Back in the fourth quarter of 2016, in the immediate aftermath of the 2016 Election, sentiment towards manufacturing in the US surged. Right before the election in October 2016, the ISM Manufacturing index was at 51.7 and eventually rallied all the way to a peak of 60.8 in August 2018. For the last nine months, though, manufacturing sentiment has been falling off a cliff as the impact of tariffs (both actual and threatened put a damper on sentiment. In the latest monthly ISM Manufacturing survey, the headline index dropped from 52.8 down to 52.1 to its lowest reading since October 2016. With this month’s decline, now, 95% of the post-election gains have been re-traced.

(Click on image to enlarge)

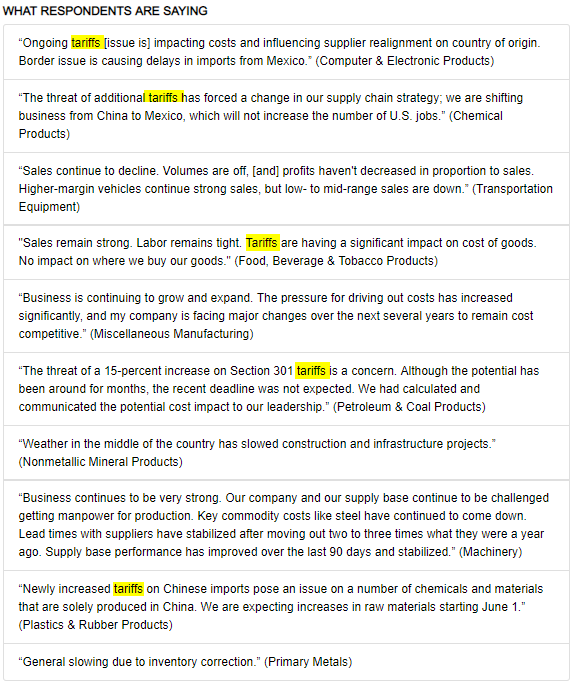

As just an example of how tariffs are impacting sentiment, take a look at the commentary section of this month’s report. Of the nine comments included in the section, five cited tariffs as an issue. The second comment was especially notable where a respondent from the Chemical Products industry said that tariffs in imports “…will not increase the number of U.S. jobs.”

(Click on image to enlarge)

As far as the breadth of this month’s report is concerned, the subcomponents were evenly split between gains and losses relative to April’s levels, but the majority were down relative to where they stood last year at this time. The only two that showed increases were Business Inventories and Customer Inventories. On the downside, Production, New Orders, Backlog Orders, Supplier Deliveries, and Prices Paid all saw double-digit declines. Prices Paid has been a real notable decliner, dropping more than 25 points from where it was last year!

(Click on image to enlarge)

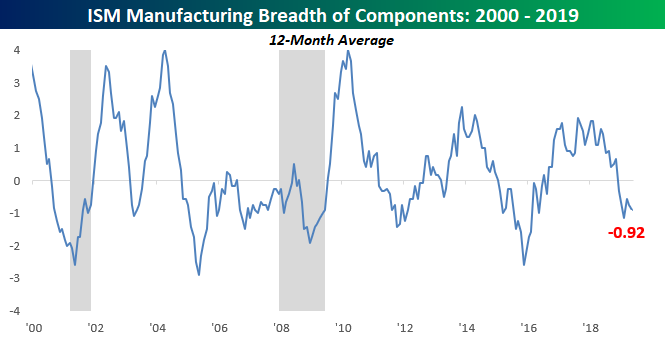

Looking at how breadth in the individual components of the ISM Manufacturing report has trended over time, the chart below shows the net number of components showing m/m increases on a 12-month average basis. Through May, the 12 month average for the Manufacturing sector was negative -0.92, which surprisingly isn’t the weakest reading we have seen in the last few months. So, at least the pace of decline doesn’t still appear to be accelerating.

(Click on image to enlarge)

Comments

Log in or sign up to join the conversation.