The Myths Of Stocks For The Long Run – Part IV

<< Read More: The Myths Of Stocks For The Long Run – Part III

<< Read More: The Myths Of Stocks For The Long Run – Part II

<< Read More: The Myths Of Stocks For The Long Run - Part I

The Math Of Loss

The “mantra” of “this time is different” is always uttered during ebullient periods in the stock market when “investment risk” is ignored and the pursuit of gains is all that seems to matter. It is during these times where markets “only seem to go up” when statements such as “investing is about ‘time-in’ the market rather than ‘timing’ the market” are made. Such statements are generally regretted in the not-so-distant future.

There is a major point of clarification that needs to be made here. I completely agree that investors cannot be “all in” or “all out” of the market on a consistently correct basis. However, it is at this point in the discussion that some analyst pulls out a chart showing how poor your investment returns would have been if you had missed the “10-best days in the market.”

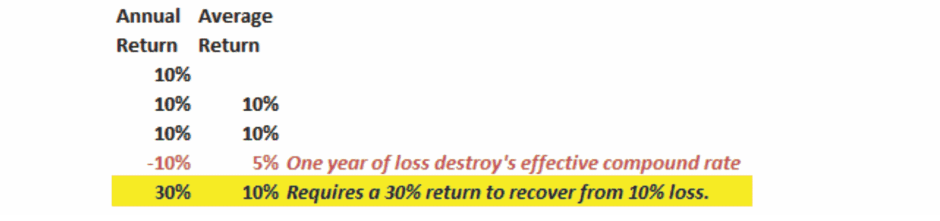

While that bit of information is true, what is never discussed is what happens to investor returns when they capture market losses. The table below shows the damage done to an investor’s portfolio during a market drawdown and the subsequent return required to get “back to even.”

Even a modest 10% correction requires an 11.11% gain just to get back to even. This is why a strategy of “getting back to even” has never been a worthwhile investment discipline.

But it is actually much worse than that when looking at a 10% loss over a longer-term investment time frame.

Let’s assume an investor wants to compound their investments by 10% a year over a 5-year period.

The “power of compounding” ONLY WORKS when you do not lose money. As shown, after three straight years of 10% returns, a drawdown of just 10% cuts the average annual compound growth rate by 50%. Furthermore, it then requires a 30% return to regain the average rate of return required. In reality, chasing returns is much less important to your long-term investment success than most believe.

