that the company did repurchase 8.5 million shares during the quarter. On April 21, the board authorized an additional $25 billion of share repurchases through April 2030. At the end of Q2, the company reported cash and short-term investments of $6.9 billion but debt that totaled $5.4 billion. For the company to buy additional shares of stock without creating net debt, it must limit itself to free cash flow, which in FY25 totaled almost $10 billion.

ADBE Is Cheap

As bad as the stock has been performing, some might assume that the reported financials have been worse than expected. This has not been the case. The company provided financial targets in March for Q2, and this included total revenue of $6.48 billion to $6.48 billion, and the company reported revenue in Q2 of $6.62 billion, up 13% from a year earlier and ahead of its internal forecast. EPS had been guided to be $5.80-5.85 on a non-GAAP basis, and ADBE reported non-GAAP EPS of $5.96.

Adobe provided financial targets last week too for the quarter ahead and for the full year, and it expects full year revenue to be $26.5 billion to $26.6 billion with EPS of $17.90-18.00 on a GAAP basis and $24.35-24.45 on a non-GAAP basis.

Analysts currently project that FY26 revenue will $26.43 billon, up 11%, with revenue expanding by 9% in FY27. Non-GAAP EPS are projected to rise 16% in FY26 to $24.33 and then pick up 13% in FY27 to $27.37.

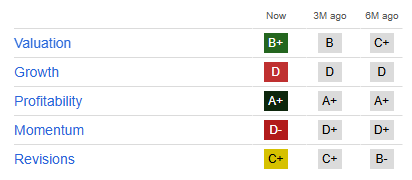

Seeking Alpha has a Quant Rating for ADBE of 3.38, which is a Hold. The rating is helped by valuation and profitability but weighed down by the very poor price momentum as well as growth, which reflects slower growth than peers for EBIT and EBITDA on a forward basis.

On a trailing basis, ADBE, at $204, trades at a PE of just 9.7X for FY25. On a forward basis, it trades at just 8.4X. Not bad for a company with no net debt!

Adobe ended Q2 with book value of $11.4 billion, and it has negative tangible book value due to intangibles and goodwill totaling $13.3 billion. Negative tangible book value concerns me for companies with a lot of debt, especially if they are losing money and burning cash, but ADBE is not in that position.

Adobe is a Magic Formula Stock

Joel Greenblatt, who runs Gotham Asset Management and is a professor at Columbia University, wrote a book in 1997 with a very long title: "You Can Be a Stock Market Genius (Even if You're Not Too Smart): Uncover the Secret Hiding Places of Stock Market Profits." Greenblatt, who was a very successful hedge fund operator (Gotham Capital), wrote a book that was even more popular, "The Little Book That Beats the Market" in 2005 and updated in 2010 about magic formula investing.

Adobe is a "Magic Formula" stock. What this means is that it has high Earnings Yield (EBIT divided enterprise value) and high Return on Capital. The book suggests taking a universe of stocks and ranking them by Earnings Yield and Return on Capital . To get the final rank of a stock by the magic formula, the ranks are added to each other and then compared. This suggests that the weighting is 50/50 between Earnings Yield and Return on Capital.

Every single day, a list of magic formula stocks changes. Why? Prices change daily! Gotham Asset Management provides a stock screener on its website that allows visitors to get a current list of the top magic formula stocks:

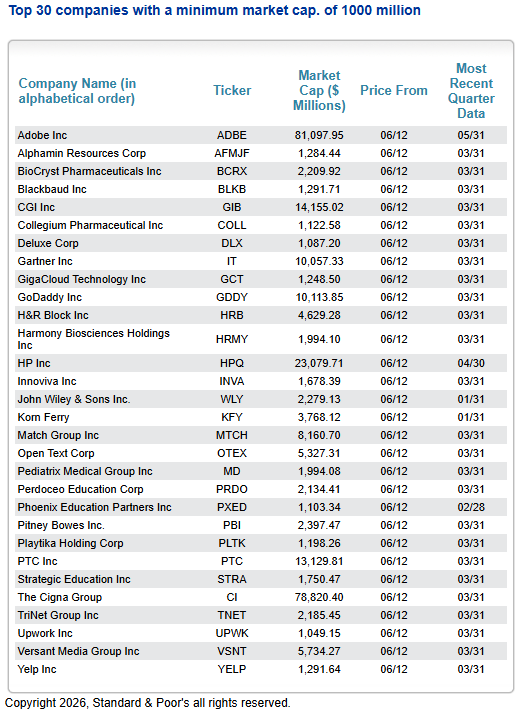

Visitors must register, but it is free of charge. In the book, Greenblatt suggests buying at least 20 stocks, and the website lets visitors get a list of the top 30 or the top 50. Adobe does qualify for the top 30 for stocks above $1 billion in market cap:

Adobe is the largest stock by market cap on the list by far. If one expands the number from 30 to 50, several larger stocks do enter.

The top 50 Magic Formula stocks above $50 billion in market cap have market caps as high as $4.9 trillion and average $365 billon with a median market cap of $125 billion. So, Adobe is one of the smaller companies that makes this list. According to Koyfin, the EV/EBIT is 6.8X, one of the very lowest valuations that range from 5.1X to 28.1X with an average of about 15X. The PE is very low too relative to the other 49 stocks that trade near 18X.

Why I Rate ADBE as a Buy

So, Adobe appears to be cheap, and it has a strong balance sheet. I shared the estimates for EPS above, and my target for year-end is based upon a PE of 11X FY27. This works out to be $301. It could get a higher multiple, but perhaps the EPS estimate, which has been rising, could fall. I think that this is a very conservative outlook, and it suggests a return over the next six months or so of 47.6%. This level is stellar compared to what the overall market returns are likely to be.

What Adobe Should Do

Going back to that list of 50 stocks with market caps above $50 billion, 46 of the 50 pay a dividend. Adobe is one of the four that don't. All four of these stocks are down sharply in 2026. Here are the total returns:

The overall list of 50 stocks has increased an average of 4.4% with a median return of 2.7%, so these stocks are lagging the S&P 500. The average dividend yield for the 50 stocks is 2.2%, with a median yield of 2.1%. Technology and Energy are the two leading sectors by far in 2026, and there are 10 Technology stocks (20%) and just 1 Energy stock (2%). Both of these are smaller than the amounts of these sectors in the S&P 500.

While most investors don't care necessarily about dividends and dividends are not tax-efficient, as they are taxable for shareholders who hold the stocks in a taxable account, there are a great number of people who do focus on dividends. There are also some very large dividend-focused ETFs and mutual funds that can't buy stocks that pay no dividend, which is the case for Adobe.

While I do not expect Adobe to necessarily begin paying a dividend, I believe that doing so would open new potential investors to the name. Buying all of that stock did not help prevent the collapse in the price, and, going forward, the company should maybe be less aggressive in its share repurchases, suing some of its free cash flow for dividends.

If it were to pay 25% of its cash flow from operations in the prior year initially, this would be $2.5 billion, which amounts to a little over $6.00 per share per year ($1.50 per quarter). The yield would be over 3%, which would stand out, especially with such a low valuation.

Conclusion

I am very bearish on stocks right now, but I do like Adobe. I am rating it a Buy, and I have shared why. I have also discussed something that it could do that would lead to me raising it to Strong Buy. I hope that the new CEO and new CFO will consider using a portion of their cash flow for dividend payment.

Comments

Log in or sign up to join the conversation.