Why Bonds Aren’t Overvalued

Doug Kass wrote a very interesting piece this week on the bond market:

“As overvalued as I believe the U.S. stock market may be, fixed-income instruments may be even more overvalued.

Yesterday the 10-year note was yielding 2.21% — the lowest yield since last Nov. 11 — and the long bond’s yield is down to 2.88% after weak core consumer price index (CPI) and retail sales were released on Good Friday, when the markets were closed.

This decline in yield and rise in bond prices may be the last opportunity for a generation to sell fixed-income positions. Indeed, bonds may now represent the single most overvalued asset class extant.”

Before I start getting a bunch of “hate mail,” let me state that I greatly respect Doug’s opinion. In this case, however, I simply have a differing view.

Both Doug and I agree that stocks are indeed overvalued. Since investors pay a price for what they believe will be the future value of cash flows from the company, it is possible that investors can misjudge that value and pay too much. Currently, with valuations trading at the second highest level in history, it is not difficult to imagine that investors have once again overestimated the future earnings and cash flows they might receive from their invested capital.

However, bonds are a different story.

Unlike stocks, bonds have a finite value. At maturity, the principal is returned to the holder along with the final interest payment. Therefore, bond buyers are very coherent of the price they pay today, for the return they will get tomorrow. Since the future return of any bond, on the date of purchase, is calculable to the 1/100th of a cent, a bond buyer is not going to pay a price that yields a negative return in the future. (This is assuming a holding period until maturity. A negative yield might be purchased on a trading basis if benchmark rates are expected to decline further and/or in a deflationary environment.)

Given that bonds are loans to borrowers, the interest rate of a bond, at the time of issuance, is tied to prevailing interest rate environment. In this discussion, we are primarily addressing the 10-year Treasury rate often referred to as the “risk-free” rate.

However, the price of an existing bond, traded on the secondary market, is determined by the difference between the coupon rate and the prevailing interest rate for the type of obligation being considered. The benchmark rate acts as the baseline. Let’s use a very basic example.

Bond A:

- $1000 bond bought at 100.00 (par) with a 5% coupon and matures in 12-months.

- At the end of 12-months Bond A matures. $1000 is returned with $50 in interest or $1050 for a 5% yield.

Benchmark Interest Rate Falls To 4%

- What is the “fair value” of Bond A in a 4% rate environment?

- Since the coupon of 5% cannot be changed, the price must be altered to adjust the “yield at maturity.”

- In this case, the price of the Bond A would need to rise from $100 to $101.

- At maturity of Bond A, the principal value of $1000 is returned along with $50 in interest to the holder.

- Since the new owner paid $1010 for the bond, there is a loss of $10 in value ($1010 – $1000) which equates to a net return of $1000 +($50 in interest – $10 loss in principal = $40) = $1040 or a 4% yield.

Got it?

