The coming wave of equity supply we detailed in The IPO Boom is growing. Last week, Alphabet executed an $80 billion secondary equity offering to fund AI infrastructure, including a $10 billion private placement to Berkshire Hathaway. Now, the Financial Times claims that Meta, Microsoft, and Amazon are planning similarly large equity raises to fund their 2026 capital expenditures. Add SpaceX’s $75 billion IPO, OpenAI’s $60 billion offering, and more supply coming soon from Anthropic and Stripe, and the equity market is being forced to absorb quite a supply shock.

The hyperscalers’ (Meta, Microsoft, Amazon and Google) preference for issuing equity rather than debt financing is twofold. With 30-year Treasury yields around 5%, issuing debt to fund a decade-long AI infrastructure would entail interest expenses before any meaningful revenue from the investments. Equity financing carries no coupon. From a basic asset-liability matching framework, funding long-duration AI assets like data centers, chips, and satellite networks that will generate cash flows in the out years with equity rather than fixed-rate debt makes sense. With equity, there is no refinancing risk, no interest burden, and no margin pressure. Further, they can buy back the equity by issuing debt when interest rates are lower. However, the cost is dilution to equity shareholders, but at current valuations, that cost is relatively low.

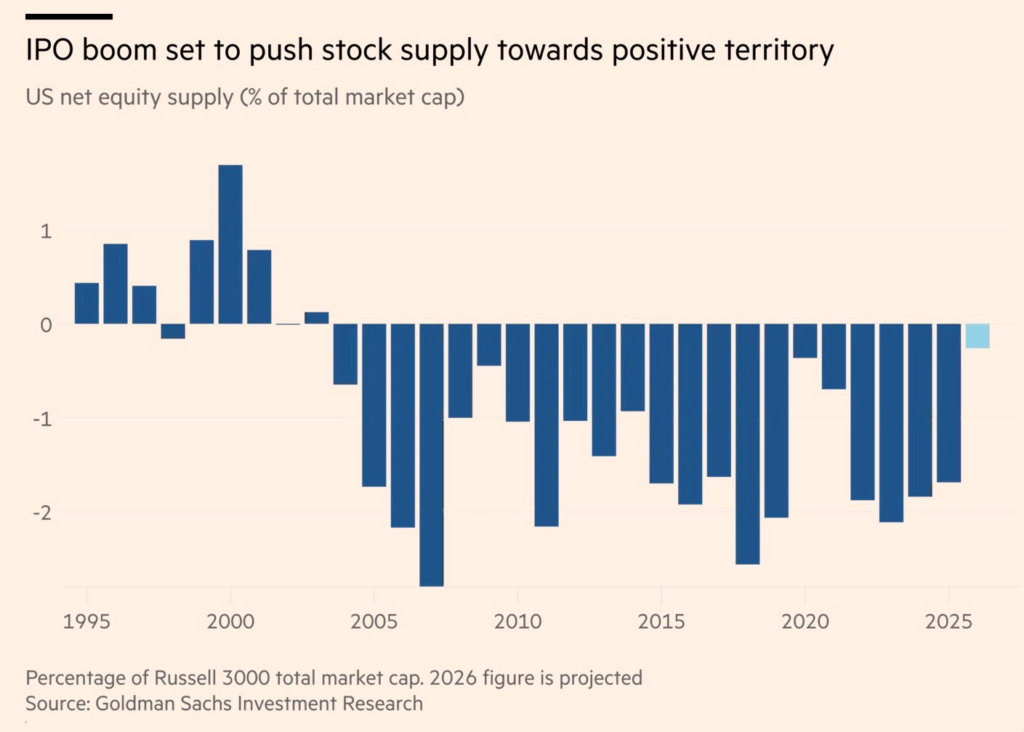

The broader implication is what matters for existing shareholders. Every new share issued by Google, Amazon, and Meta, every IPO allocation absorbed by investors, represents capital redirected away from something that is already owned. The supply will unfold over time, so they are unlikely to create a shock but rather a persistent headwind. The graph below, courtesy of the FT shows expected net (issuance less buybacks) issuance this year. It could easily be the first positive year since 2003.

What To Watch Today

Earnings

No earnings releases today.

Economy

Market Trading Update

All week I’ve described the same tape. The semiconductors fell by more than 9% on Friday, bounced 5% on Monday, then rolled over again on Wednesday. As we noted over the weekend, leverage is the real issue underneath this market, and it’s worth explaining WHY an index this large now trades like a momentum stock. The answer isn’t that the fundamentals changed three times in five sessions. It’s the plumbing.

