The Myths Of Stocks For The Long Run – Part X

<< Read More: Part I – “Buy & Hold” Can Be Hazardous To Your Wealth

<< Read More: Part II – Why Crashes Matter & The Saving Problem

<< Read More: Part III – Valuations & Forward Returns

<< Read More: Part IV – The Math Of Loss

<< Read More: Part V – Choosing The Right Portfolio Benchmark

<< Read More: Part VI – Should You Invest Like Warren Buffett?

<< Read More: Part VII - The Myths Of Stocks For The Long Run

<< Read More: Part VIII - The Myths Of Stocks For The Long Run

<< Read More: The Myths Of Stocks For The Long Run – Part IX

CHAPTER 10 – Risk Knows No Age

“If you are a young investor, you need to take on as much risk as possible. The more risk you take, the greater the reward.”

This is actually a false statement.

Let’s start with the definition of “risk” according to Merriam-Webster:

1: possibility of loss or injury : peril

2: someone or something that creates or suggests a hazard

3a : the chance of loss or the perils to the subject matter of an insurance contract; also : the degree of probability of such loss

3b : a person or thing that is a specified hazard to an insurer

3c : an insurance hazard from a specified cause or source

4: the chance that an investment (such as a stock or commodity) will lose value

Nowhere in that definition does it suggest a positive outcome for taking on “risk.”

In fact, the more “risk” assumed by an individual the greater the probability of a negative outcome. We can use a mathematical example of “Russian Roulette” to prove the point.

The number of bullets, the prize for “surviving,” and the odds of “survival” are shown:

(Click on image to enlarge)

While there are certainly those that would “eat a bullet” for their family, the point is simply while “more risk” equates to more reward, the consequences of a negative result increases markedly.

The same is true in investing.

At the peak of bull market cycles, there is a pervasive, cancerous dogma communicated by Wall Street and the media which suggests that in the long run, stocks are a “safe bet,” and risk is somehow mitigated over time.

This is simply not true.

Blaise Pascal, a brilliant 17th-century mathematician, famously argued that if God exists, belief would lead to infinite joy in heaven, while disbelief would lead to infinite damnation in hell. But, if God doesn’t exist, belief would have a finite cost, and disbelief would only have at best a finite benefit.

Pascal concluded, given that we can never prove whether or not God exists, it’s probably wiser to assume he exists because infinite damnation is much worse than a finite cost.

A recent comment from a reader further confirms what many investors to believe about risk and time.

“The risk of buying and holding an index is only in the short-term. The longer you hold an index the less risky it becomes.”

So according to our reader, the “risk” of losing capital diminishes as time progresses.

First, risk does not equal reward. “Risk” is a function of how much money you will lose when things don’t go as planned. The problem with being wrong, and facing the wrath of risk, is the loss of capital creates a negative effect to compounding that can never be recovered.

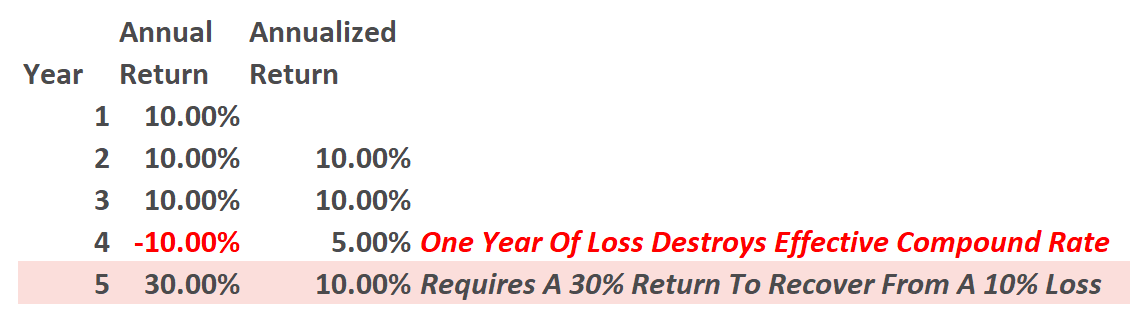

As we showed previously, let’s assume an investor wants to compound investments by 10% a year over a 5-year period. The table below shows what happens to the “average annualized rate of return” when a loss is experienced.

The “power of compounding” ONLY WORKS when you do not lose money. As shown, after three straight years of 10% returns, a drawdown of just 10% cuts the average annual compound growth rate by 50%. Furthermore, it then requires a 30% return to regain the average rate of return required. In reality, chasing returns is much less important to your long-term investment success than most believe.