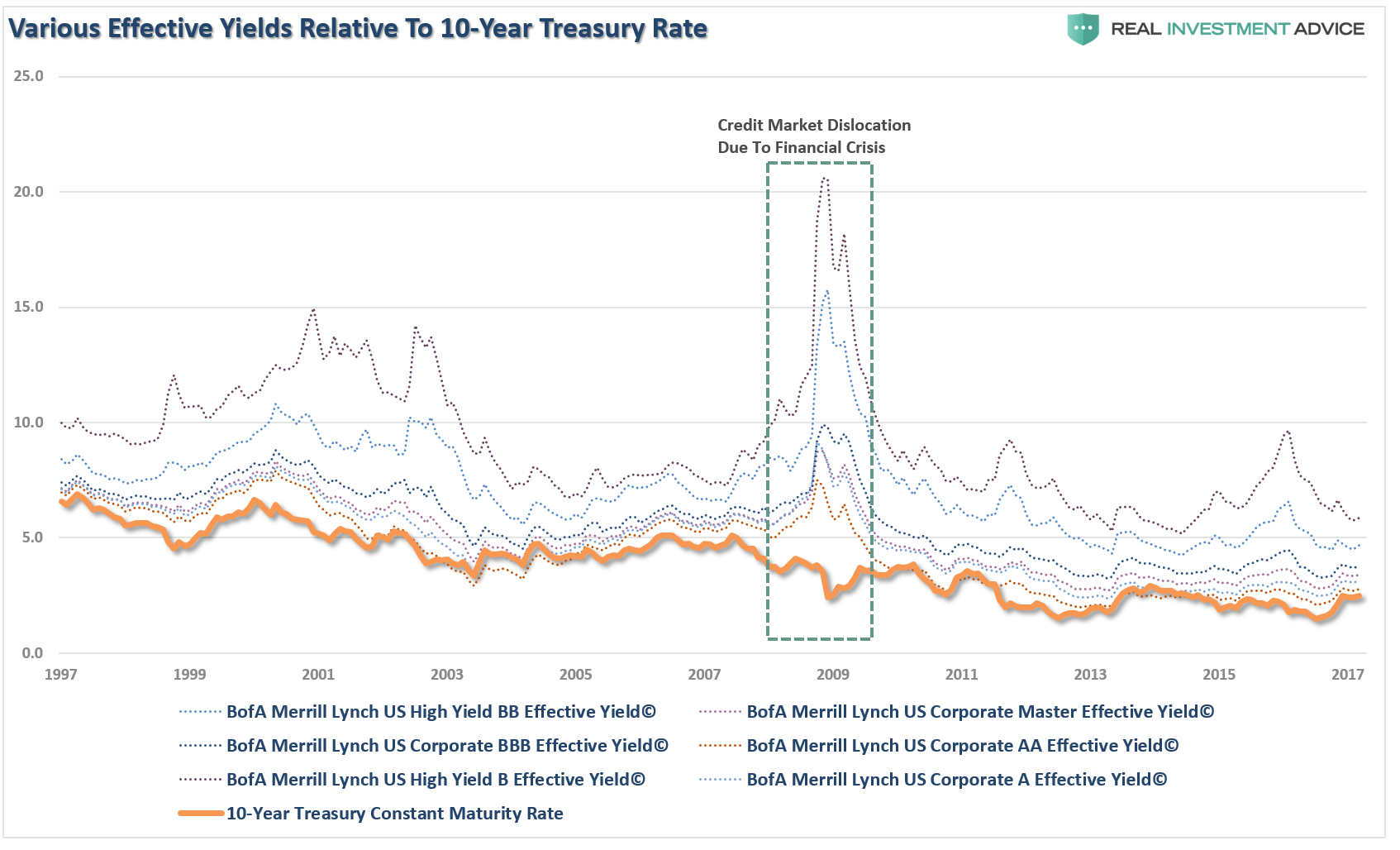

The chart below shows the 10-year Treasury yield as compared to BBB to AA Corporate Bond rates. Not surprisingly, as the credit rating declines the spreads between the “risk-free” rate and the “risk” rate increases. However, with the exception of the bond market freeze during the “financial crisis,” the ebb and flow of yields primarily track the ebb and flow of the “risk-free” benchmark rate.

Since rates are generally tied to a primary benchmark, for bonds to become overvalued the benchmark rate would have to become detached from the underlying metrics that drive the level of borrowing costs.