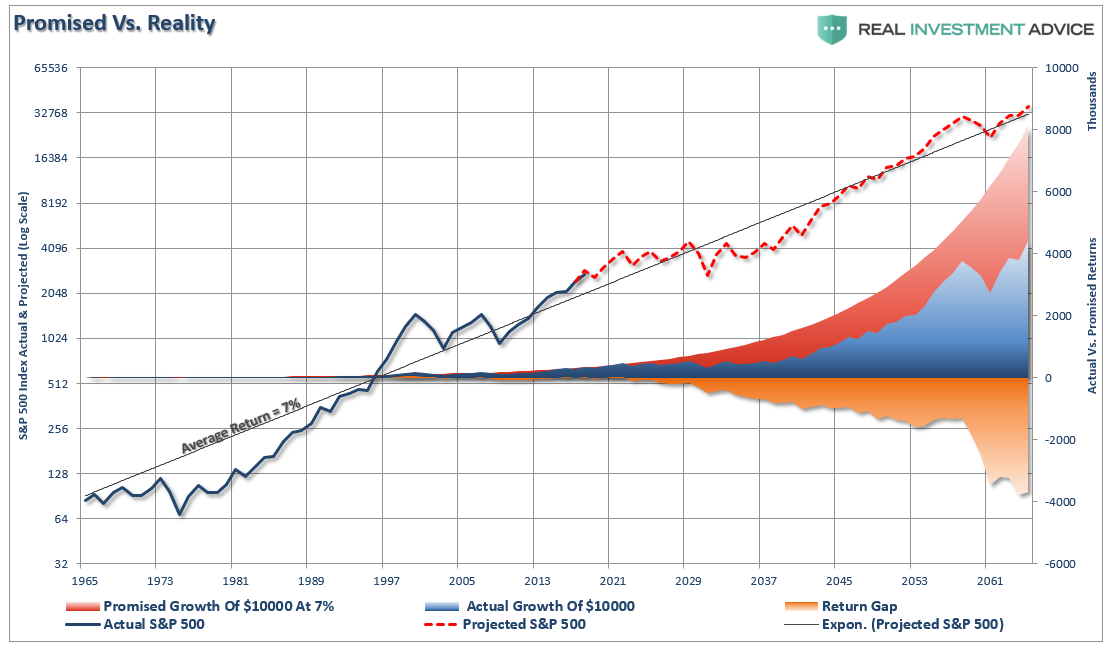

Here is another way to view the difference between what was “promised,” versus what “actually” happened. The chart below takes the average rate of return, and price volatility, of the markets from the 1960’s to present and extrapolates those returns into the future.

(Click on image to enlarge)

When imputing volatility into returns, the differential between what investors were promised (and this is a huge flaw in financial planning) and what actually happened to their money is substantial over long-term time frames.

Not surprisingly, the idea of being “all in the market all the time” turns out to be a poor strategy when viewed in this manner. What bullish prognosticators forget is the importance of capital destruction as it relates to portfolio returns over time. It is also why you should question statements as:

“Losses are just part of investing in the stock market. If you aren’t prepared to lose tremendous amounts of value, you shouldn’t be in stocks.”

Wait a second.

Why should I need to be prepared to lose a tremendous amount of value in my portfolio?

Why can’t I apply some rather simplistic risk management tools, combined with a lower volatility portfolio allocation model, to create returns over time with a lower risk of major drawdowns? After all, is this not one of the most basic tenants of investing: “buy low/sell high?”

Or as Warren Buffett stated:

- Rule #1: Don’t Lose Money

- Rule #2: Refer To Rule #1

Managing The Risk

There are no great investors of our time that “buy and hold” investments. Even the great Warren Buffett sells investments. True investors buy when they see value and sell when value no longer exists.

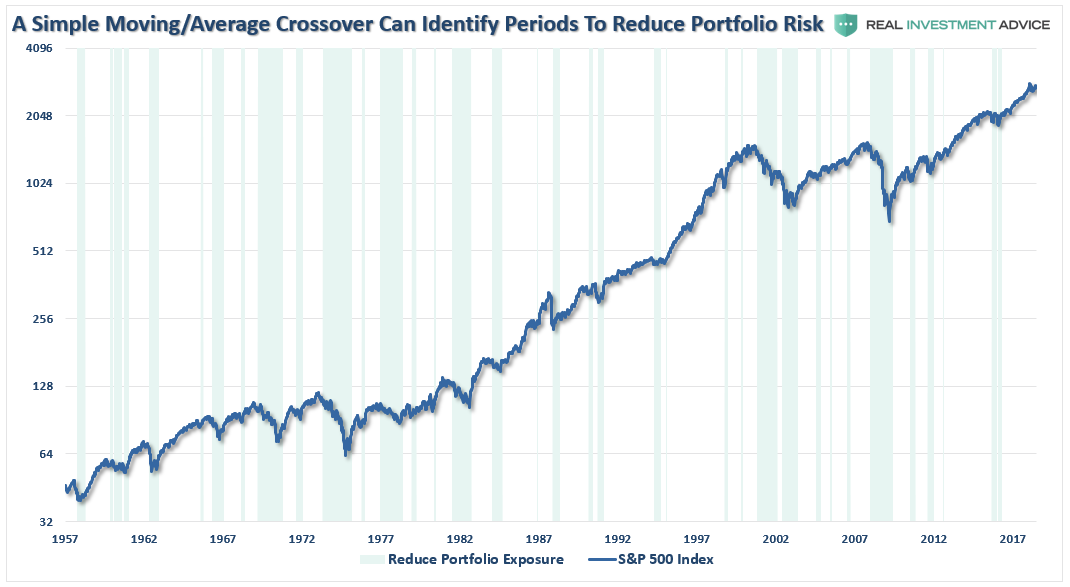

While there are many sophisticated methods of handling risk within a portfolio, even using a basic method of price analysis, such as a moving average crossover, can be a valuable tool over the long-term holding periods.

