What Is A Liquidity Trap?

Article of the Week from Fixing the Economists

by Philip Pilkington

Perhaps the worst thing that can happen to a term in any language is that it loses completely its meaning and becomes a sort of floating signifier that can attach itself to any old nonsense. Such is the case today with the term “liquidity trap”.

In contemporary parlance, “liquidity trap” means something like the situation many countries have faced since 2008; that is, a situation in which central banks have lowered interest rates right down to the zero-bound level and the economy fails to respond.

It is certainly clear why this might be considered a sort of “trap”, but why on earth would it be considered a “liquidity” trap? Few today seem to stop to think about the actual meaning of the two words in this term in any depth at all, so busy are they debasing the words in the English language as if they were so many clipped coins.

“Liquidity trap”. Well, that must be a trap caused by liquidity. Is it then a trap caused by too much liquidity? Surely not. That would imply that the central banks created our current so-called liquidity trap by creating too much money, but clearly modern day liquidity trap proponents like Paul Krugman do not think this. They think that the central bank has hit a limit to the amount of effectiveness money creation can have. The “trap” comes from elsewhere then.

So, from where does it come? Well, the modern day liquidity trap proponents seem to imply that in our current environment the demand for money becomes perfectly elastic – that is, no matter how much money the central banks create it is simply soaked up by thirsty hoarders. Hence the trap – not one caused by liquidity, but instead one in which people become desperate for liquidity.

In fact, this is precisely what the originator of the term, John Maynard Keynes, and his followers actually thought that a liquidity trap was. Here is the original quote on the liquidity trap from Keynes’ General Theory of Employment, Money and Interest:

There is the possibility … that, after the rate of interest has fallen to a certain level, liquidity-preference may become virtually absolute in the sense that almost everyone prefers cash to holding a debt which yields so low a rate of interest. In this event the monetary authority would have lost effective control over the rate of interest. But whilst this limiting case might become practically important in future, I know of no example of it hitherto.

Note carefully what Keynes is saying here. He is saying that in the event of a liquidity trap the rate of interest would fall outside the dictates of the central bank. The bank would pump money into the system and interest rates would fail to come down because people would simply hold cash. This is absolutely not happened in the post-2008 world, where yields across the board fell in response to the money creation programs like QE.

Keynes’ follower Hyman Minsky used the liquidity trap argument in the correct manner and gave it a sharper form; one which, unlike the form used by the pseudo-Keynesians, actually seeks to elucidate something rather than create a fog of unmeaning. Here is a quote from his book Stabilizing an Unstable Economy:

After a debt deflation that induces a deep depression, an increase in the money supply with a fixed head count of other assets may not lead to a rise in the price of other assets. (Stabilizing an Unstable Economy, p202)

So, what happens in such a scenario? Well, interest rates on assets that are not considered almost perfectly liquid rises sharply. Here is Minsky from his earlier bookJohn Maynard Keynes:

The view that the liquidity-preference function is a demand-for-money relation permits the introduction of the idea that in appropriate circumstances the demand for money may be infinitely elastic with respect to variations in the interest rate… The liquidity trap presumably dominates in the immediate aftermath of a great depression or financial crisis. (John Maynard Keynes, p36)

Read that carefully. The liquidity trap dominates then in the “immediate aftermath” of a financial crisis. What we would expect to see in an actual liquidity trap is prices falling on assets that are not considered perfectly safe and, conversely, interest rates rising on those same assets. Meanwhile, assets that are considered perfectly safe – like Treasury Bills – should see their prices rise and their interest rates fall.

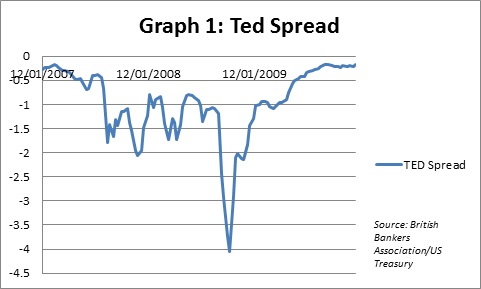

And that is precisely what we saw in the immediate aftermath of the 2008 crisis as can be seen from the TED Spread below which is the spread between the LIBOR rate, the rate at which banks typically lend to one another, and the three-month Treasury Bill rate, which is the value placed on perfectly safe assets.

There is your liquidity trap. But as we can also see from the graph, we exited the liquidity trap rather quickly – we were out by late 2009 – and as the quantitative easing programs were stepped up asset prices rose across the board and interest rates fell. The world we then entered was indeed a strange one. But to characterise it as a sort of perpetual liquidity trap, as the likes of Krugman and the pseudo-Keynesians do, is completely outlandish.

A liquidity trap does not exist unless the prices on imperfectly safe assets are falling and their interest rates are rising. This is not the world we have lived in since 2008 and so this world is not one of a liquidity trap. The only reason anyone thinks otherwise is because they are sloppy thinkers who, frankly, do not understand what they’re talking about or even the words they use to express themselves. They seem to want to create a rationalisation for why monetary policy – which they hold as the superior tool of economic management – fails. But the real reason it failed was because it was never a particularly good tool for macroeconomic stabilisation in the first place. It had nothing to do with some extended period of the economy remaining in a liquidity trap. And if the pseudo-Keynesians must come up with fancy sounding terms for monetary policy’s failure after the crisis, could they kindly make up these terms themselves and not spoil the ones we already have?

Disclosure: None.