The Myths Of Stocks For The Long Run – Part V

Written by Lance Roberts, Michael Lebowitz, CFA and John Coumarianos, M.S.

- Part I – “Buy & Hold” Can Be Hazardous To Your Wealth

- Part II – Why Crashes Matter & The Saving Problem

- Part III – Valuations & Forward Returns

- Part IV – The Math Of Loss

Choosing The Right Portfolio Benchmark

“Investing isn’t about beating others at their game. It’s about controlling yourself at your own game.” –Ben Graham

Benchmarks serve an important role in growing one’s wealth. Most importantly they provide a yard-stick to see how we are doing in meeting our future retirement goals. For those that rely on professionals to manage their money, a benchmark allows the client to gauge how the manager is performing versus what the market is providing.

We do not disparage the use of benchmarks. However, the purpose of this article is to help you understand the differences between an equity index and your portfolio. As we discussed in Part 2 of this series, the proper benchmark for any portfolio is the rate of inflation plus a rate of growth that achieves the specific level of inflation-adjusted dollars required at retirement. Meeting such benchmark guarantees you meet your goal. No other index can claim that. Benchmarking to the S&P 500, or any other equity index, requires investors to take on excess investment risk which is not correlated to the financial goals or duration of the portfolio.

This article specifically addresses the difficulty of trying to track an equity benchmark index (i.e. the S&P 500.)

The continual efforts to “beat the benchmark” leads individuals to make emotional decisions to buy and sell at the wrong times; jump from one investment strategy to another, or from one advisor to the next. But why wouldn’t they? This mantra has been drilled into us by Wall Street over the last 30 years. While the chase to “beat the index” is great for Wall Street, as money in motion creates fees, most individuals have done far worse.

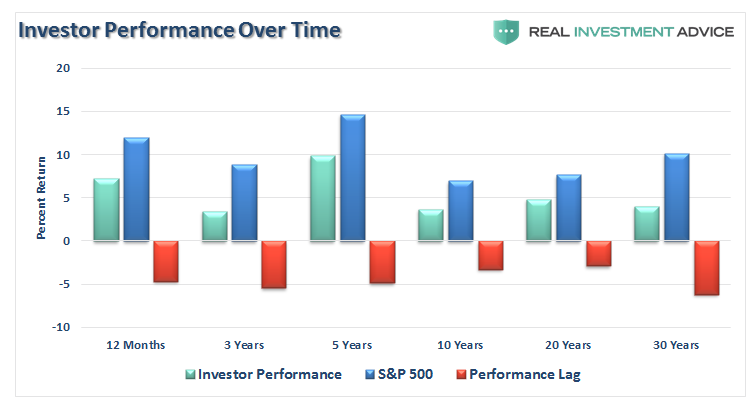

The annual studies from Dalbar show the dismal truth, individuals consistently underperform the benchmark index over EVERY time frame.

The reason this underperformance consistently occurs is due to emotional and behavioral tendencies and the many differences between a “market capitalization weighted index” versus a “dollar invested portfolio.”

Let’s set aside the emotional and behavioral mistakes for today, and focus on the differences between a benchmark index and your portfolio which make beating an index difficult.

Building The Sample Index

To best understand why tracking the S&P 500 index is hard we must first understand how the S&P 500 index is constructed. The following explanation is from Investopedia:

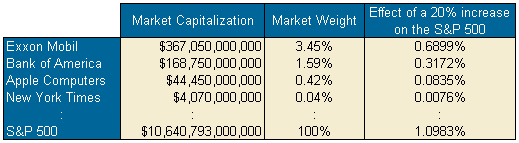

“The S&P 500 is a U.S. market index that is computed by a weighted average market capitalization. The first step in this methodology is to compute the market capitalization of each component in the index.

This is done by taking the number of outstanding shares of each company and multiplying that number by the company’s current share price, or market value. For example, if Apple Computer has roughly 830 million shares outstanding and its current market price is $53.55, the market capitalization for the company is $44.45 billion (830 million x $53.55).

Next, the market capitalizations for all 500 component stocks are summed to obtain the total market capitalization of the S&P 500, as illustrated in the table below. This market capitalization number will fluctuate as the underlying share prices and outstanding share numbers change.

In order to understand how the underlying stocks affect the index, the market weight (index weight) needs to be calculated. This is done by dividing the market capitalization of a company on the index by the total market capitalization of the index.