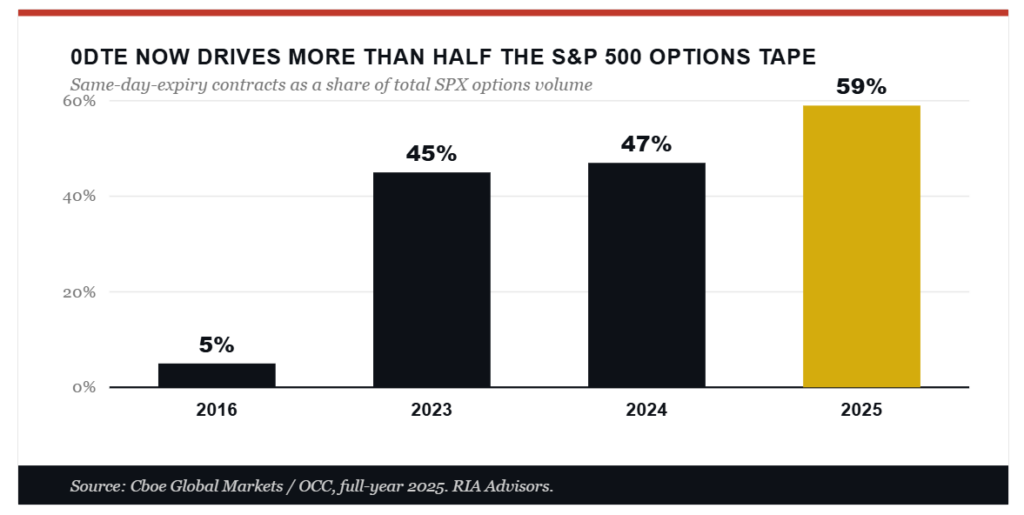

Start with the options tape. In 2025, zero-day-to-expiry contracts made up roughly 59% of all S&P 500 options volume, about 2.3 million contracts a day. Back in 2016, that share was 5%. When more than half the flow expires the same session, dealers hedge in real time, buying strength and selling weakness straight into the close. That mechanic doesn’t start a selloff. It pours gasoline on whatever is already moving, which is exactly why the round trips have been so violent.

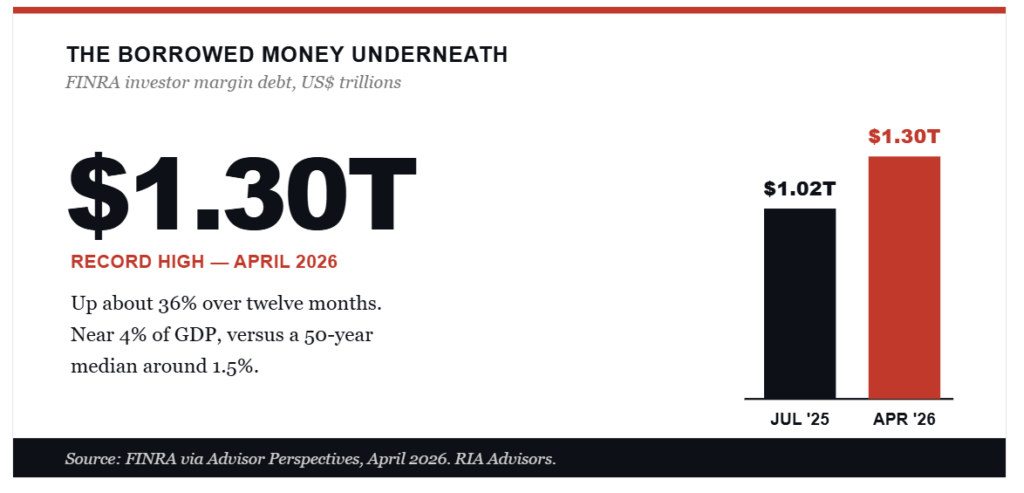

Underneath those options sits a record pile of borrowed money. FINRA margin debt hit an all-time high of $1.30 trillion in April, up better than a third in a year, and now runs near 4% of GDP against a long-run median closer to 1.5%. The retail crowd has fresh tools too. There are about 377 single-stock ETFs now, 276 of them launched in 2025 alone, many of them levered 2x to a single name. The new SpaceX leveraged fund trading Friday is just the latest. Make no mistake, these are accelerants, not investments.

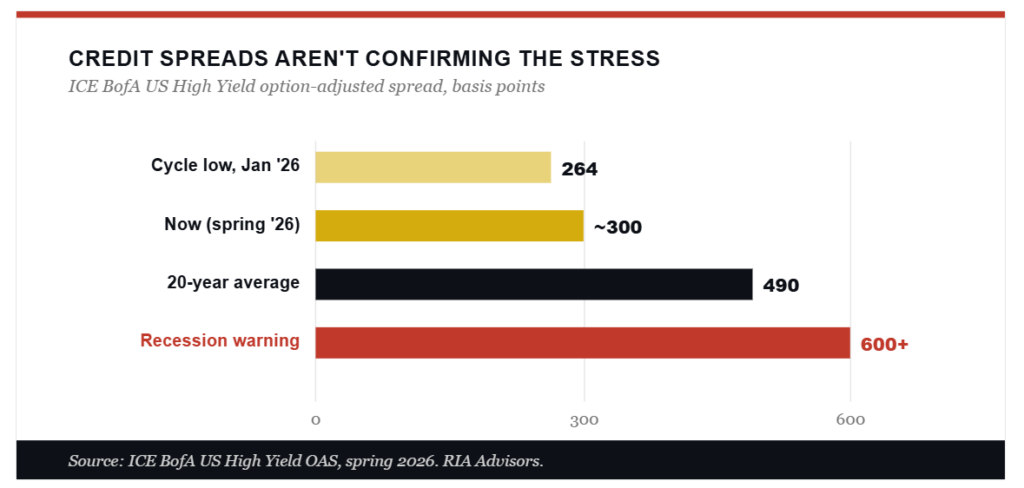

Here’s what should keep you honest, though, because it cuts against the bearish story. If this were the start of something systemic, credit would be screaming. It isn’t. High-yield spreads sit near 300 basis points, close to the tightest since 2007 and a fraction of the 490 average. The bond market is pricing trouble in a few crowded trades, not a credit event. That’s the bulls’ strongest card, and it’s a fair one.

