There Will Be No Economic Boom

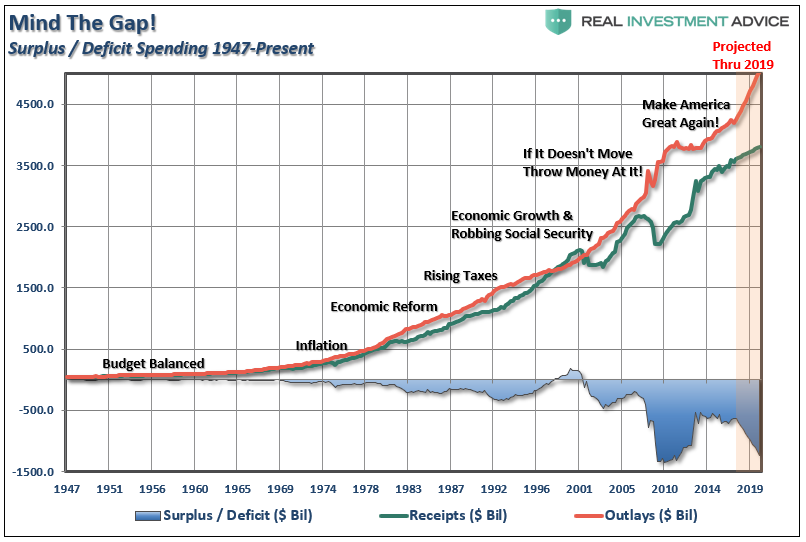

Last week, Congress passed a 2-year “continuing resolution, or C.R.,” to keep the Government funded through the 2018 elections. While “fiscal conservatism” was just placed on the sacrificial altar to satisfy the “Re-election” Gods,” the bigger issue is the impact to the economy and, ultimately, the financial markets.

The passage of the $400 billion C.R. has an impact that few people understand. When a C.R. is passed it keeps Government spending at the same previous baseline PLUS an 8% increase. The recent C.R. just added $200 billion per year to that baseline. This means over the next decade, the C.R. will add $2 Trillion in spending to the Federal budget. Then add to that any other spending approved such as the proposed $200 billion for an infrastructure spending bill, money for DACA/Immigration reform, or a whole host of other social welfare programs that will require additional funding.

But that is only half the problem. The recent passage of tax reform will trim roughly $2 Trillion from revenues over the next decade as well.

This is easy math.

Cut $2 billion in revenue, add $2 billion in spending, and you create a $4 Trillion dollar gap in the budget. Of course, that is $4 Trillion in addition to the current run rate in spending which continues the current acceleration of the “debt problem.”

But it gets worse.

As Oxford Economics reported via Zerohedge:

