The Great Disconnect: Markets Vs. Economy

The general consensus is the rise in capital markets, despite global weakness, geopolitical risks and sluggish employment and wage growth, is clearly a sign of economic strength as witnessed by rising corporate profitability.

Therefore, stocks are the only investment worth having.

My arguments are much more pragmatic.

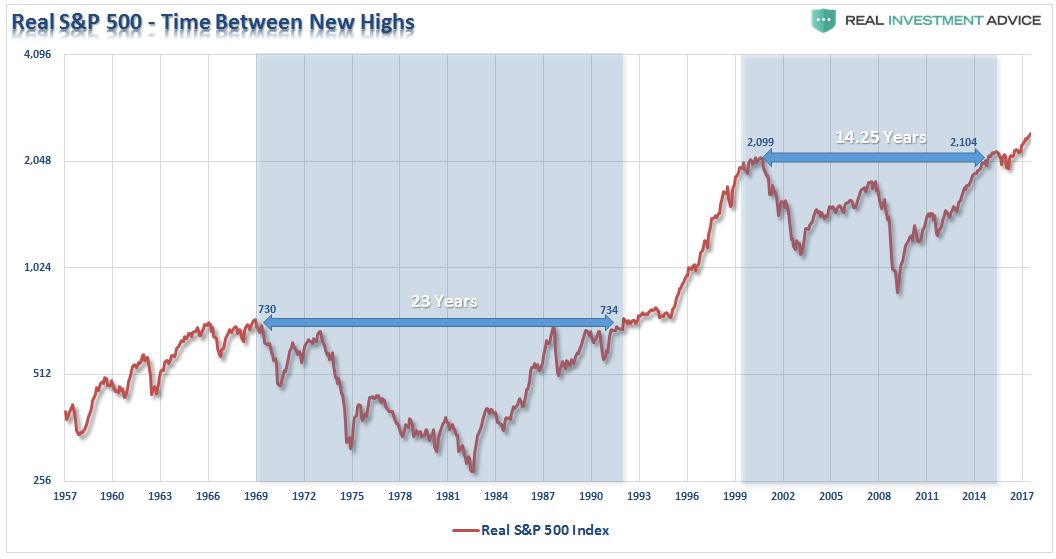

First, it is worth noting that while the markets have risen to “all-time highs,” there was a massive amount of “time” lost in growing capital to meet retirement goals.

This is crucially important to understand as was something I addressed in “Stocks – The Great Wealth Equalizer:”

“By the time that most individuals achieve a point in life where incomes and savings rates are great enough to invest excess cash flows, they generally do not have 30 years left to reach their goal. This is why losing 5-7 years of time getting back to “even” is not a viable investment strategy.

