The Myths Of Stocks For The Long Run – Part VII

- Part I – “Buy & Hold” Can Be Hazardous To Your Wealth

- Part II – Why Crashes Matter & The Saving Problem

- Part III – Valuations & Forward Returns

- Part IV – The Math Of Loss

- Part V – Choosing The Right Portfolio Benchmark

- Part VI – Should You Invest Like Warren Buffett?

The Problem Of Psychology

During this series so far we have primarily discussed the more mechanical issues surrounding “investing myths” over the duration of an individuals investing “life-span.”

Individuals are often told:

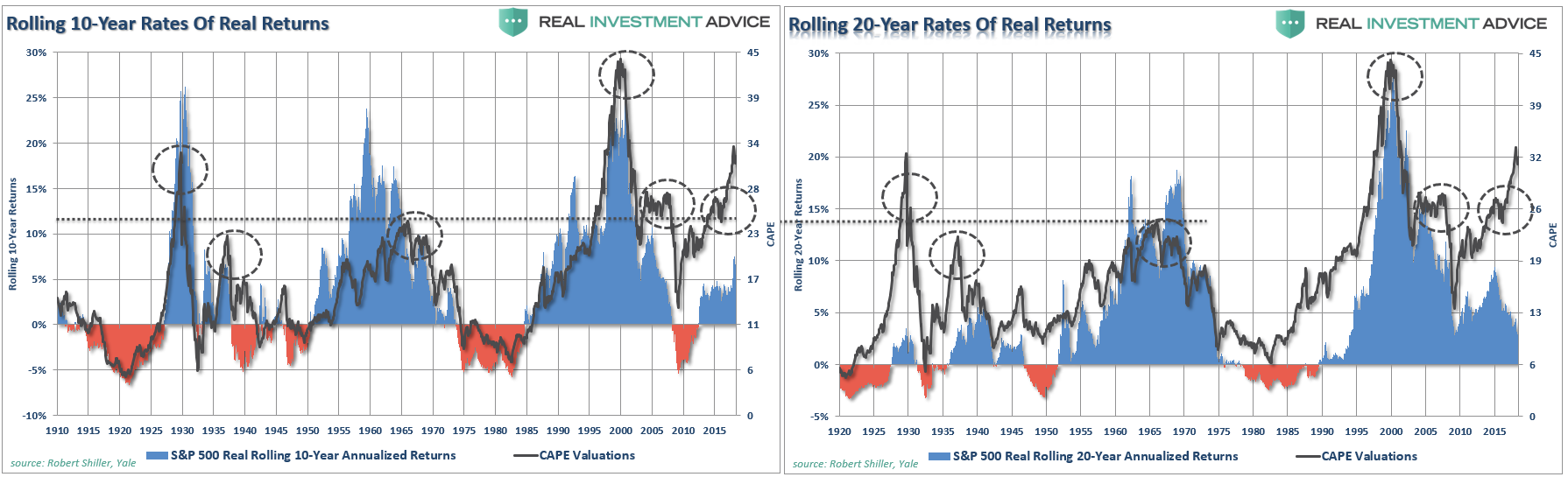

“There has never been a 10 or 20-year period in the market with negative returns.”

As we showed previously, such is not exactly correct once you account for inflation.

While “buying and holding” an index will indeed create a positive return over a long enough holding period, such does not equate to achieving financial success. But even if “investing your way to wealth” worked as advertised, then why are the vast majority of Americans so poorly equipped for retirement?

Every three years, the Federal Reserve conducts a study of American finances which exposes the lack of financial wealth for the bottom 90% of households. (Read: The Bottom 90% & The Failure Of Prosperity)

Other survey’s also confirm much of the same. Via Motley Fool:

“Imagine how the 50th percentile of those ages 35 – 44 has a household net worth of just $35,000 – and that figure includes everything they own, any equity in their homes, and their retirement savings to boot.

That’s sad considering those ages 35 and older have had probably been out in the workforce for at least ten years at this point.

And even the 50th percentile of those ages 65+ aren’t doing much better; they’ve got a median net worth of around $171,135, and quite possibly decades of retirement ahead of them.

How do you think that is going to work out?”

Another common misconception is that everyone MUST be saving in their 401k plans through automated contributions. According to Vanguard’s recent survey, not so much.

- The average account balance is $103,866 which is skewed by a small number of large accounts.

- The median account balance is $26,331

- From 2008 through 2017 the average inflation-adjusted gain was just 28%.

So, what happened?