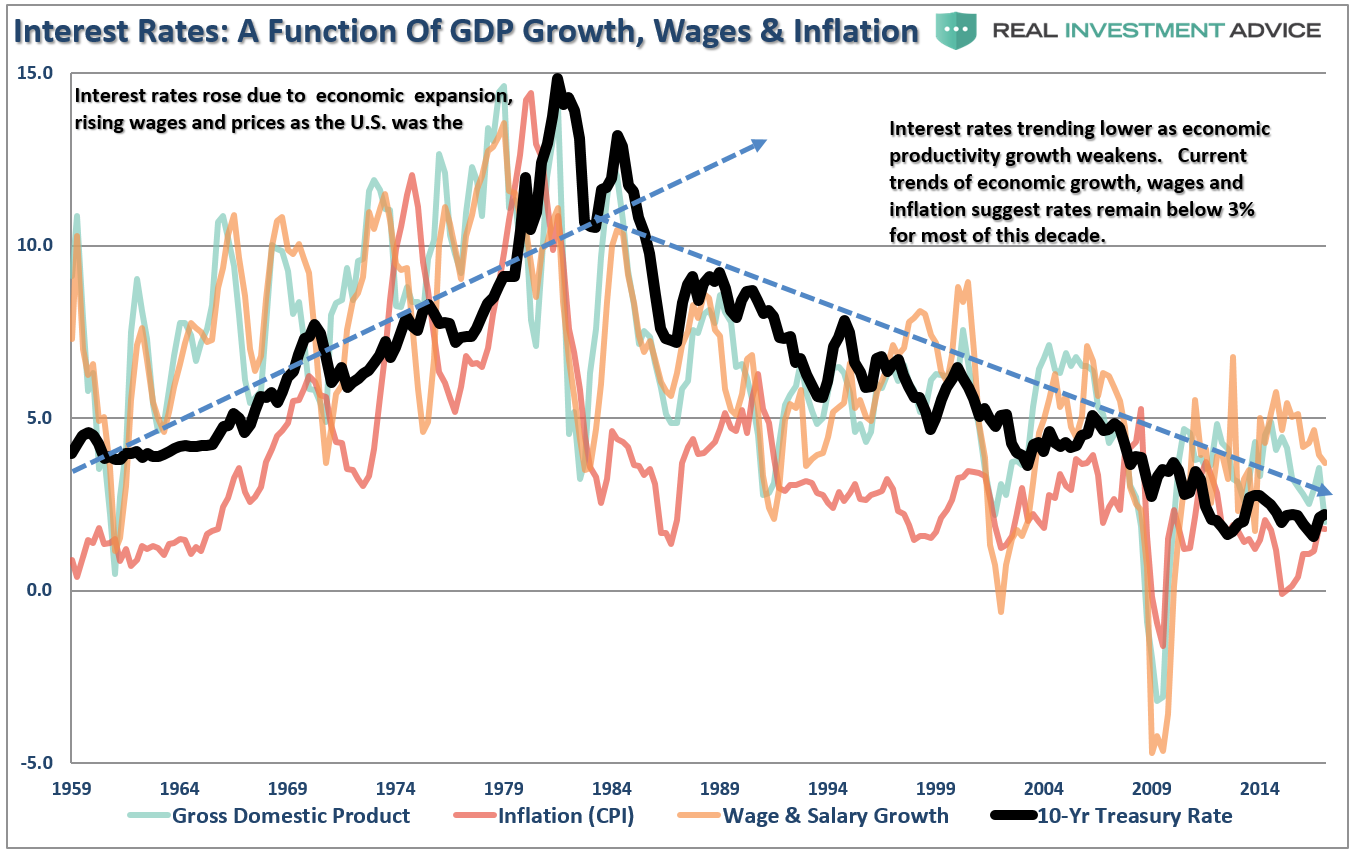

As I have discussed many times in the past, interest rates are a function of three primary factors: economic growth, wage growth, and inflation. The relationship can be clearly seen in the chart below.