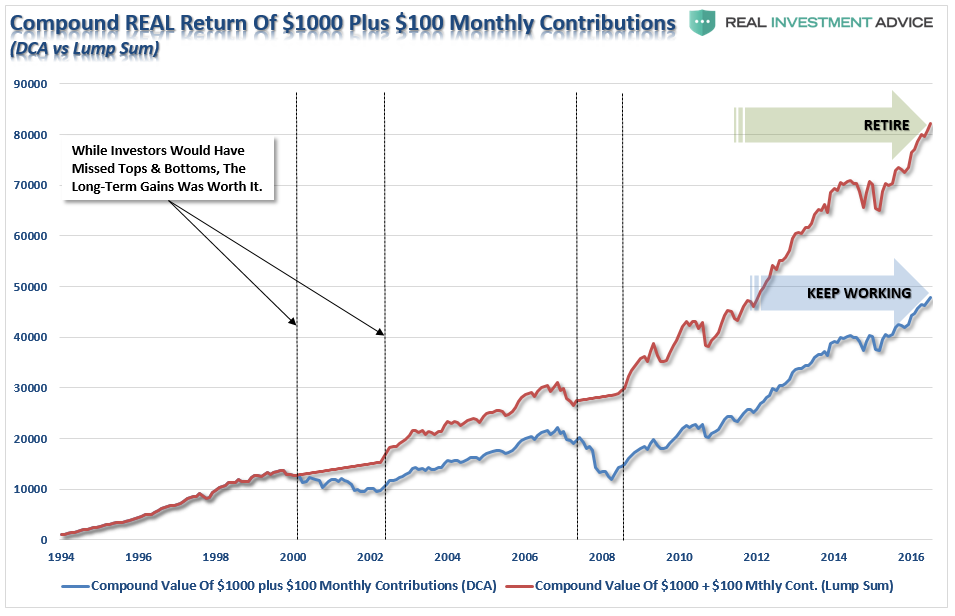

The chart below is the inflation-return of $1000 invested in 1995 with $100 added monthly. The blue line represents the impact of the investment using simple dollar-cost averaging. The red line represents a “lump sum” approach. The lump-sum approach utilizes a simple weekly moving average crossover as a signal to either dollar cost average into a portfolio OR moves to cash. The impact of NOT DESTROYING investment capital by buying into a declining market is significant.”

“Importantly, I am not advocating “market timing” by any means. What I am suggesting is that if you are going to invest into the financial markets, arguably the single most complicated game on the planet, then you need to have some measure to protect your investment capital from significant losses.

While the detrimental effect of a bear market can be eventually be recovered, the time lost during that process can not. This is a point that is consistently missed by the ever bullish media parade chastising individuals for not having their money invested in the financial markets.”

However, setting aside that point for the moment, how valid is the argument the rise of asset prices is related to economic strength. Since companies ultimately derive their revenue from consumers buying their goods, products, and services, it is logical that throughout history stock price appreciation, over the long-term, has roughly equated to economic growth. However, unlike economic growth, asset prices are psychologically driven which leads to “boom and busts” over time. Looking at the current economic backdrop as compared to asset prices we find a very large disconnect.