- Why aren’t those 401k balances brimming over with wealth?

- Why aren’t those personal E*Trade and Schwab accounts bursting at the seams?

- Why are so many people over the age of 60 still working?

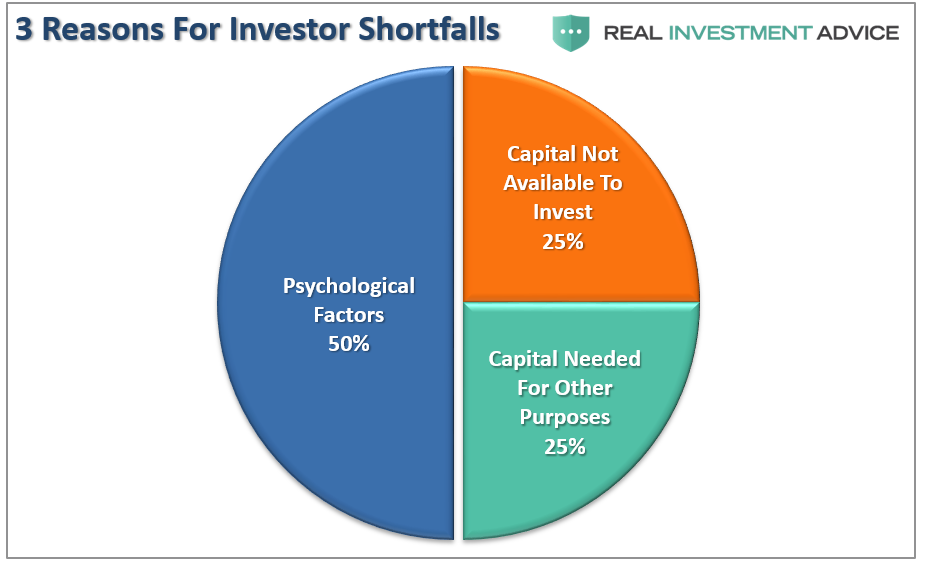

While we previously covered the impact of market cycles, the importance of limiting losses, the role of starting valuations, and the proper way to think about benchmarking your portfolio, the two biggest factors which lead to chronic investor underperformance over time are:

- Lack of capital to invest, and;

- Psychological behaviors

Psychological factors account for fully 50% of investor shortfalls in the investing process. It is also difficult to “invest” when the majority of Americans have an inability to “save.”

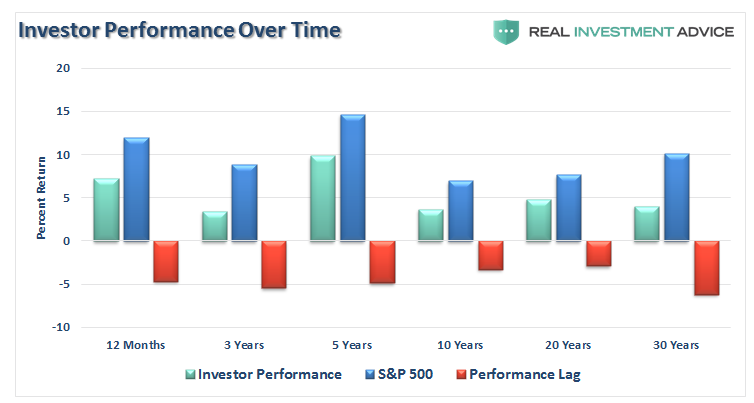

These factors, as shown by data from Dalbar, lead to the lag in performance between investors and the markets over all time periods.

While “buy and hold” and “dollar cost averaging” sound great in theory, the actual application is an entirely different matter. The lack of capital is an issue which can only be resolved through financial planning and budgeting, however, the simple answer is:

Live on less than you make and invest the rest.

Behavioral biases, however, are an issue which is little understood and accounted for when managing money. Dalbar defined (9) nine of the irrational investment behavioral biases specifically:

- Loss Aversion – The fear of loss leads to a withdrawal of capital at the worst possible time. Also known as “panic selling.”

- Narrow Framing – Making decisions about on part of the portfolio without considering the effects on the total.

- Anchoring – The process of remaining focused on what happened previously and not adapting to a changing market.

- Mental Accounting – Separating performance of investments mentally to justify success and failure.

- Lack of Diversification – Believing a portfolio is diversified when in fact it is a highly correlated pool of assets.

- Herding– Following what everyone else is doing. Leads to “buy high/sell low.”

- Regret – Not performing a necessary action due to the regret of a previous failure.

