Stock markets have become more dynamic over the years, changing virtually every rule in the book. Decades ago, the most popular ways of investing were via initial public offerings (IPOs) and the net-net method of picking undervalued stocks in the secondary market. Few investors bothered with the complexity and implications of doing thorough fundamental, macro and systemic analysis on stocks before investing.

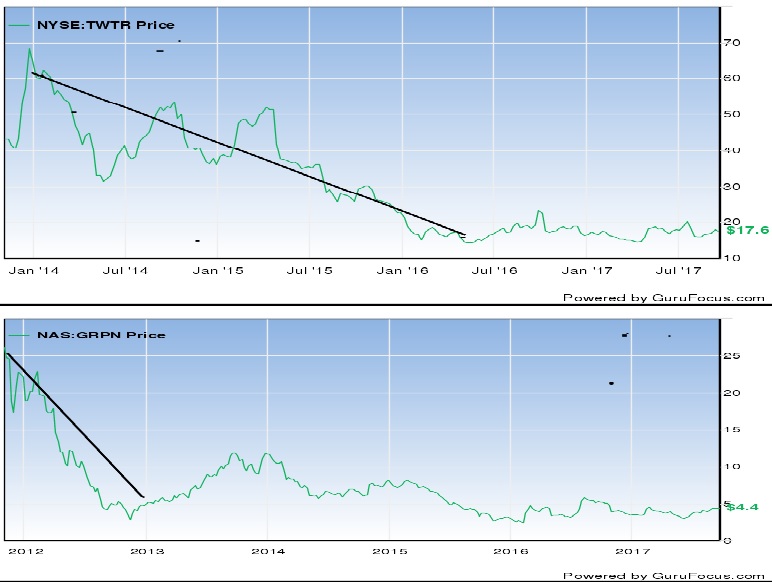

But today the markets are bombarded by legions of short-term investors that are out to capitalize on volatility. So, where does this leave the long-term or long-only investors looking for opportunities that are suited to retirement investing? In today’s markets, not every IPO is a winner. I can point to a few examples like Twitter (TWTR ) and Groupon (GRPN ), which looked promising before going public but proved otherwise a few months after listing:

Based on the price trends demonstrated in these charts, anyone betting on those two IPOs would have lost significantly, bar those who sold shortly after the listing. But that’s not the way of long-term investing. So, where does this leave our retirement investing community? Well, if you closely follow the opinions of some retirement investors, then you will see that one characteristic they have in common is adaptability to modern markets. This means that retirement investors can no longer restrict themselves to one investment strategy.

Retirement investors are now adapting their strategies to modern stock trading techniques. They are diversifying their portfolios to include assets from global markets and are not afraid to invest in stocks that promise future growth.

Generally, most growth stocks make good retirement stocks, and dividend stocks are some of the best in class. So, if a stock pays good dividends and seems to increase the dividend amount periodically, then chances are good that said stock will be a reliable growth stock in the long run. However, retirement investors are looking not only at dividend growth stocks, but also stocks that promote growth in the future despite paying no dividends in the present.

These stocks rely on growth driven by potentially disruptive products in their product pipelines, an operational restructuring that results in massive cost cuts, or the overall economic growth of the countries where they draw a majority of their income, among other factors. For instance, some frontier markets have very high GDP growth rates, and emerging markets like China and India boast several times the growth rates experienced in the U.S. and the U.K. Therefore, diversifying your retirement investing portfolio to these markets can help cushion against low returns from modern stock markets.

Another way to diversify a modern retirement portfolio is to invest in different assets. While bonds rank first in the minds of some retirement investors, more and more investors are now mixing up their portfolios to include real estate assets, U.S. bonds, U.S. stocks, international stocks, international bonds and alternatives (e.g., a personal business or commodities), as well as cash.

Then depending on their age and risk appetite, investors allocate distinct levels of investment to the various asset categories to match their goals. A retirement portfolio does not have to rely entirely on fixed-income instruments like bonds and savings because modern stock trading techniques have become widely accepted as a strategy for retirement investing.

In addition, life expectancy levels have increased globally from about 60–65 years in the 1970s to about 75–80 years now, and those who are born today can expect to live well beyond 80 years according to analysts. This means people will need greater savings to cover their protracted life expectancy. As such, taking higher levels of risk in expectation of higher returns is now a more common practice in the retirement investing community.

Conclusion

In summary, there will always be conservative investors who prefer bonds and other fixed-income securities, while the stock market appeals to the less risk-averse as a means of retirement investing.

However, we are beginning to see a bridge between the two investment strategies, coupled with alternative ways of saving for retirement. As always, investors are out to make as much money as possible for retirement, and in recent years that has meant increased activity in the stock market with a specific interest in growth stocks.

Comments

Log in or sign up to join the conversation.