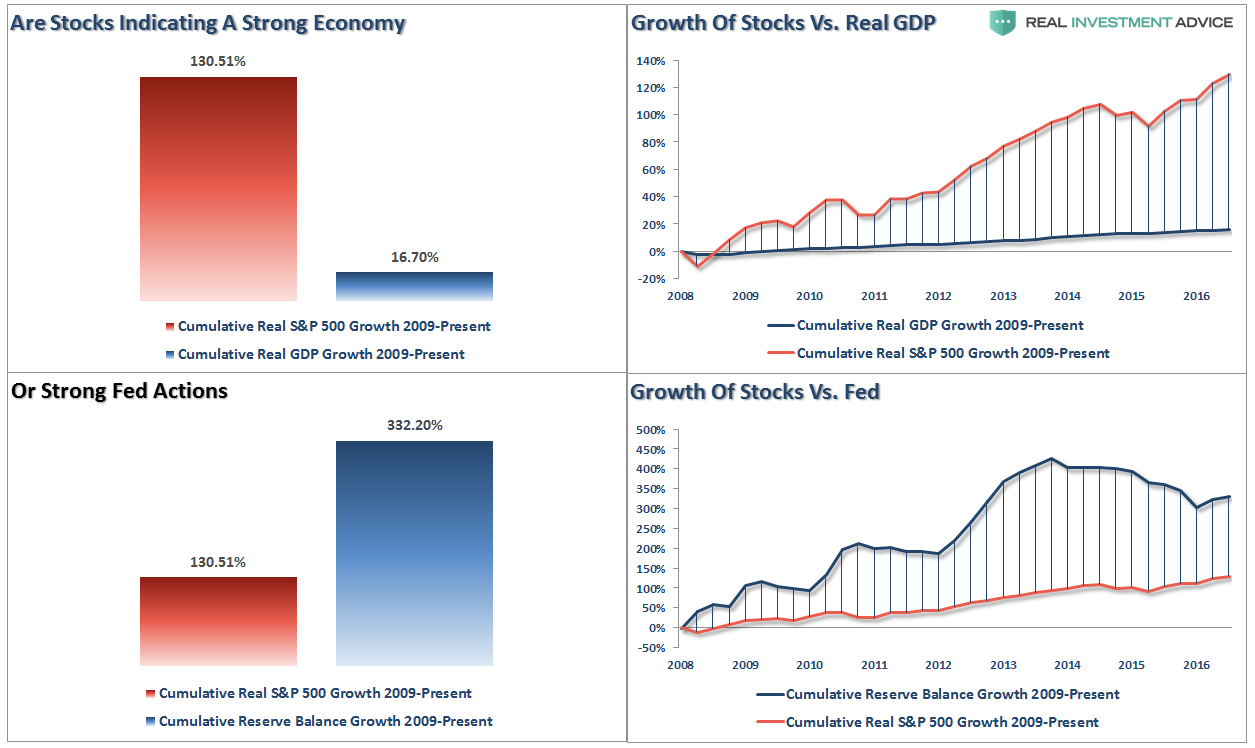

Since Jan 1st of 2009, through the end of June, the stock market has risen by an astounding 130.51%. However, if we measure from the March 9, 2009 lows, the percentage gain explodes to more than 200%. With such a large gain in the financial markets we should see a commensurate indication of economic growth – right?

The reality is that after 3-massive Federal Reserve driven “Quantitative Easing” programs, a maturity extension program, bailouts of TARP, TGLP, TGLF, etc., HAMP, HARP, direct bailouts of Bear Stearns, AIG, GM, bank supports, etc., all of which total more than $33 Trillion, the economy grew by just $2.64 Trillion, or a whopping 16.7% since the beginning of 2009. The ROI equates to $12.50 of interventions for every $1 of economic growth.

Not a very good bargain.

Furthermore, the Fed’s monetary programs have inflated the excess reserves of the major banks by roughly 332% during the same period of time. The increases in excess reserves, which the banks can borrow for effectively zero, have been funneled directly into risky assets in order to create returns.

With the Fed threatening to withdraw the reinvestment from their massive balance sheet, one has to ask just how much risk to asset prices there currently is?