Will such a method ALWAYS be right? Absolutely not. However, will such a method keep you from losing large amounts of capital? Absolutely.

The chart below shows a simple moving average crossover study. The actual moving averages used are not important, but what is clear is that using a basic form of price movement analysis can provide useful identification of periods when portfolio risk should be REDUCED. Importantly, I did not say risk should be eliminated; just reduced.

(Click on image to enlarge)

Again, we are not implying, suggesting or stating that such signals mean going 100% to cash. We are suggesting that when “sell signals” are given that is the time when individuals should perform some basic portfolio risk management such as:

- Trim back winning positions to original portfolio weights: Investment Rule: Let Winners Run

- Sell positions that simply are not working (if the position was not working in a rising market, it likely won’t in a declining market.) Investment Rule: Cut Losers Short

- Hold the cash raised from these activities until the next buying opportunity occurs. Investment Rule: Buy Low

Missing The 10 Worst Days

With this understanding, let’s revisit the myth of “missing the 10-best days in the market.” The reason that portfolio risk management is so crucial is that it is not “missing the 10-best days” that is important, it is “missing the 10-worst days.” The chart below shows the comparison of $100,000 invested in the S&P 500 Index (log scale base 2) and the return when adjusted for missing the 10 best and worst days.

(Click on image to enlarge)

Clearly, avoiding major drawdowns in the market is key to long-term investment success. If I am not spending the bulk of my time making up previous losses in my portfolio, I spend more time compounding my invested dollars towards my long-term goals.

You Can’t Handle The Volatility

Despite the mainstream attempt at convincing you that it is “time in the market” that matters, the reality is that there have been many periods in history where you simply “ran out of time.”

Here’s another huge myth:

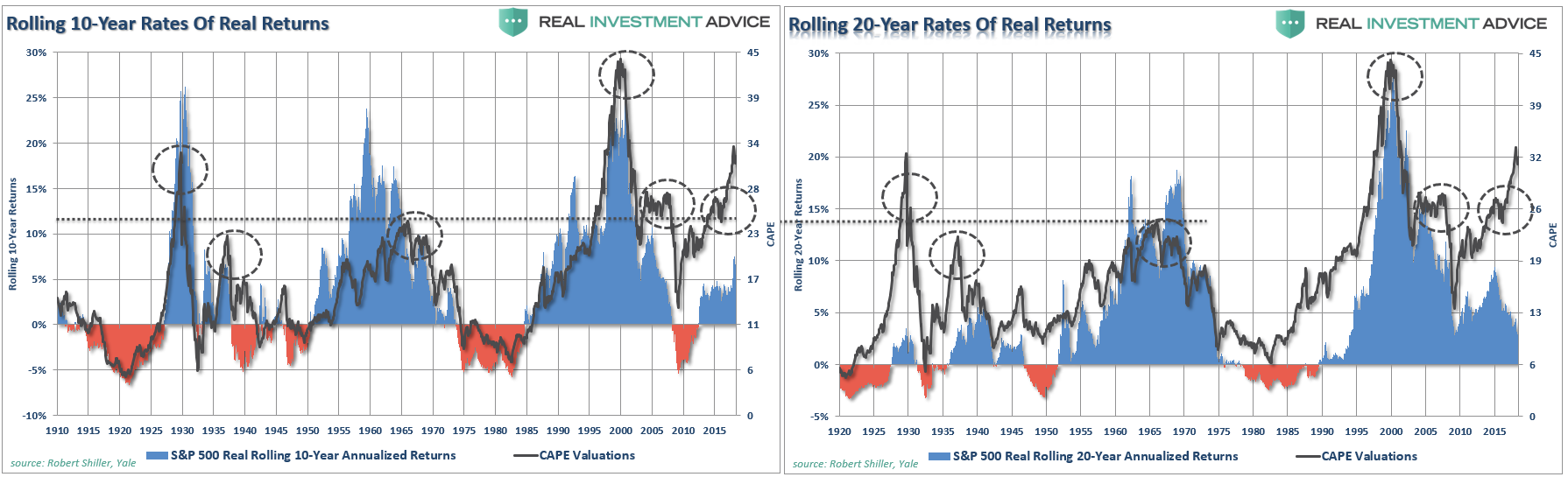

“There has never been a 10- or 20-year period that had negative returns.”