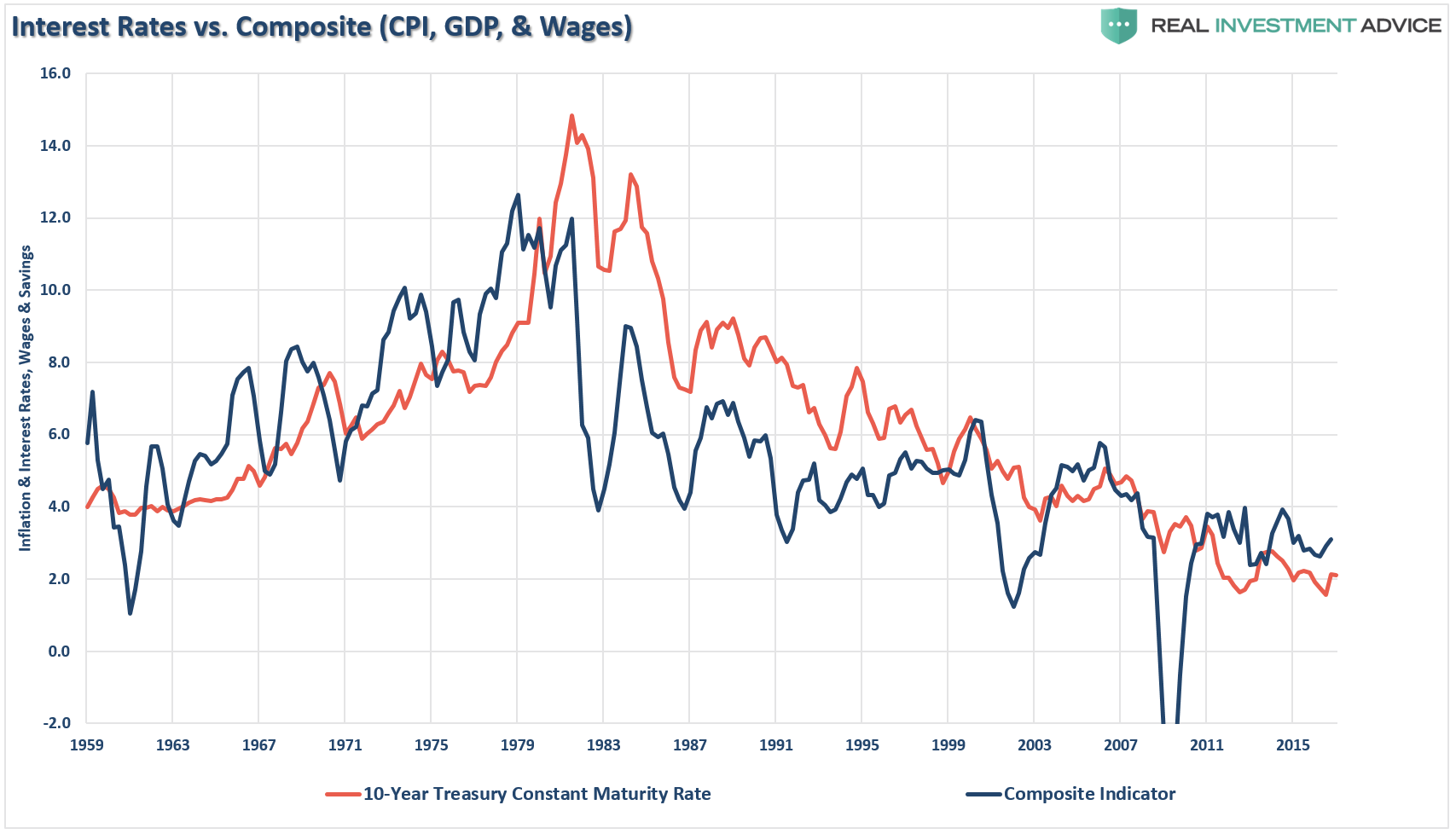

Okay… maybe not so clearly. Let me clean this up by combining inflation, wages, and economic growth into a single composite for comparison purposes to the level of the 10-year Treasury rate.