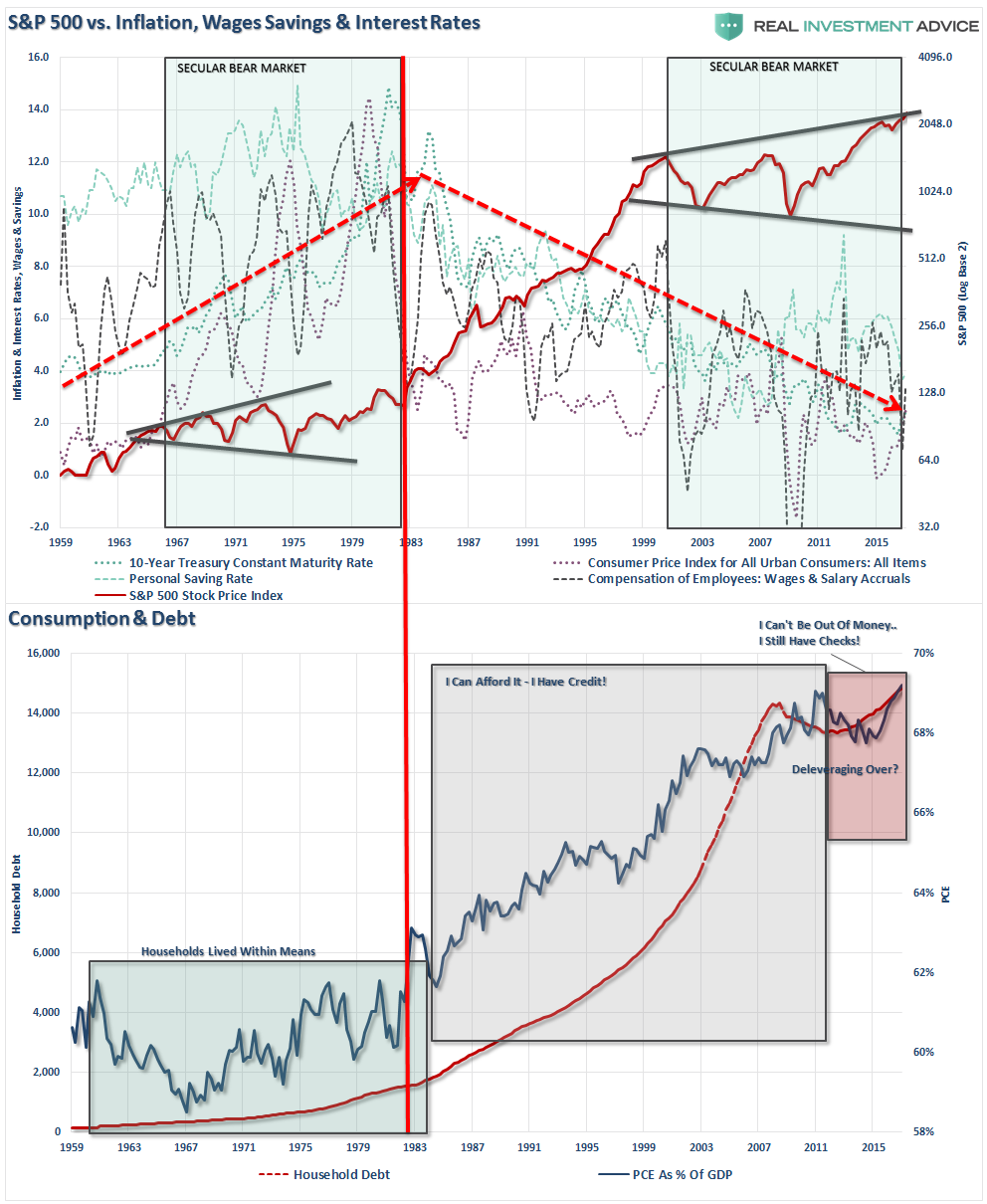

Unfortunately, while Wall Street has benefited greatly from the Fed’s interventions, Main Street has not. Over the past few years, as asset prices surged higher, there has been very little translation into actual economic prosperity for a large majority of Americans. This is reflective of weak wage, economic and inflationary growth which has led to a surge in consumer debt to record levels.

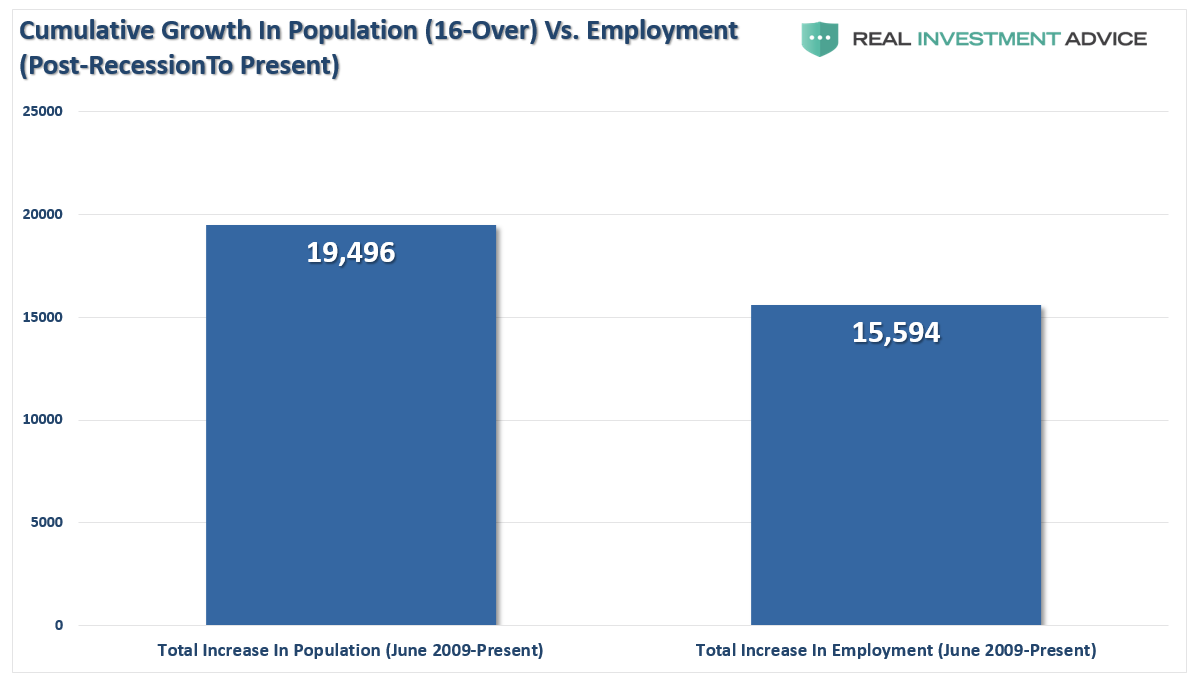

Of course, weak economic growth has led to employment growth that is primarily a function of population growth. As I addressed just recently:

“The first is that the number of ‘real’ employees, while growing, is in lower income producing and temporary jobs, and the rate of job growth is substantially lower than the growth of the population.”