For example, if Exxon Mobil’s market cap is $367.05 billion and the S&P 500 market cap is $10.64 trillion, this gives Exxon a market weight of roughly 3.45% ($367.05 billion / $10.64 trillion). The larger the market weight of a company, the more impact each 1% change will have on the index.

For example, if Exxon Mobil were to rise by 20% while all other companies remained unchanged, the S&P 500 would increase in value by 0.6899% (3.45% x 20%). If a similar situation were to happen to The New York Times, it would cause a much smaller, 0.0076% change to the index because of the company’s smaller market weight.”

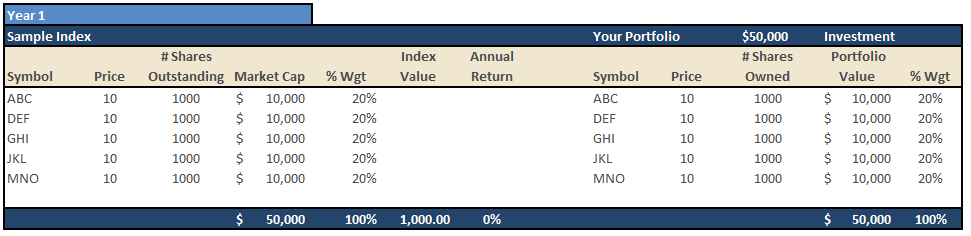

Okay, with that baseline understanding of the construction of the S&P 500, let’s create a most basic index called the Sample Index which is comprised of 5 fictional companies. For simplicity purposes, each company has 1000 shares of stock outstanding and all trade at $10 per share. The table shows the index versus “Your Portfolio” which is a $50,000 investment weighted identically.

We will take both the Sample Index and Your Portfolio through various events and price changes that cause differences to occur between the two. The events, and passage of time, are labeled at the top of each table. At the end of the exercise, we provide you a performance chart covering the entire period.

In Year 1, our starting point, we divide “your portfolio’s” $50,000 investment into exactly the same weights and stocks as the Sample Index as follows:

There are a couple of caveats here. The first is that by using so few stocks the percentage changes to the index, and subsequently the portfolio, are amplified versus that of the must broader indexes. However, this only for informational and learning purposes – it is the concept we are after.

Secondly, there are many other factors, outside of the examples that we will cover today, that have major impacts on performance. Corporate events such as mergers, buyouts, and acquisitions affect the index. Your portfolio is also impacted by withdrawals, contributions, and your dividend reinvestment policy.

Lastly, and most importantly, none of the examples today include the significant impacts to portfolio performance over time which comes from taxes, fees, commissions and other expenses. These factors alone typically account for a bulk of the underperformance over the long term but are often ignored by investors trying to chase some random benchmark index.

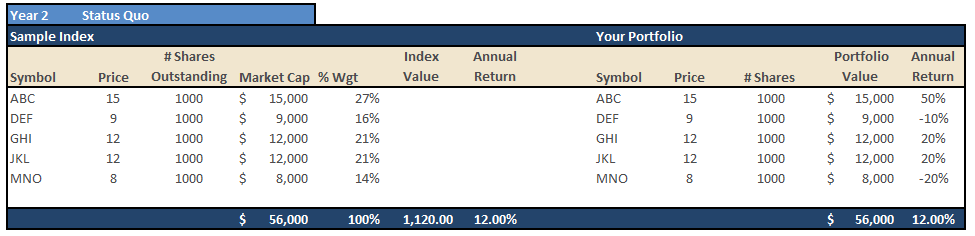

The Status Quo

In year two, we assume that nothing exceptional, other than typical price appreciation or depreciation occurred. The table below shows the impact of price changes on both the Sample Index and Your Portfolio.

As you can see the Sample Index and Your Portfolio had the same price return and remain exactly the same.