The trouble is what tight spreads and record leverage mean together. They mean there’s no margin of safety left in the system. Howard Marks put it best. The riskiest thing in markets is the belief that there is no risk. When the plumbing is this geared, and credit is this calm, the move to respect is the one that feeds on itself.

The bottom line. Don’t confuse violent with fragile, and don’t confuse quiet credit with safe. Keep your hedges, trim what’s levered, and watch high-yield spreads. As long as they stay calm, this is a structure-driven shakeout. The day credit widens alongside the VIX, the housekeeping becomes something worse.

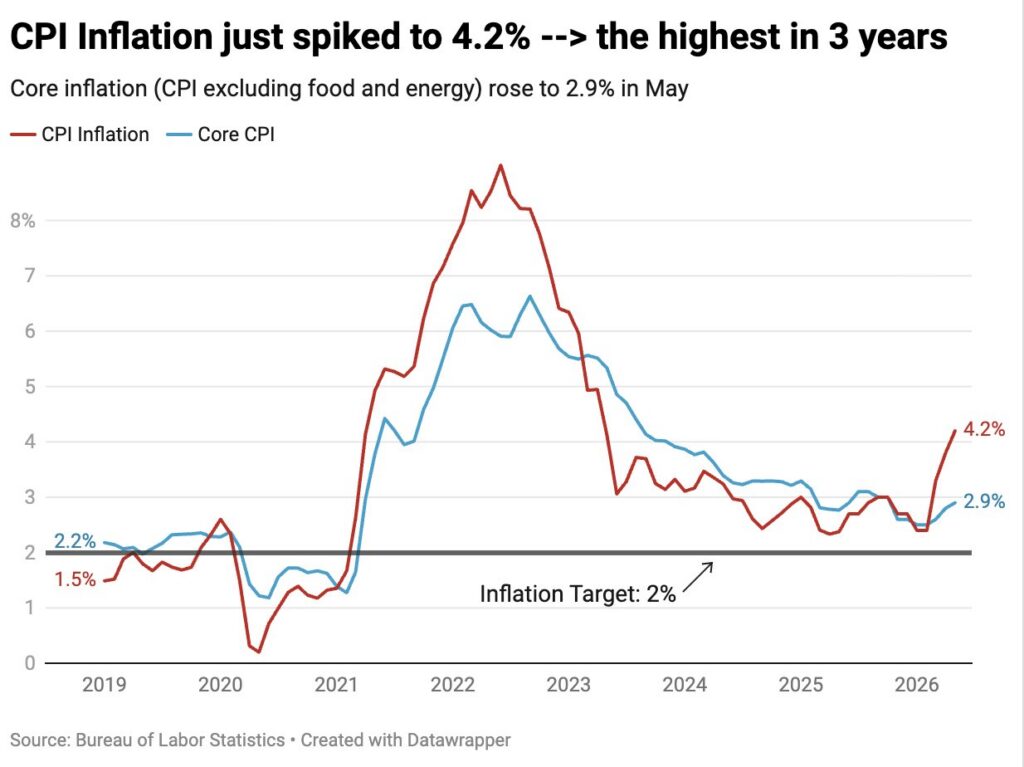

CPI: Optimism Beneath The Surface

Headline monthly CPI rose by 0.5%, in line with estimates. Core CPI only rose by 0.2%, a tenth below estimates. This was the first month since late 2022 that the annual Core CPI was higher than the year prior. Not surprisingly, the impacts of the Iranian War and the closing of the Strait of Hormuz are driving the CPI higher; however, there are signs that underlying inflation is cooling. For instance, Core Goods CPI fell by .11%, the first drop in over a year. Also of note, shelter prices, which account for 40% of the CPI Index, increased by 0.3% over the month, as owners’ equivalent rent rose 0.3% and rental prices rose 0.4%. CPI shelter inflation remains stubbornly above real-world housing inflation, portending a decline in CPI when it catches up. Strip out food, energy, and shelter, and headline inflation is running at 2.4%.

Given the recent improvement in labor conditions and the latest CPI data, it’s highly likely the Fed will leave interest rates alone at next week’s FOMC meeting. That said, the odds are good that the market perceives the Fed as having a hawkish bias, based on the coming FOMC statement and the dot plots. The Fed Funds futures market is already pricing in a 25bps rate increase by year’s end.

Tweet of the Day

Comments

Log in or sign up to join the conversation.