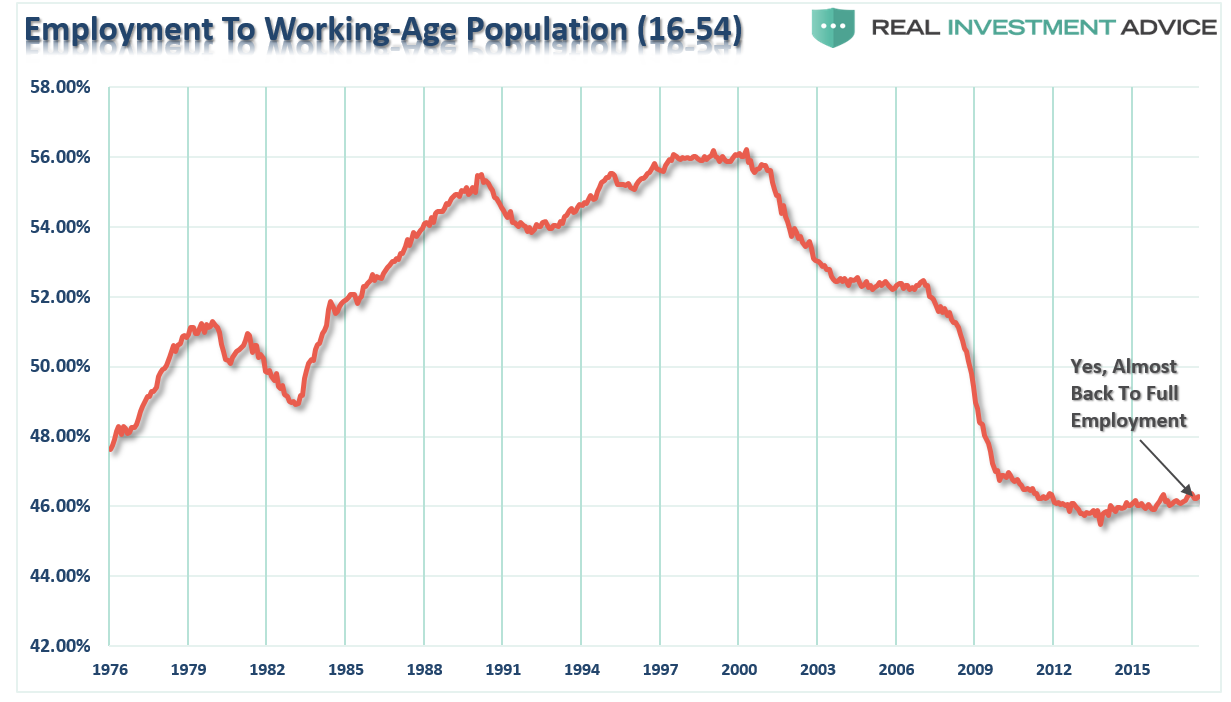

While reported unemployment is hitting historically low levels, there is a swelling mass of uncounted individuals that have either given up looking for work or are working multiple part time jobs. This can be clearly seen in the chart below which is the working age population of those between the ages of 16 and 54 as a percentage of that same age group. (This analysis strips out the argument of retiring baby boomers, who ironically, aren’t retiring, not because they don’t want to, but because they can’t afford to.)