- Media Response – The media has a bias to optimism to sell products from advertisers and attract view/readership.

- Optimism – Overly optimistic assumptions tend to lead to rather dramatic reversions when met with reality.

George Dvorsky once wrote that:

“The human brain is capable of 1016 processes per second, which makes it far more powerful than any computer currently in existence. But that doesn’t mean our brains don’t have major limitations. The lowly calculator can do math thousands of times better than we can, and our memories are often less than useless — plus, we’re subject to cognitive biases, those annoying glitches in our thinking that cause us to make questionable decisions and reach erroneous conclusions.“

Cognitive biases are an anathema to portfolio management as it impairs our ability to remain emotionally disconnected from our money. As history all too clearly shows, investors always do the “opposite” of what they should when it comes to investing their own money. They “buy high” as the emotion of “greed” overtakes logic and “sell low” as “fear” impairs the decision-making process.

Let’s dig into the top-5 of the most insidious biases which keep us from achieving our long-term investment goals.

1) Confirmation Bias

As individuals, we tend to seek out information that conforms to our current beliefs. For instance if one believes that the stock market is going to rise, they tend to heavily rely on news and information from sources that support that position. Confirmation bias is a primary driver of the psychological investing cycle.

To confront this bias, investors must seek data and research that they may not agree with. Confirming your bias may be comforting, but challenging your bias with different points of view will potentially have two valuable outcomes.

First, it may get you to rethink some key aspects of your bias, which in turn may result in modification, or even a complete change, of your view. Or, it may actually increase the confidence level in your view.

The issue of “confirmation bias” is well known by the media. Since the media profits from “paid advertisers,” viewer or readership is paramount to obtaining those clients. The largest advertisers on many financial sites are primarily Wall Street related firms promoting products or services. These entities profit from selling product they create to individuals, therefore it should be no surprise they advertise on websites that tend to reflect supportive opinions. Given the massive advertising dollars that firms such as Fidelity, J.P. Morgan (JPM), and Goldman Sachs (GS) spend, it leaves little doubt why the more successful websites refrain from presenting views which deter investors from buying related products or services.

As individuals, we want “affirmation” our current thought processes are correct. As human beings, we hate being told we are wrong, so we tend to seek out sources that tell us we are “right.”

This is why it is always important to consider both sides of every debate equally, analyze the data accordingly, and form a balanced conclusion. Being right and making money are not mutually exclusive.

2) Gambler’s Fallacy

The “Gambler’s Fallacy” is one of the biggest issues faced by individuals when investing. As emotionally driven human beings, we tend to put a tremendous amount of weight on previous events believing that future outcomes will somehow be the same.

The bias is clearly addressed at the bottom of every piece of financial literature.

“Past performance is no guarantee of future results.”

However, despite that statement being plastered everywhere in the financial universe, individuals consistently dismiss the warning and focus on past returns expecting similar results in the future.

Performance chasing has a high propensity to fail continually causing investors to jump from one late cycle strategy to the next. This is shown in the periodic table of returns below. “Hot hands” only tend to last on average 2-3 years before going “cold.”

We traced out the returns of the S&P 500 and the Barclay’s Aggregate Bond Index for illustrative purposes. Importantly, you should notice that whatever is at the top of the list in some years tends to fall to the bottom of the list in subsequent years. “Performance chasing” is a major detraction from an investor’s long-term investment returns.

Of course, it also suggests that analyzing last year’s losers, which would make you a contrarian, has often yielded higher returns in the near future.

3) Probability Neglect

When it comes to “risk taking” there are two ways to assess the potential outcome. There are “possibilities” and “probabilities.” As individuals, we tend to lean toward what is possible such as playing the “lottery.” The statistical probabilities of winning the lottery are astronomical, in fact, you are more likely to die on the way to purchase the ticket than actually winning it. However, it is this infinitesimal “possibility” of being fabulously wealthy that makes the lottery so successful. Las Vegas exists for one reason; amateur gamblers favor possibility over probability.

As investors, we tend to neglect the “probabilities,” or specifically the statistical measure of “risk” undertaken, with any given investment. Our bias is to “chase” stocks that have already shown the biggest increase in price as it is “possible” they could move even higher. However, the “probability” is by the time the masses have come to discover the opportunity, most of the gains have likely already been garnered.

“Probability Neglect” is the very essence of the “buy high, sell low” syndrome.