The problem with following Wall Street’s advice to be “all in – all the time” is that eventually you are going to be dealt a losing hand such as in our example above. During bull market advances, prices rise in part due to earnings growth but also because investors are willing to pay more for a dollar of earnings than they were in the past. This is called multiple expansion and it is the hallmark of almost every bull market. Periods where price gains were largely the result of excessive multiple expansion, such as the 1920’s and 1990’s, were met with devastating losses when valuations normalized. The losses simply brought prices back to, or even below, levels which were commensurate with earnings.

The longer we chase a market where multiples are expanding well past norms, the greater the deviation from earnings and the greater the risk. As multiples expand, investors unwittingly escalate the inherent risk more than they realize which exposes them to greater damage when markets go through an eventual reversion process.

Even in healthy markets with fair valuations, risks exist. But in markets with high valuations the risk of a reversion increases as time marches on.

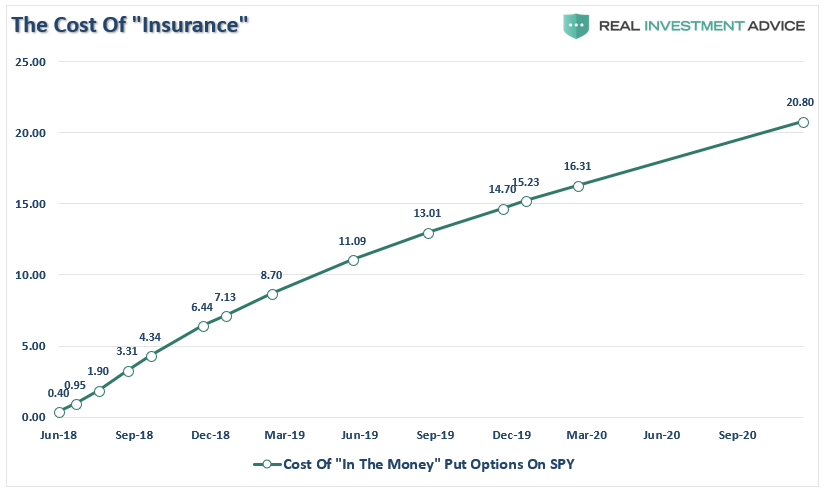

Here is another way to view how “risk” increases over time. Currently, valuations stand at levels similar to those of 1929 and not far behind those of 2000. Lets examine the current cost of “buying insurance” (put options) on the S&P 500 exchange-traded fund ($SPY). If the “risk” of ownership actually declines over time, then the cost of “insuring”the portfolio should decline as well. Why then, as shown below, does the cost of insurance rise over time?

(Click on image to enlarge)

As you can see, the longer the period our “insurance” covers, the more “costly” it becomes. This is because the risk of an unexpected event which creates a loss in value rises the longer an event doesn’t occur.

Furthermore, history shows that large drawdowns occur with regularity over time.

In early 2017, Byron Wien was asked the question of where we are in terms of the economy and the market to a group of high-end investors. To wit:

“The one issue that dominated the discussion at all four of the lunches was whether or not we were in the late stages of the business cycle as well as the bull market. This recovery began in June 2009 and the bull market began in March of that year. So we are more than 100 months into the period of equity appreciation and close to that in terms of economic expansion.“

His point is that markets rotate between bullish and bearish phases. When he made that statement he was simply saying the current economic recovery and the bull market are very long in the tooth. As shown below why shouldn’t we expect a market decline to follow, it has every other time?

(Click on image to enlarge)

The “full market cycle” will complete itself in due time to the detriment of those who fail to heed history, valuations, and psychology.

“There are two halves of every market cycle. “

(Click on image to enlarge)

“In the end, it does not matter IF you are ‘bullish’ or ‘bearish.’ The reality is that both ‘bulls’ and ‘bears’ are owned by the ‘broken clock’ syndrome during the full-market cycle. However, what is grossly important in achieving long-term investment success is not necessarily being ‘right’ during the first half of the cycle, but by not being ‘wrong’ during the second half.”

But as Mr. Pascal suggests, even if the odds that something will happen are small, we should still pay attention to that slim possibility if the potential consequences are dire. Rolling the investment dice while saving money by skimping on insurance may give us a shot at amassing more wealth, but the RISK of failure, and possibly a devastating failure, increase substantially.

Duration Matching

In the bond market the concept of “duration matching” is commonplace. If I have a specific target date, say 10-years in the future, I don’t want a portfolio of bonds maturing in 20-years. By matching the duration of the bond portfolio to my target date, I can immunize the portfolio against increases in interest rates which would negatively affect the principal value in the future.

Unfortunately, in the equity markets, and particularly given the advice of the vast majority of mainstream analysis suggesting that all individuals should “buy and hold” indexed based investments over the long-term, the concept of duration matching is disregarded.

Stocks are considered to be going concerns and therefore have no maturity, therefore the question of “duration matching” a stock portfolio becomes problematic. However, the problem can be somewhat solved through a combination of both allocation and risk management.