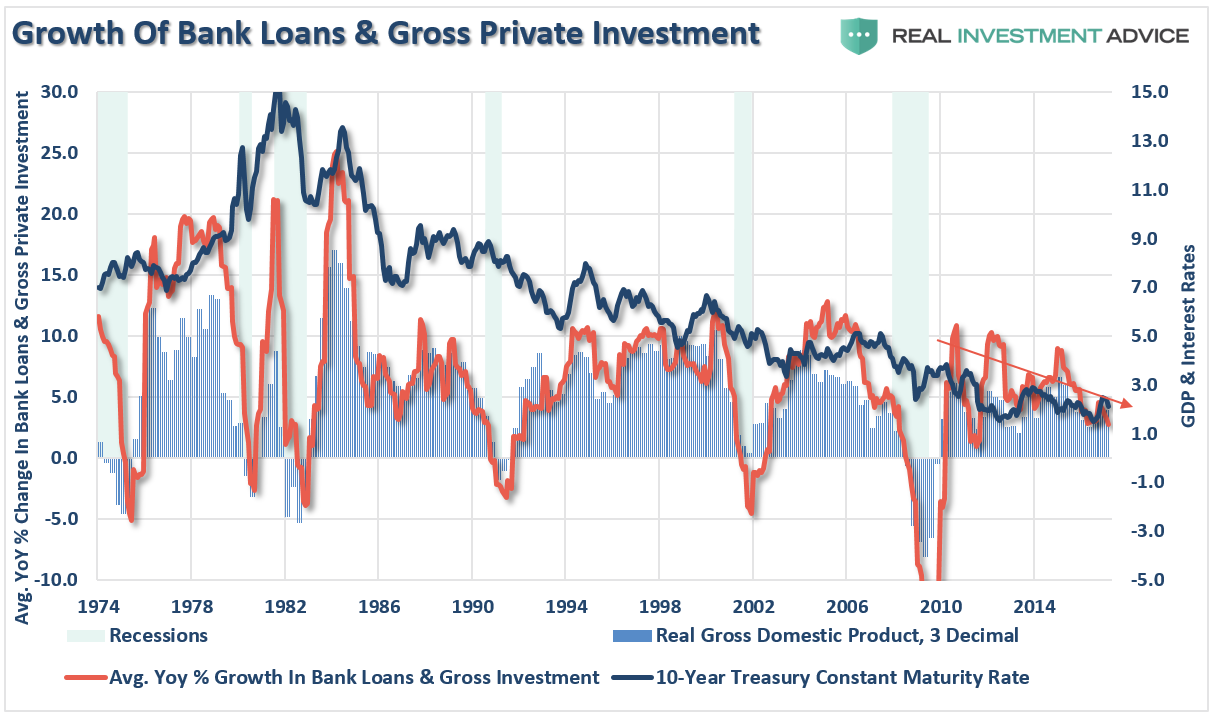

As you can see, the level of interest rates is directly tied to the strength of economic growth and inflation. Since wage growth is what allows individuals to consume, which makes up roughly 70% of economic growth, the level of demand for borrowing is directly tied to the demand from consumption. As demand increases, businesses then demand credit for increases in capital expenditures or production. The interest rates of loans are driven by demand from borrowers. Currently, as shown below, the level of demand is consistent with the interest rates currently being charged. (Also: note the sharp drop in activity over the last several months which has been previously consistent with recessionary onsets)

Since “borrowing costs” are directly tied to the underlying economic factors that drive the NEED for credit, interest rates, and therefore bond values, can not be overvalued. Furthermore, since bonds have a finite value at maturity, there is little ability for an overvaluation in the “price paid” for a bond as compared to its future “finite value” at maturity.