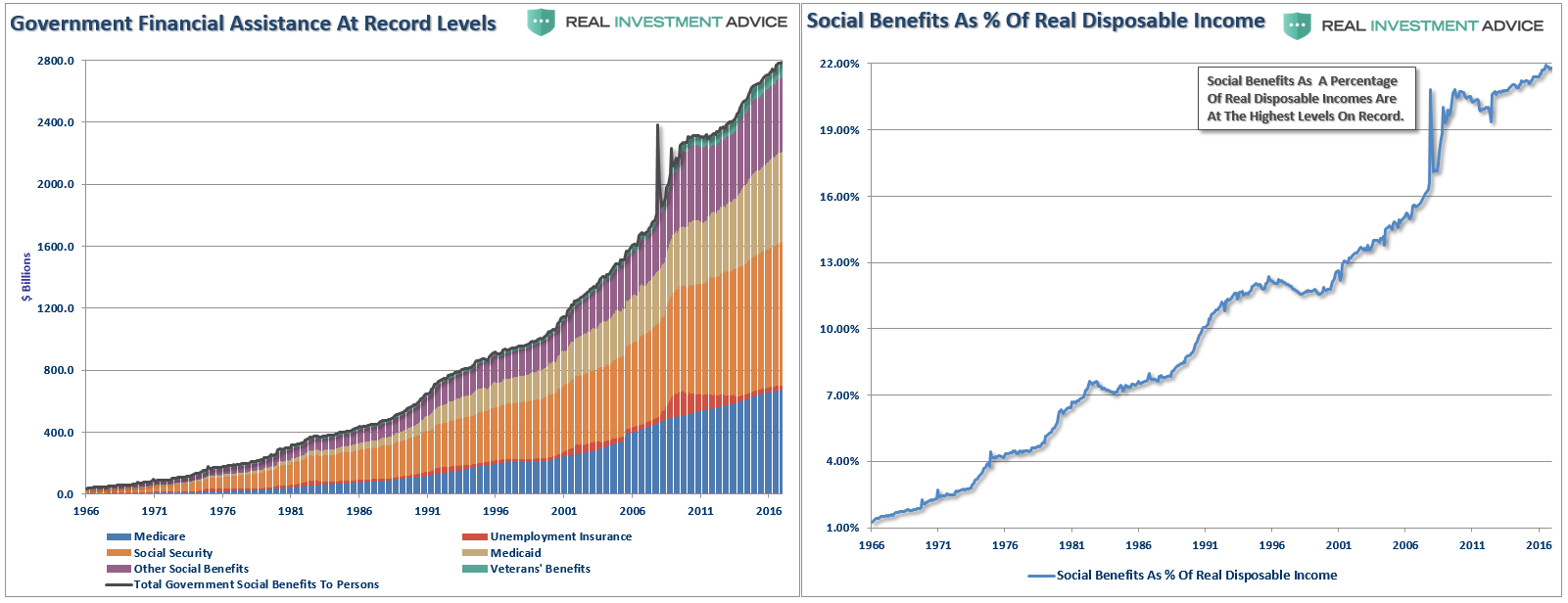

These higher levels of under and unemployment have kept pressures on wages even as work hours have lengthened. The declines in real income are evident as the burgeoning “real” labor pool, and demand for higher wage work, is actually suppressing wages as companies opt for increasing productivity, continued outsourcing, and streamlining employment to protect corporate profit margins. However, as the cost of living is affected by the rising food, energy and health care prices without a compensatory increase in incomes – more families are forced to turn to assistance in order to survive.

Without government largesse, many individuals would literally be living on the street. The chart above shows all the government “welfare” programs and current levels to date. The black line represents the sum of the underlying sub-components. While unemployment insurance has tapered off after its sharp rise post the financial crisis, social security, Medicaid, Veterans’ benefits and other social benefits have continued to rise.

Importantly, for the average person, these social benefits are critical to their survival as they make up more than 22% of real disposable personal incomes. With 1/5 of incomes dependent on government transfers, it is not surprising that the economy continues to struggle as recycled tax dollars used for consumption purposes have virtually no impact on the overall economy.

It is extremely hard to create stronger, organic, economic growth when the dependency on recycled tax-dollars to meet living requirements remains so high.

But, Earnings Have Beaten Estimates?