Over the years, I have done hundreds of seminars discussing how economic, fundamental and market dynamics drive future outcomes. At each one of these events, I always take a poll asking participants how long they have from today until retirement. Not surprisingly, the average is about 15 years.

The reason is obvious. For most in their 20’s and 30’s, they are simply not making enough money yet to save aggressively nor or is that a focus. During the 30’s and early 40’s, they are buying a house, raising kids, and paying for college – again, not a lot of money left over to save. For most, it is the mid-40’s and early 50’s where the realization to save and invest for retirement becomes a priority. Not surprisingly, this is the dynamic that we see across most of the country today in survey’s showing the majority of individuals VASTLY under-saved for retirement.

As you can see, the median American household will struggle to fund retirement..

There are two problems facing investor outcomes.

First, you don’t have 100+ years to invest in the market to get the “average” long-term returns.

Second, your “long-term” investment horizon is simply the time you have between today and when you retire. As I stated above, for most people that is about 15 years.

So, for argument sake, let’s be generous and assume you have 20-years from today until retirement. As we discussed previously, we know that based on current valuations in the market, forward real total returns in the market will likely be, on average, fairly low to negative.

(Click on image to enlarge)

What this chart clearly shows is the “WHEN” you invest is crucially more important than “IF” you invest in the financial markets. In regards to the current market environment consider this chart from Brett Freeze.

(Click on image to enlarge)

Based on 70 years of history, there has never been a period in which the ratio of market cap to GDP (red vertical dotted line) has been this high and returns over the next ten years were positive.

This is where the concept of “Duration Matching” in equity portfolios becomes important.

Given a 15 to 20-year time horizon for most individuals, investing when market valuations were elevated resulted in a loss of principal value during the time frame heading into retirement. In other words, most individuals simply “ran out of time” to reach their retirement goals. This has been the case currently for those 15-20 years ago that were planning to retire currently. Those plans have now been greatly postponed.

This is also the case for those with a 10-20 year horizon who put their trust into a “buy and hold” portfolio and disregard both valuations and risk.

When building a portfolio model, an investor must take into consideration the actual “time-frame” to retirement and the relative valuation level of the market at the beginning of the investing time frame.

For example, for an individual with a 15-year time frame to retirement and elevated market valuations, a portfolio model might resemble the following:

Note: The equity portion is “managed for downside risk protection” which we will explain in an upcoming chapter, which means that during certain periods the exposure to equities is reduced substantially.

The portfolio is designed to deliver a “total return” including capital appreciation to adjust the value of the individual’s “savings” for inflation, interest income and dividend yield. Each of these components is critical to achieving long-term investing success. While we can build a portfolio of bonds with a specific maturity, we have no such option in equities. This is where “risk management” must be used as a substitute.

Let’s compare the portfolio above with an all-equity portfolio in a market environment that is either +/- 10% in a given year.

Assume: Equity delivers a 2% dividend yield and taxable bonds deliver 3% in interest income.

The 50% recapture on the balanced portfolio means that we assume risk mitigation techniques will reduce losses by 50% relative to the decline of the S&P 500 index.

As you can see, managing a portfolio against downside can greatly increase future outcomes of the time frame an individual has until retirement. We regularly post a real-time model in the weekly newsletter since 2007 which adjusts a 60/40 allocation model for risk. By reducing the amount of time required to “get back to even” long-term returns can be improved to reach projected retirement goals.

(Click on image to enlarge)

Should you invest in the markets? Yes.

However, the allocation model used must adjust for both the time horizon to your financial goals and corresponding valuation levels.

If you are 20-years old and buy into the top of a market cycle, you could likely find yourself 20-years toward your retirement goal without much progress. Conversely, if you are 45-years, or older with valuations elevated, fundamental and economic prospects weak, and the majority of the previous bull-market behind you; managing your portfolio as if you were a 20-year old will have significantly negative outcomes.

As I stated above, the problem with equities is that they never mature. Unlike bonds where a specific rate of return can be calculated at the time of purchase, we can only guess at the future outcome of an equity-related investment. This is why some form of a “risk management” process must be adopted particularly in the latter years of the savings and accumulation time frame.

While it is always exhilarating to chase markets when they are rising, cheered on by the repetitious droning of the “buy and hold” crowd, when markets reverse those cheers turn to excuses. You are likely familiar with “no one could have seen the crash coming” and “you’re a long-term investor, right?”

The problem is that the “long-term” of the market and the “long-term” of your retirement goals are always two VERY different things.

There is only one true fact to remember:

“All bull markets last until they are over.” – Jim Dines

You see, risk has no age.

Risk is risk.

Disclosure: The information contained in this article should not be construed as financial or investment advice on any subject matter. Real Investment Advice is expressly disclaims all liability in ...

more