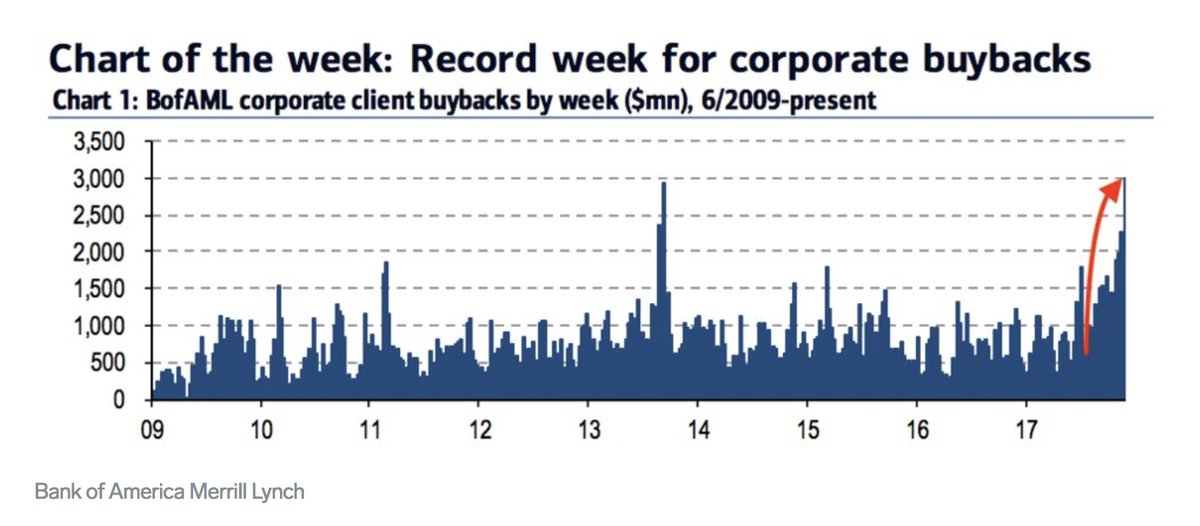

Share Buybacks & Bankruptcy

Over the last ten years, corporations have become major buyers of their own stock pushing such actions to record levels. Stock buybacks are typically viewed as a good thing by Wall Street analysts supposedly because it is a sign that the “company believes” in itself, however, nothing could be further from the truth.

The reality is that stock buybacks are often a tool used to artificially inflate bottom line earnings per share which, temporarily, drives share prices higher. The biggest beneficiary of buybacks are the executives whose compensation is heavily tied to stock options. The losers are the long terms shareholders. Not only must the debt and interest expense, frequently incurred to conduct buybacks, be paid for with future earnings, but the buyback, in many cases, took precedence over investment in the company’s future. The long-term implications for the company and the economy are troubling.

The importance of buybacks cannot be overlooked. The dollar amount of sales, or top-line revenue, is extremely difficult to fudge or manipulate. However, bottom line earnings are regularly manipulated by accounting gimmickry, cost-cutting, and share buybacks to enhance “per share” results in order to boost share prices and meet “Wall Street Expectations.”

Stock buybacks DO NOT show faith in the company by the executives but rather a LACK of better ideas for which to use the capital for.

Importantly, for our overall example, the reduction in outstanding shares reduces market capitalization.

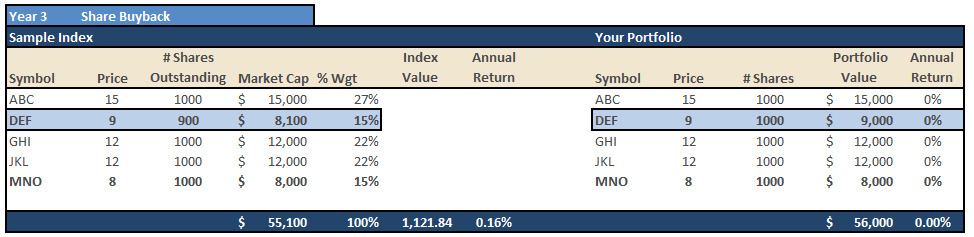

Let’s go back to our original index and portfolio example.

In year 3, Company DEF buys back 100 shares and each company experiences a change in its share price.

The table below shows the impact of these three events on the index and the portfolio.

Notice that the DEF share buyback caused the market capitalization of the index to fall and the weighting of DEF to decline versus the other stocks. Your Portfolio was unchanged and accordingly, the weightings of the index and your portfolio are different. As we will see the returns will begin to diverge at this point because of the slight change in weighting.