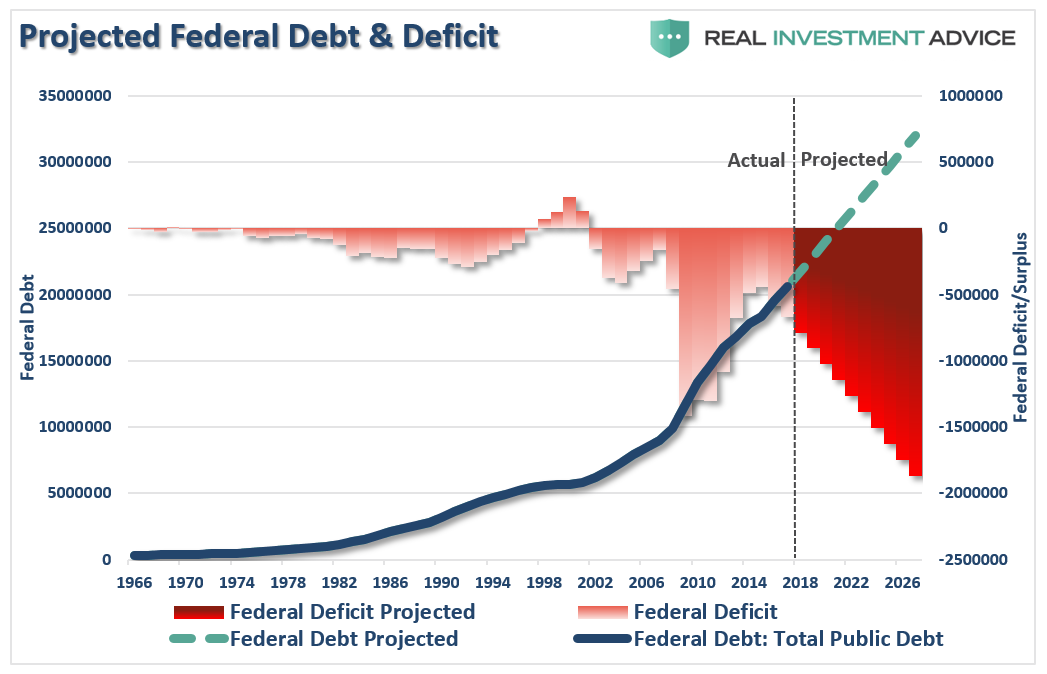

“The tax cuts passed late last year, combined with the spending bill Congress passed last week, will push deficits sharply higher. Furthermore, Trump’s own budget anticipates that US debt will hit $30 trillion by 2028: an increase of $10 trillion.”

Oxford is right. In order to “pay for” all of the proposed spending, at a time when the government will receive less revenue in the form of tax collections, the difference will be funded through debt issuance.

Simon Black recently penned an interesting note on this:

“Less than two weeks ago, the United States Department of Treasury very quietly released its own internal projections for the federal government’s budget deficits over the next several years. And the numbers are pretty gruesome.

In order to plug the gaps from its soaring deficits, the Treasury Department expects to borrow nearly $1 trillion this fiscal year. Then nearly $1.1 trillion next fiscal year. And up to $1.3 trillion the year after that.

This means that the national debt will exceed $25 trillion by September 30, 2020.”

You can project the run rate quite easily, and it isn’t pretty.

Of course, “fiscal responsibility” left Washington a long time ago, so, what’s another $10 Trillion at this point?

While this issue is not lost on a vast majority of Americans that “choose” to pay attention, it has been quickly dismissed by much of the mainstream media, and Congressman running for re-election, by suggesting tax reform will significantly boost economic growth over the next decade. The general statement has been:

“By passing much-needed tax reform, we will finally unleash the economic growth engine which will more than pay for these tax cuts in the future.”

Don’t dismiss the importance of $25-30 Trillion in U.S. debt. It is larger than the debts of every other nation in the world – combined.

Congress Killed The Economic Boom

While it truly is a great “talking point,” the reality is it just isn’t true.

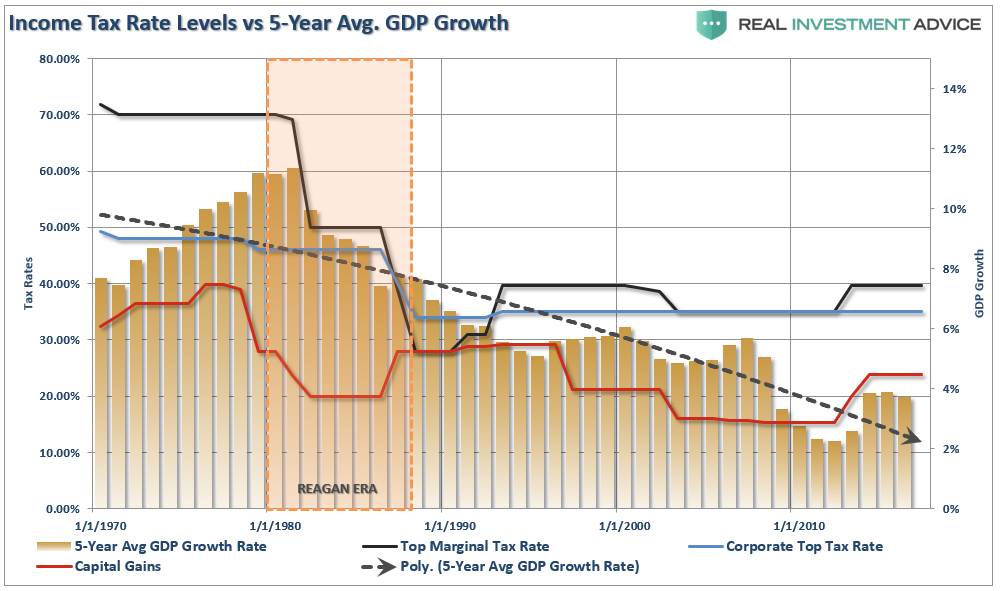

As I have shown previously, there is absolutely NO historical evidence that cutting taxes, without offsetting, cuts to spending leads to stronger economic growth.

