Technically Speaking: The Beer Bet

In this past weekend’s article, I laid out my positioning for a short-term rally back to recent highs and why we were looking to “modestly” increase exposure. To wit:

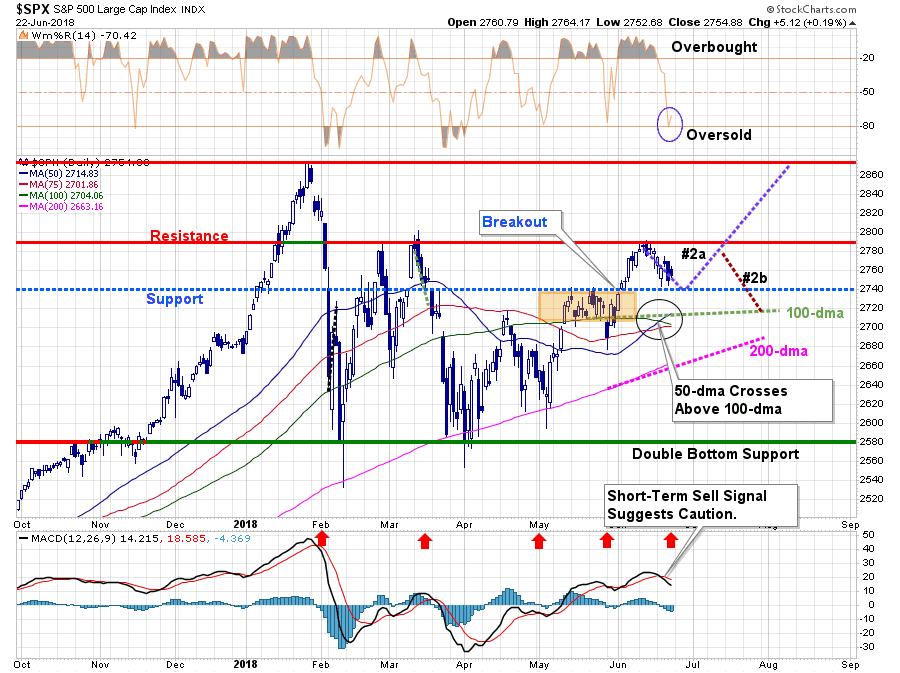

“That is what we got this past week as the market retested the most recent breakout above the Fibonacci 61.8% retracement level twice.

While the weekly ‘buy signal’ did NOT trigger this week, keeping our allocation model at 75%, we have been adding exposure over the last few weeks as the market continued to break out of consolidations. As we stated previously, we were looking for the following setup to add equity exposure to portfolios.

- A retracement back to previous support that did not violate it

- An oversold condition on a short-term basis.

- An opportunistic setup for a continuation of our investment pathway #2a

As shown in the chart below, all three requirements were fulfilled this week. Therefore, on Thursday and Friday, we did increase equity exposure and will look to add more on any weakness in the markets early next week.”

(Click on image to enlarge)

Over the weekend, my friend Doug Kass disagreed with my view:

Coming up Monday morning on @TSTRealMoneyPro -- why I respectfully disagree with my pal @LanceRoberts

— Douglas Kass (@DougKass) June 23, 2018

By contrast I have been building up my net short exposure in the last ten days. https://t.co/t2EmjGHy67

In yesterday’s post, he clarified his reasoning behind his view of more trouble ahead for the market.

“Meanwhile, the partisanship in Washington, D.C. – on both sides of the pew – has never been more pronounced and a disquieting backdrop of animus and hostility reins. The impact of this condition on consumer and business confidence remain unknown.

Valuations are contracting, stocks are beginning to ignore good results (e.g., Micron Technology (MU) ) and the risks of policy (both fiscal and monetary) miscues are rising — at a time in which monetary policy around the world is pivoting towards tightening.

Meanwhile, the benefits of the corporate tax reduction is trickling up and not trickling down.

I was long as the S&P Index rose in early June. but I moved back into a net short exposure (via defined risk (SPY) puts and with a short (QQQ) ) at mid-month as signs of global economic ambiguities multiplied, investor optimism grew and the threat of policy mistakes increased — and the downside risks were heightened as measured against upside reward.

- Market Downside: 2400 to 2450

- ‘Fair Market Value’: 2500

- Trading Range: 2550-2750 to 2800

- Current S&P Cash (Adjusted for this morning’s future drop): 2735

Here are the current reward versus risk parameters (based upon the -15 handle drop in S&P futures, 2735 S&P equivalent):

- There are 310 points of downside risk against only 65 points of upside reward (compared to the top of the expected trading range) in my new pessimistic case (2400-2450). This is an overwhelmingly negative reward vs risk ratio (5:1).