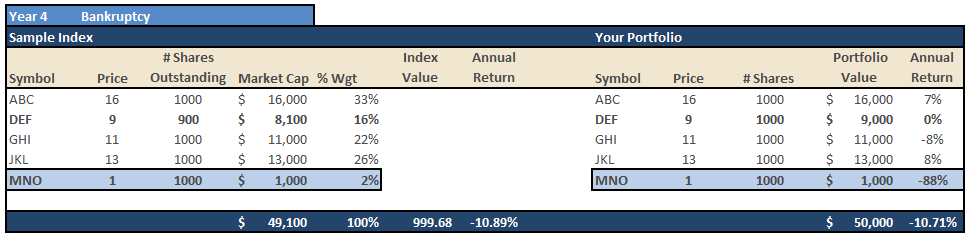

Substitution Effect

In year four we introduce the “substitution effect.”

When company’s such as GM, AIG, Enron, Worldcom, and a host of others in history, goes bankrupt or have shrunken considerably, they are swapped out of the index for another company. The index is naturally reweighted for the “substitution.” The table below shows the impact of the substitution on the index and your portfolio.

The substitution not only adds a new stock to the index but a stock with a much higher weighting than the one removed. Not only does Your Portfolio not hold the new stock but whatever value is left on the removed stock is still affecting your portfolio. Additionally, the change in weightings causes further misalignment between the index and your portfolio.

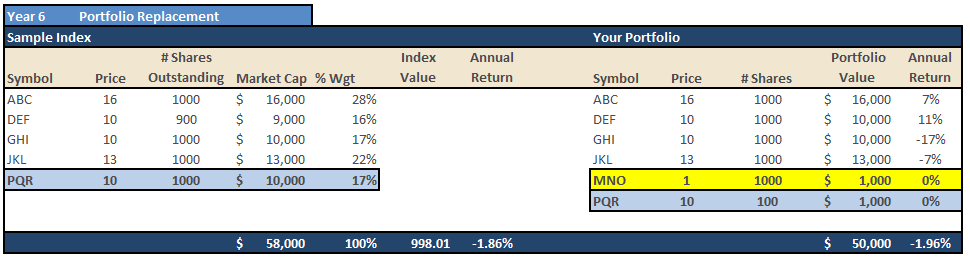

In order for you to get your portfolio back into alignment with the Sample Index, the stock of MNO Company must be sold and replaced with PQR. The problems with doing this are shown in the next table.

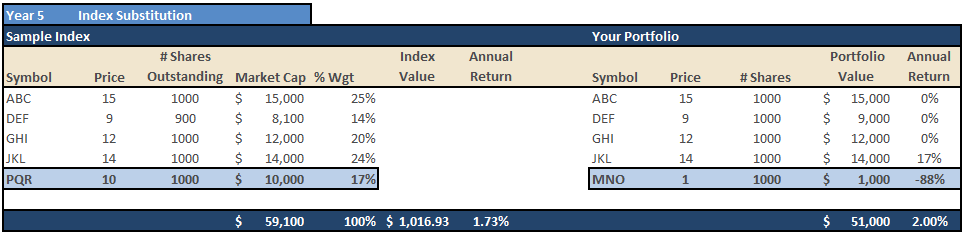

The Replacement Effect

The replacement of a stock in your actual portfolio is confronted by a problem. Since there is no cash in the portfolio, other than what was raised by the sell of MNO – only 100 shares of PQR can be purchased as shown in the table below.

As with each year previously we also included changes in price for each individual company other than PQR so that the substitution and replacement were done at the same price for example purposes.

Note: Yes, I could have rebalanced the portfolio to raise cash to purchase more shares of PQR, however, we have NOT rebalanced the index. Therefore, using just available cash is the appropriate measure.

Comparison Is The Problem

The point of this exercise is to show how different types of index and corporate events change the composition of the Index. Unless one is consistently rebalancing their portfolio they will not be able to match the index. Even if one is constantly trading to mimic the index, the commissions, taxes, and fees will weigh heavily on results over time and will lead to underperformance of the benchmark index.