Even Congressman Kevin Brady, Chairman of the House Ways and Means Committee, confirmed the same.

Deficits, and deficit spending, are HIGHLY destructive to economic growth as it directly impacts gross receipts and saved capital equally. Like cancer – running deficits, along with continued deficit spending, continues to destroy saved capital and damages capital formation.

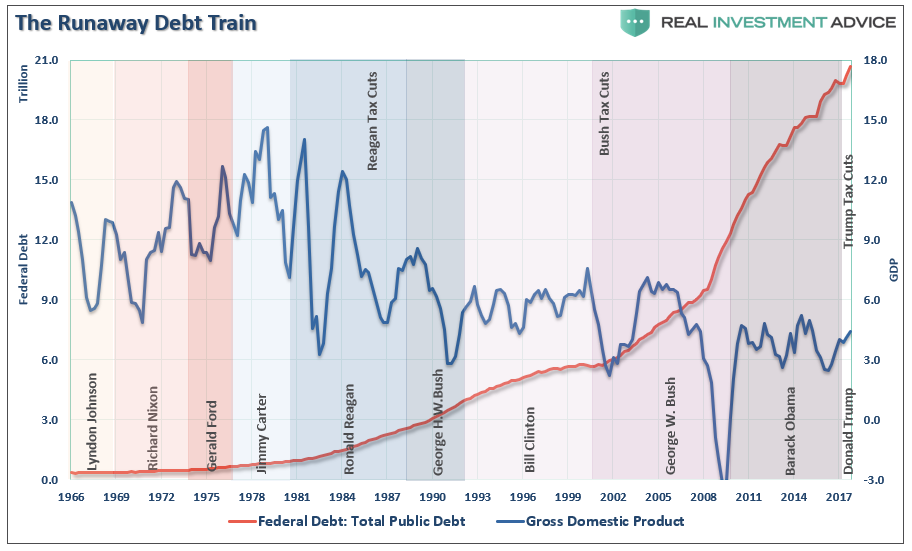

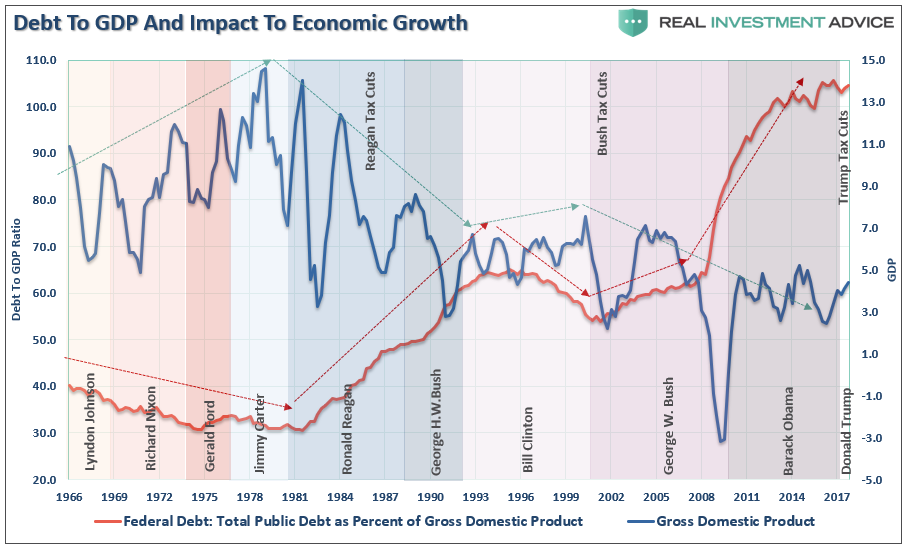

Debt is, by its very nature, a cancer on economic growth. As debt levels rise it consumes more capital by diverting it from productive investments into debt service. As debt levels spread through the system it consumes greater amounts of capital until it eventually kills the host. The chart below shows the rise of federal debt and its impact on economic growth.