- Compared to ‘fair market value,’ (2500) there are 235 points of downside risk versus only 65 points of upside reward. That’s a negative 4:1 ratio.

- Against the expected trading range, there are 185 handles of downside risk and only 65 points of upside reward (to the top end of the anticipated trading range). That’s a 3:1 adverse ratio.

There are more Shades of 1999 and signposts that FAANG may have peaked, while we face a new regime of volatility reflecting a host of factors and the possibility of increased economic and market outcomes (many of which are adverse).

A changing market complexion is occurring coincident with global monetary tightening – making equities and other long-dated assets less attractive as the risk-free rate of return expands.”

I don’t disagree with Doug’s outlook at all. Although, we did place a friendly wager on a very short-term outcome.

— Douglas Kass (@DougKass) June 25, 2018

While I have indeed maintained a bit more bullish stance as of late due to a confluence of factors, I have also consistently recognized the risks which remain. As I wrote this weekend:

“There is risk to the outlook, however. With the short-term sell signal triggered last week, it does keep us cautious. However, as we have seen previously, such a signal can be reversed quickly. Also, with the 50-dma crossing above 100-dma, further support for a continued bullish advance is back in place.

Importantly, while we are indeed more ‘bullishly inclined’ at the moment, and are willing to give the bulls a bit of ‘running room,’ we have moved stops up. We are also keeping our tolerance for losses restricted as downside risk continues to outweigh reward over the intermediate term.

We still remain slightly overweight in cash, and underweight equities, as the late-cycle risk and trade issues remain heavily prevalent.”

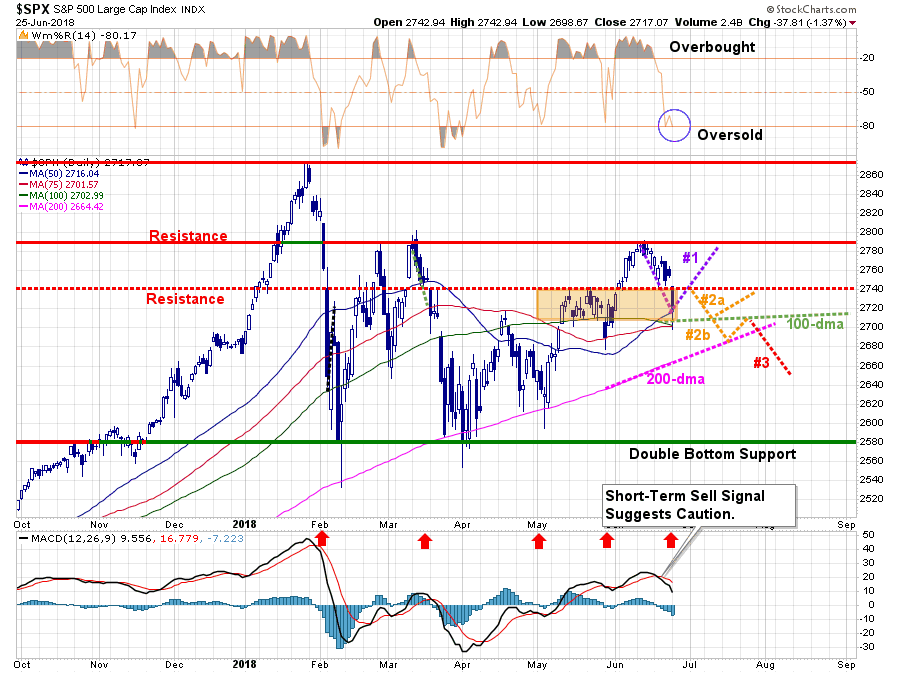

Doug won the bet yesterday as the market cracked the 100-dma and certainly raises the risk profile of market currently. However, while the breakdown yesterday is certainly concerning, there is a confluence of support at the 100-dma which coincides with the 50- and 75-dma as well. Also, there is a rising trend line from the March lows which provides additional support at current levels. With the market oversold, the bulls must make a stand here and defend these levels.

(Click on image to enlarge)

Because of the breakdown on Monday, we DID NOT increase equity exposure in portfolios as of yet. With 50% of portfolios currently in cash and fixed income, the damage from yesterdays sell-off was mostly mitigated. (This is the advantage of cash and fixed income in a volatile market.)

The good news, if you want to call it that, is the cluster of support, as noted above, is now critically important. A break below these levels brings Doug’s lower ranges into view very quickly with the first real test coming at the 200-dma.

With this idea in mind, I updated the pathway chart above to take into account these potential outcomes.