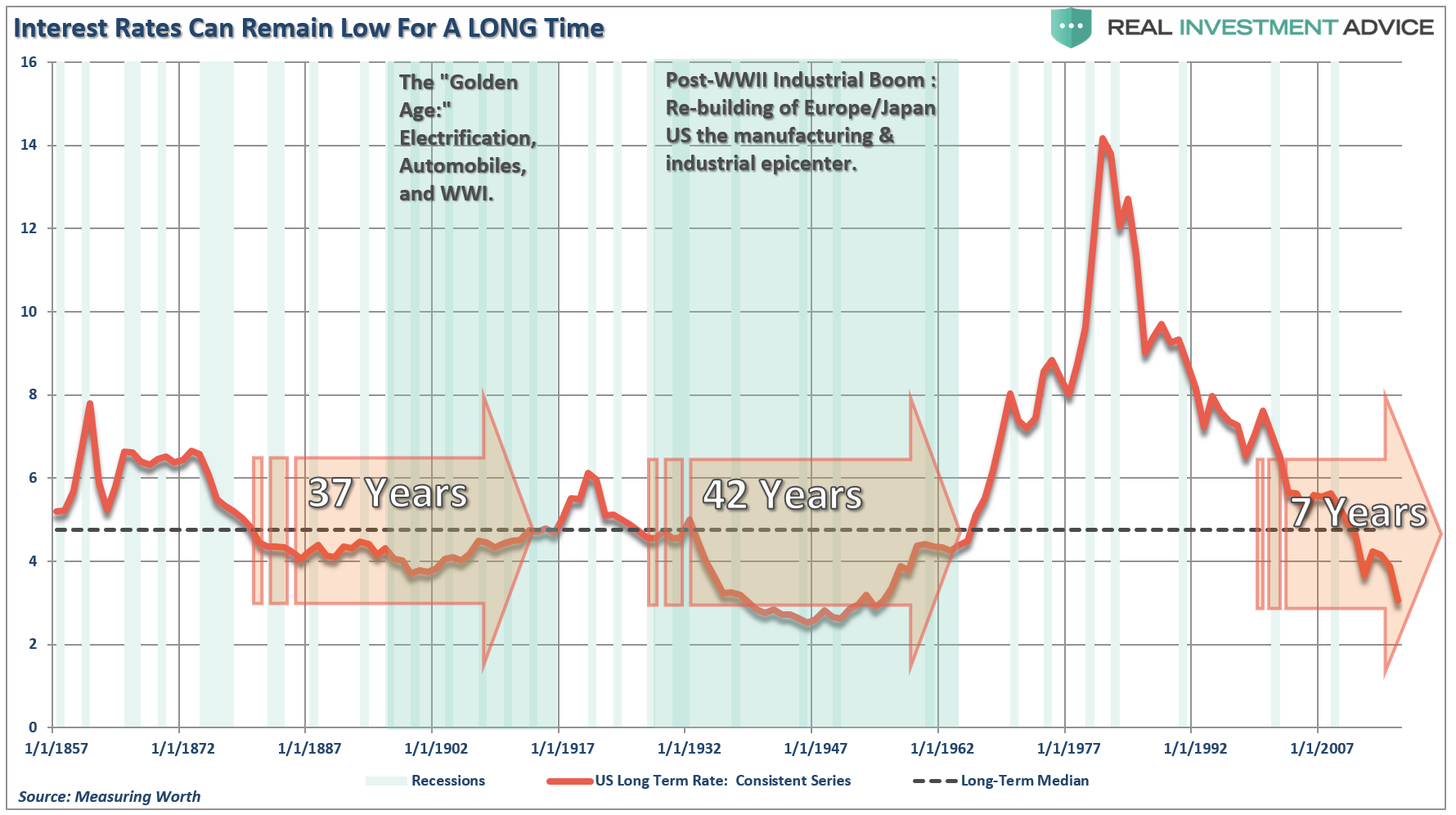

As I discussed previously, the primary argument that rates must go up, is simply because rates are currently so low. That is not necessarily true. Take a look at the long-term chart of 10-year equivalent Treasury rates below. (The dashed black line is the median interest rate during the entire period.)

(Note: Notice that a period of sustained low interest rates below the long-term median, as shown in the chart above, averaged roughly 40 years during both previous periods. We are only currently 7-years into the current secular period of sub-median interest rates.)

As shown, there have been two previous periods in history that have had the necessary ingredients to support rising interest rates. The first was at the turn of the previous century as the country became more accessible via railroads and automobiles, production ramped up for World War I and America began the shift from an agricultural to industrial economy.

The second period occurred post-World War II as America became the “last man standing” as France, England, Russia, Germany, Poland, Japan and others were left devastated. It was here that America found its strongest run of economic growth in history as the “boys of war” returned home to start rebuilding the countries that they had just destroyed. But that was just the start of it as innovations leaped forward as all eyes turned toward the moon.