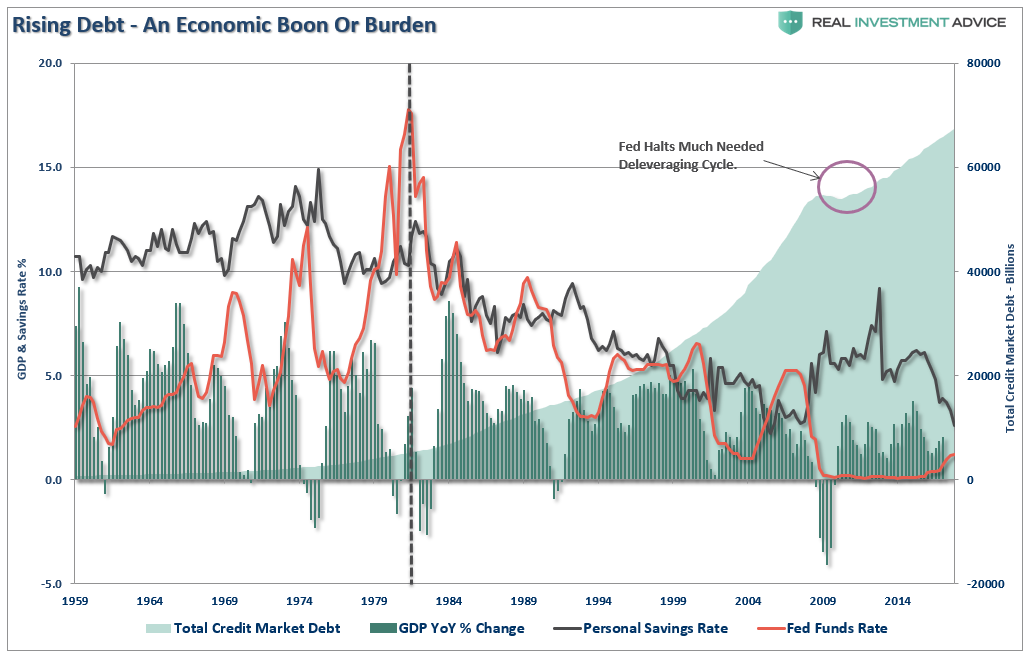

The reality is that the majority of the aggregate growth in the economy since 1980 has been financed by deficit spending, credit creation and a reduction in savings. This reduced productive investment in the economy and the output of the economy slowed. As the economy slowed, and wages fell, the consumer was forced to take on more leverage to maintain their standard of living which in turn decreased savings. As a result of the increased leverage more of their income was needed to service the debt – and with that, the “debt cancer” engulfed the system.

The Austrian business cycle theory attempts to explain business cycles through a set of ideas. The theory views business cycles:

“As the inevitable consequence of excessive growth in bank credit, exacerbated by inherently damaging and ineffective central bank policies, which cause interest rates to remain too low for too long, resulting in excessive credit creation, speculative economic bubbles and lowered savings.”

The problem that is yet not recognized by the current Administration and mainstream economists is that the excessive deficits and exponential credit creation can no longer be sustained. The process of a “credit contraction” will eventually occur over a long period of time as consumers and governments are ultimately forced to deal with the deficits.

The good news is the process of “clearing” the market will eventually allow resources to be reallocated back towards more efficient uses and the economy will begin to grow again at more sustainable and organic rates.

Today, however, expectations of a return to economic growth rates of the past are most likely just a fairy tale. The past 9-years of stock market returns have been fueled by trillions of dollars of support and direct injections into the financial system – that support is not sustainable in the long run. While the injections have kept the economy from falling into a depression in the short term – the unwinding of that support will suppress economic growth for many years to come.

There is no way to achieve the necessary goals “pain-free.” The time to implement austerity measures is when the economy is running a budget surplus and is close to full employment. That time was two Administrations ago when the economy would have slowed but could have absorbed and adjusted to the restrictive measures. However, when things are good, no one wants to “fix what isn’t broken”. The problem today is that with a high dependency on government support, high levels of underemployment and rising budget deficits, the implementation of austerity measures will only deter future economic growth, which is dependent on the very things that need to be “fixed”.

The processes that fueled the economic growth over the last 30 years are now beginning to run in reverse, and when combined with the demographic shifts in the U.S., the impact could be far more immediate and prolonged than the media, economists, and analysts are currently expecting. Sacrifices will have to be made, the economy will drag on at subpar rates of growth, individuals will be working far longer into their retirement years and the next generation of Americans will lead a far different life than what the currently retiring generation enjoyed.

It is simply a function of the math.

Disclosure: The information contained in this article should not be construed as financial or investment advice on any subject matter. Real Investment Advice is expressly disclaims all liability in ...

more