Pathway #1: Given the recent tendency for bulls to rush in to “buy the dips,” the current oversold condition on a short-term basis provides enough “fuel” to support a rally back to recent highs. (30%)

Pathway #2a: Given both the short-term oversold condition AND the confluence of support at the 100-dma, the market is able to rally back to 2740 remains confined to a tight trading range between the 100-dma and 2740. (30%)

Pathway #2b: follows the path of #2a but fails to hold support at the 100-dma and quickly falls to test support at the 200-dma. The market will be deeply oversold at that point, so a rally back to the 100-dma is probable. If the market fails to move above 100-dma then a break below the 200-dma becomes probable and brings Pathway #3 into focus. (40%)

And just like the first rule of “Fight Club” – we do not talk about “Pathway #3.”

Actually, we will, we just aren’t there yet.

Should a break of the 200-dma occur we will be discussing much more about the onset of a cyclical bear market, risk reduction, and hedging. While I remain “hopeful” the market can regain its stability and continue to quickly compensate for Trump’s trade rhetoric, “hope” is not an investment strategy.

As I stated previously, these “pathways” are how we assess the risk of potential outcomes in a market that is experiencing much higher levels of price volatility than what we have seen previously. As longer-term investors, we “hope” to invest capital that will grow over time, but given the rising risks of a late stage market cycle, reductions in market liquidity, and tighter monetary policy we maintain a focus on capital preservation.

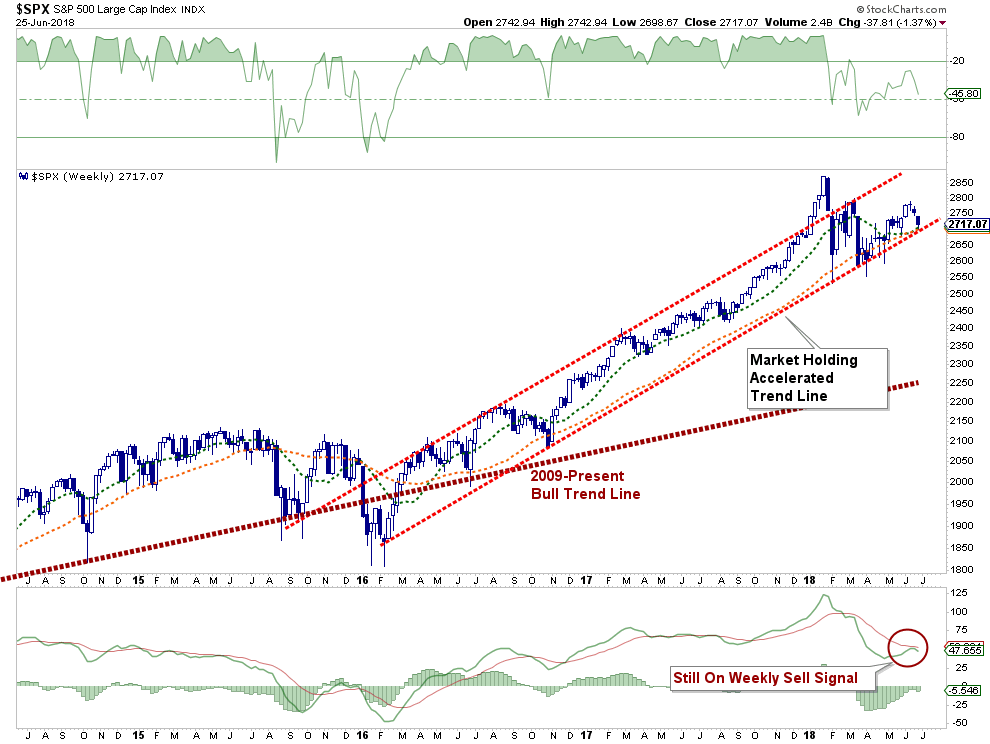

There is a strong rising bullish trendline from the 2016 lows which coincides with both the short and long-term moving averages. This provides fairly strong support for the market on an intermediate-term basis which keeps us allocated to equities currently.

(Click on image to enlarge)

Any confirmed break below 2710 on a weekly basis, a break which fails to recover, will most likely signal the onset of a protracted bear market. With no real support, until you reach the long-term bullish trendline from 2009, there is roughly 500-points of downside risk. I certainly don’t plan to “hold” equities “long” during such an event.

For now, I continue to allow excess cash and bonds to continue to offset the short-term volatility.

One thing is for sure, things are starting to get much more interesting. As I stated a couple of weeks ago, we are still giving the “bulls the benefit of the doubt” momentarily, however:

“…we do so with a risk-management process in place. We encourage you to do the same. If you don’t have one, it might be time to develop one.”

Or find someone to do it for you.

Now, I just have to figure out how to get a case of beer across state lines.

Disclosure: The information contained in this article should not be construed as financial or investment advice on any subject matter. Real Investment Advice is expressly disclaims all liability in ...

more