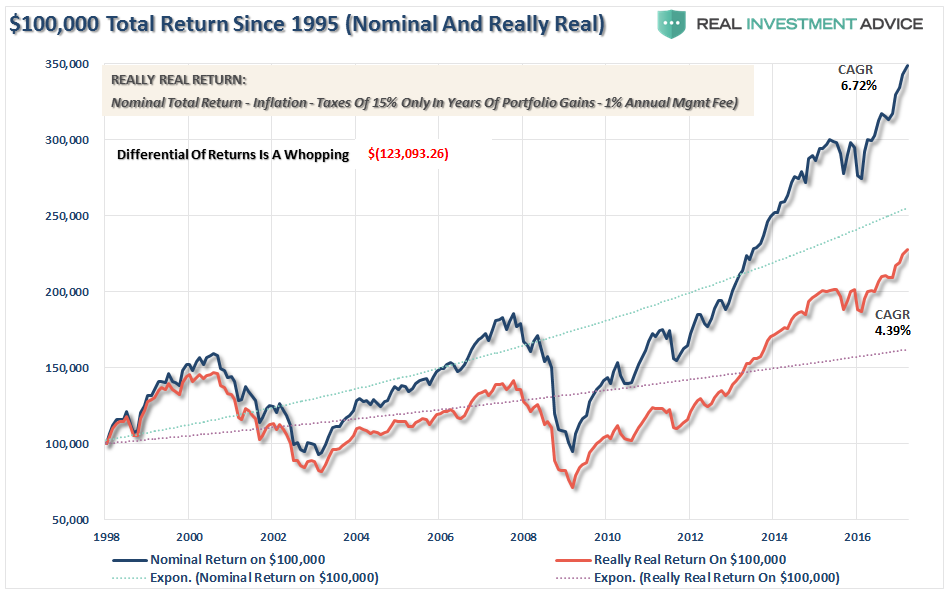

The chart below once again returns us to our $100,000 invested into the nominal index versus a $100,000 portfolio adjusted for “reality.” A $100,000 investment in 1998 has had a compounded annual growth rate of 6.72% on a nominal basis as compared to just a 4.39% rate when adjusted for reality. The numbers are far worse if you started in 2000 or 2008.

Furthermore, both numbers also fall far short of the promised 8% annualized rates of return often promised by the mainstream analysts promising riches if you just buy their investment product, or service, and hang on long enough.

The reality, as shown previously, is that such an outcome will likely prove to be extremely disappointing. However, the financial media continually pushes the idea that we must “beat the index.”

However, comparison is the cause of more unhappiness than anything else. Perhaps it is inevitable that human beings as social animals have an urge to compare themselves with one another. Maybe it is just because we are all terminally insecure in some cosmic sense. Social comparison comes in many different guises. “Keeping up with the Joneses,” is one well-known way.

Comparison is why individuals have trouble patiently sitting on their hands, letting whatever process they are comfortable with work for them. They get waylaid by some comparison along the way and lose their focus. If an individual makes 12% on their investments, they are very pleased. That is, until they learn “everyone else” made 14%. Now they are upset.

The whole financial services industry, as it is constructed now, is predicated on making people upset so they will move their money around in a frenzy. Money in motion creates fees and commissions. The creation of more benchmarks, indices and style boxes is nothing more than the creation of more things to COMPARE to which keeps individuals in a perpetual state of outrage creating more revenue for Wall Street.

Comparison of your performance to an index is potentially dangerous to your investing objectives.

The major learning points regarding benchmarking are:

1) The index contains no cash

2) It has no life expectancy requirements – but you do.

3) It does not have to compensate for distributions to meet living requirements – but you do.

4) It requires you to take on excess risk (potential for loss) in order to obtain equivalent performance – this is fine on the way up, but not on the way down.

5) It has no taxes, costs or other expenses associated with it – but you do.

6) It has the ability to substitute at no penalty – but you don’t.

7) It benefits from share buybacks – but you don’t.

In order to win the long-term investing game, your portfolio should be built around the things that matter most to you.

– Capital preservation

– A rate of return sufficient to keep pace with the rate of inflation.

– Expectations based on realistic objectives. (The market does not compound at 8%, 6% or 4%)

– Higher rates of return require an exponential increase in the underlying risk profile. This tends to not work out well.

– You can replace lost capital – but you can’t replace lost time. Time is a precious commodity that cannot be regained.

– Portfolios are time-frame specific. If you have a 5-years to retirement but build a portfolio with a 20-year time horizon (taking on additional risk) the results will likely be disastrous.

We want to reiterate an important thought from the start of this article. Stock indexes have little to do with your goals. Later in this series, we will discuss a benchmark that is extremely relevant to every investor but used by a precious few – inflation. Simply, if your portfolio is growing faster than inflation your wealth is growing. However, just because your portfolio beat the S&P 500, it does not mean your wealth is actually growing.

As Ben Graham suggests, investing is not a competition and there are horrid consequences for treating it as such.

Disclosure: The information contained in this article should not be construed as financial or investment advice on any subject matter. Real Investment Advice is expressly disclaims all liability in ...

more