(Click on image to enlarge)

Even on a total return (dividends included) basis, there have been four previous periods, working on the 5th, where a “near zero” 20-year return is not the outcome investors were hoping for. It also left many investors far short of their financial goals.

(Click on image to enlarge)

Of course, such dismal forward returns have only occurred when the starting 10-year cyclically adjusted P/E ratio was above 23x earnings. At over 30x earnings, this would suggest that “time in the market” may not be as beneficial over the next 20-years.

More importantly, it is the “human factor,” a subject we will explore thoroughly in another chapter, which leads to the poorest of outcomes over time. When markets are strongly trending positively, the emotion of “greed” leads to a diminishment as to the appreciation of risk contained within portfolios. Even the worst possible investment mistakes are masked by strongly rising prices. (It is near the peak of these periods when articles espousing “this time is different” and chastising those that “missed the rally…”)

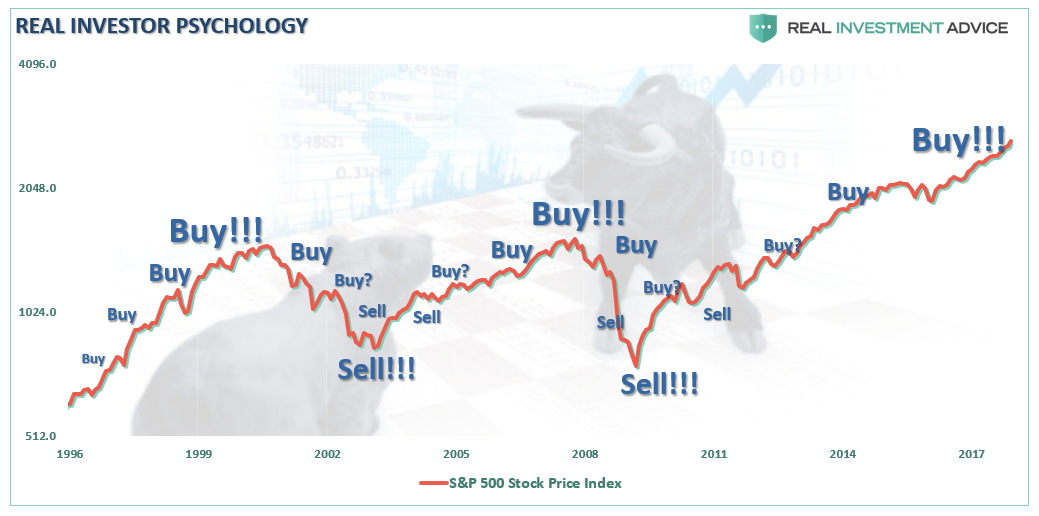

However, it is only after a significant decline in prices, and a large amount of capital destruction, that individuals “panic sell” to stop the “pain of loss” and the risk in portfolios is realized. This is where investors do the most damage to their long-term portfolio goals. I have published the following “investor psychology” chart many times in the past – the message is all too clear.

(Click on image to enlarge)

Let me reiterate this point. A strict discipline of portfolio risk management will NOT eliminate all losses in portfolios. However, it will minimize the capital destruction to a level that can be dealt with logically rather than emotionally.

There is no reason to “benchmark” your portfolio to some random index. The index is a mythical creature, like the Unicorn, and chasing it takes your focus off of what is most important – your money and your specific goals.Investing is not a competition and, as history shows, there are horrid consequences for treating it as such. This is why incorporating some method of managing the inherent risk of investing over the full-market cycle. I would question those who tell you not to do so as they are likely acting from a position of incompetence or self-interest. In the long run, you probably will not beat the index, but you are likely to achieve your financial goals which is why you invested to start with.

Disclosure: The information contained in this article should not be construed as financial or investment advice on any subject matter. Real Investment Advice is expressly disclaims all liability in ...

more