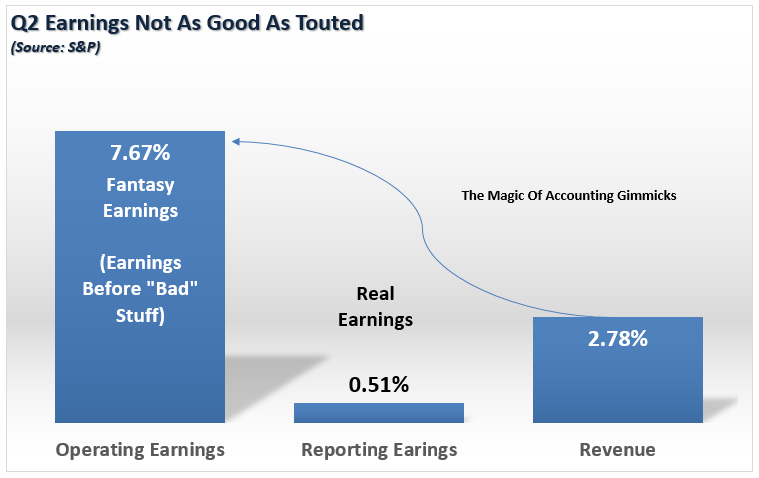

Corporate profits have surged since the end of the last recession which has been touted as a definitive reason for higher stock prices. While I cannot argue the logic behind this case, as earnings per share are an important driver of markets over time, it is important to understand that the increase in profitability has not come strong increases in revenue at the top of the income statement.

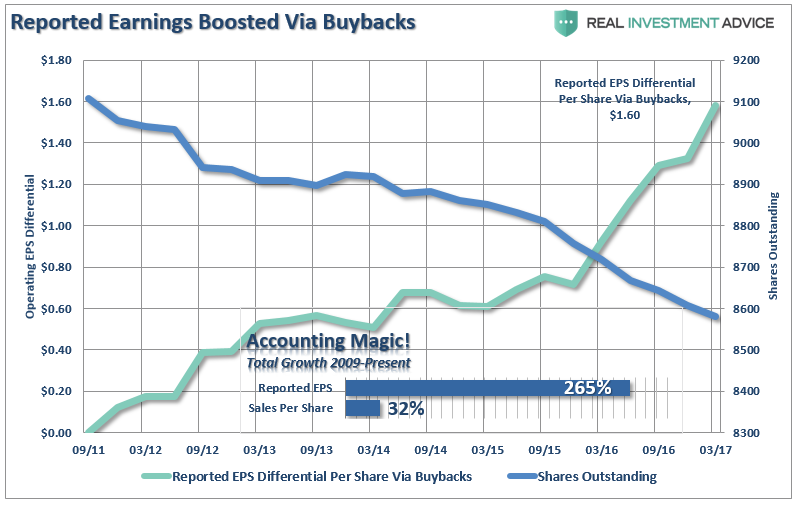

The chart below shows the deviation between the widely touted OPERATING EARNINGS (earnings before all the “bad” stuff) versus REPORTED EARNINGS which is what all historical valuations are based on. I have also included revenue growth as well.

This is a not a new anomaly, but has been a consistent “meme” since the end of the financial crisis. As the chart below shows while earnings per share have risen by over 260% since the beginning of 2009 – revenue growth has barely eclipsed 30%.

As expected, since the economy is 70% driven by personal consumption, GDP growth and revenues have grown at roughly equivalent rates.

While suppressed wage growth, layoffs, cost-cutting, productivity increases, accounting gimmickry and stock buybacks have been the primary factors in surging profitability, these actions have little effect on revenue growth. The bigger problem for investors is all of the gimmicks to win the “beat the estimate game” are finite in nature. Eventually, real rates of revenue growth will matter. However, since consumer incomes have been cannibalized by suppressed wages and interest rates – there is nowhere left to generate further sales gains from in excess of population growth.

So, while the markets have surged to “all-time highs,” for the majority of Americans who have little, or no, vested interest in the financial markets their view is markedly different. While the Fed keeps promising with each passing year the economy will come roaring back to life, the reality has been that all the stimulus and financial support can’t put the broken financial transmission system back together again.

Eventually, the current disconnect between the economy and the markets will merge.

My bet is that such a convergence is not likely to be a pleasant one.

Disclosure: The information contained in this article should not be construed as financial or investment advice on any subject matter. Streettalk Advisors, LLC expressly disclaims all liability in ...

more