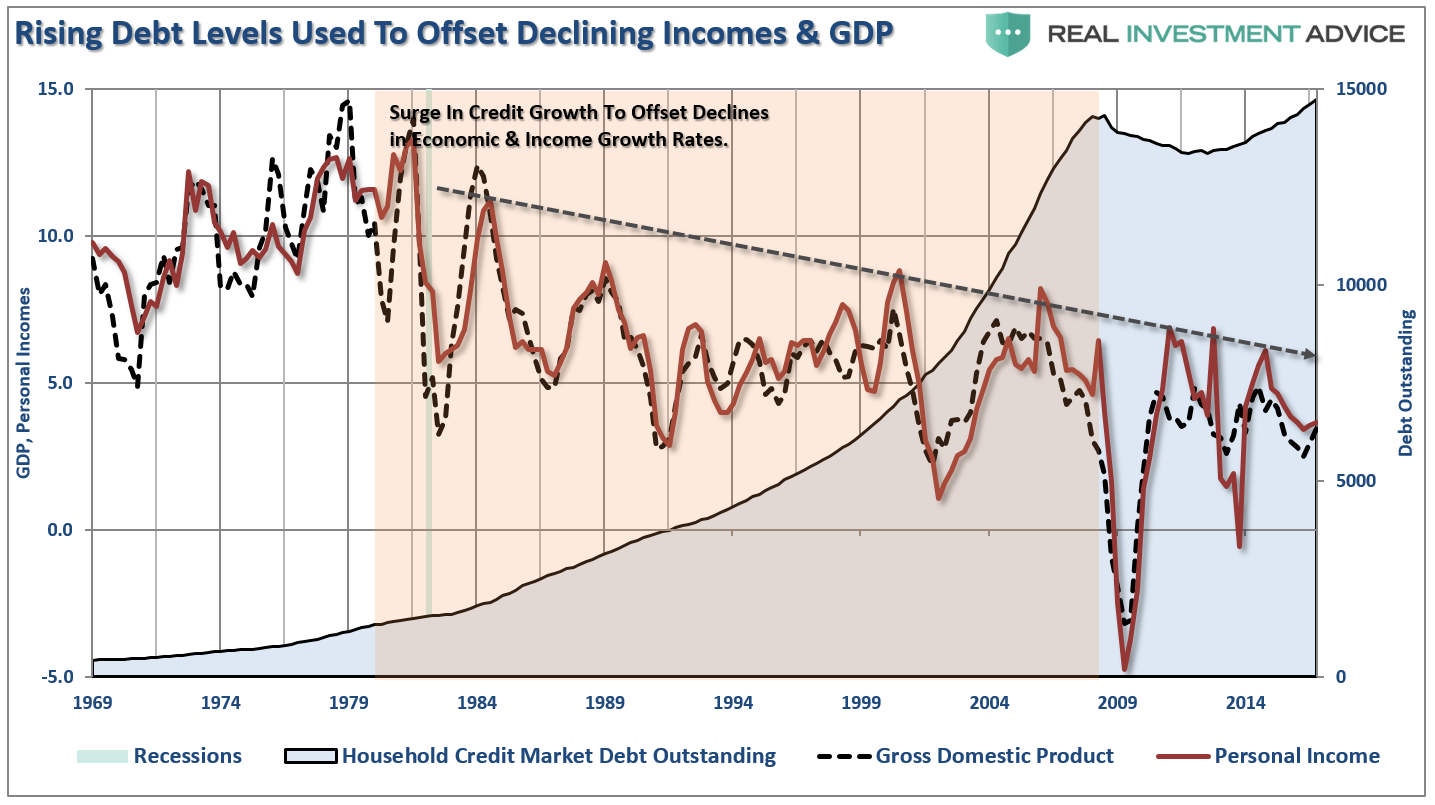

Today, the U.S. is no longer the manufacturing epicenter of the world. Labor and capital flows to the lowest cost providers so that inflation is effectively exported from the U.S. and deflation can be imported. Technology and productivity gains ultimately suppress labor and wage growth rates over time and debt continues to usurp capital from productive investments and savings. The chart below shows this dynamic change which begins in 1980. A surge in consumer debt was the offset between lower rates of economic growth and incomes in order to maintain the “American lifestyle.”

The problem with most of the forecasts for the end of the bond bubble is the assumption that we are only talking about the isolated case of a shifting of asset classes between stocks and bonds.

However, the issue of rising borrowing costs spreads through the entire financial ecosystem like a virus. The rise and fall of stock prices have very little to do with the average American and their participation in the domestic economy. Interest rates are an entirely different matter.

Since interest rates affect “payments,” increases in rates quickly have negative impacts on consumption, housing, and investment which ultimately deters economic growth.

Given the current demographic, debt, pension and valuation headwinds, the future rates of growth are going to be low over the next couple of decades. Even the Fed’s own “long run” economic growth rates currently run below 2%. Given this environment, the current level of interest rates are currently “fairly valued” based on those conclusions.

Will the “bond bull” market eventually come to an end? Yes, eventually. However, the catalysts needed to create the type of economic growth required to drive interest rates substantially higher, as we saw prior to 1980, are simply not available today. This will likely be the case for many years to come as the Fed, and the administration, come to the inevitable conclusion that we are now caught in a “liquidity trap” along with the bulk of developed countries.

While there is little left for interest rates to fall in the current environment, there is also not a tremendous amount of room for increases. Therefore, bond investors are going to have to adopt a “trading” strategy in portfolios as rates start to go flat-line over the next decade.

Of course, you don’t have to look much further than Japan for a clear example of what I mean.

Disclosure: The information contained in this article should not be construed as financial or investment advice on any subject matter. Streettalk Advisors, LLC expressly disclaims all liability in ...

more

A very good primer on the whole issue. Perhaps, an analysis of the yield curve would support your case more that there is no bubble as the flattening of the curve argues that inflation is not a problem.

I wonder if we could add Doug Cass to the tantrum brotherhood. That mafia scares people with bond prices all the time, in order to secure bonds for people who want to buy them at a discount. The only Cass I really liked anyway was Momma Cass.