Robert Rubin, former Secretary of the Treasury, once stated;

“As I think back over the years, I have been guided by four principles for decision making. First, the only certainty is that there is no certainty. Second, every decision, as a consequence, is a matter of weighing probabilities. Third, despite uncertainty, we must decide and we must act. And lastly, we need to judge decisions not only on the results, but on how they were made.

Most people are in denial about uncertainty. They assume they’re lucky, and that the unpredictable can be reliably forecasted. This keeps business brisk for palm readers, psychics, and stockbrokers, but it’s a terrible way to deal with uncertainty. If there are no absolutes, then all decisions become matters of judging the probability of different outcomes, and the costs and benefits of each. Then, on that basis, you can make a good decision.”

4) Herd Bias

Maybe the best way to show how susceptible we are to follow the crowd is by watching this video from Candid Camera.

Though we are often unconscious of the action, humans tend to “go with the crowd.” Much of this behavior relates back to “confirmation” of our decisions but also the need for acceptance. The thought process is rooted in the belief that if “everyone else” is doing something, and if I want to be accepted, then I need to do it also.

In life, “conforming” to the norm is socially accepted and in many ways expected. However, in the financial markets, the “herding” behavior is what drives markets to extremes.

As Howard Marks once stated:

“Resisting – and thereby achieving success as a contrarian – isn’t easy. Things combine to make it difficult; including natural herd tendencies and the pain imposed by being out of step, since momentum invariably makes pro-cyclical actions look correct for a while. (That’s why it’s essential to remember that ‘being too far ahead of your time is indistinguishable from being wrong.’

Given the uncertain nature of the future, and thus the difficulty of being confident your position is the right one – especially as price moves against you – it’s challenging to be a lonely contrarian.”

Moving against the “herd” is where the most profits are generated by investors in the long term. The difficulty for most individuals, unfortunately, is not necessarily knowing when to “bet” against the stampede but the psychologically debilitating action of being different. As they say, “it is lonely at the top.”

5) Anchoring Effect

This is also known as a “relativity trap” which is the tendency to compare our current situation within the scope of our own limited experiences. For example, I would be willing to bet that you could tell me exactly what you paid for your first home and what you eventually sold it for. However, can you tell me what exactly what you paid for your first bar of soap, your first hamburger, or your first pair of shoes? Probably not.

The reason is that the purchase of the home was a major “life” event. Therefore, we attach particular significance to that event and remember it vividly. If there was a gain between the purchase and sale price of the home, it was a positive event and, therefore, we are likely to assume that the next home purchase will have a similar result. When we become mentally “anchored” to an event we tend to base our future decisions around it.

When it comes to investing we do very much the same thing. If we buy a stock and it goes up, we remember that stock and that outcome. Therefore, we become anchored to that stock. Individuals tend to “shun” stocks which lost value even though the individual simply bought and sold at the wrong times. After all, it is not “our” fault an investment lost money; it was just a bad company. Right?

This “anchoring” effect also contributes to performance chasing over time. If you made money with ABC stock but lost money on DEF, then you “anchor” on ABC and keep buying it as it rises. When the stock begins its inevitable “reversion,” investors remain “anchored” on past performance until the “pain of ownership” exceeds their emotional threshold. It is then they tend to panic “sell” and now become “anchored” to a negative experience and never buy shares of ABC again. Worse, DEF, despite your past experience owning it, may present great value at reduced prices, but your previous negative experience reduces your inclination to purchase it.

Conclusion

In the end, we are just human. Despite the best of our intentions, it is nearly impossible for an individual to be devoid of the emotional biases that inevitably lead to poor investment decision making over time. This is why all great investors have strict investment disciplines that they follow to reduce the impact of human emotions.

Take a step back from the media, and Wall Street commentary, for a moment and make an honest assessment of the financial markets today. Are valuations at levels that have previously lead to higher rates of future returns? Are interest rates rising or falling? Are individuals currently assessing the “possibilities” or the “probabilities” in the markets?

As individuals, we invest our hard earned “savings” into a “speculative” environment where we are “betting” on a future outcome. The reality is the majority of individuals are ill-prepared for an impact event to occur. This is particularly the case in late-stage bull market cycles where complacency runs high.

The discussion of why “this time is not like the last time” is largely irrelevant. Whatever gains investors garner in the first-half of an investment cycle by chasing the “bullish thesis” will be almost entirely wiped out during the second-half. Of course, this is the sad history of individual investors in the financial markets as they are always “told to buy,” but never “when to sell.”

Disclosure: The information contained in this article should not be construed as financial or investment advice on any subject matter. Real Investment Advice is expressly disclaims all liability in ...

more