Technically Speaking: Buy The Dip?

In this past weekend’s newsletter, I reviewed every S&P sector and several major markets to analyze the risk/reward opportunities that currently exist. In a nutshell, there really weren’t many. To wit:

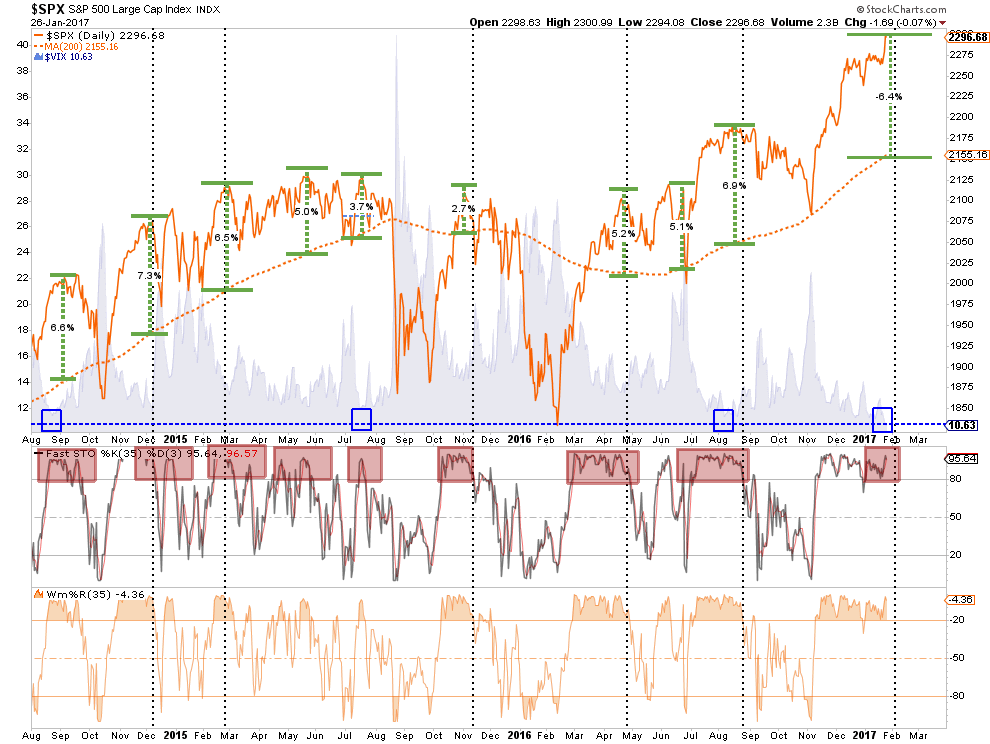

“We can also witness the rather extreme extension of prices above the 200-dma. Such extensions, which are always combined with extreme overbought conditions, have typically not lasted long and have been a good indication to take profits in the short-term. This provides some opportunity to invest capital following a correction to some level of support.”

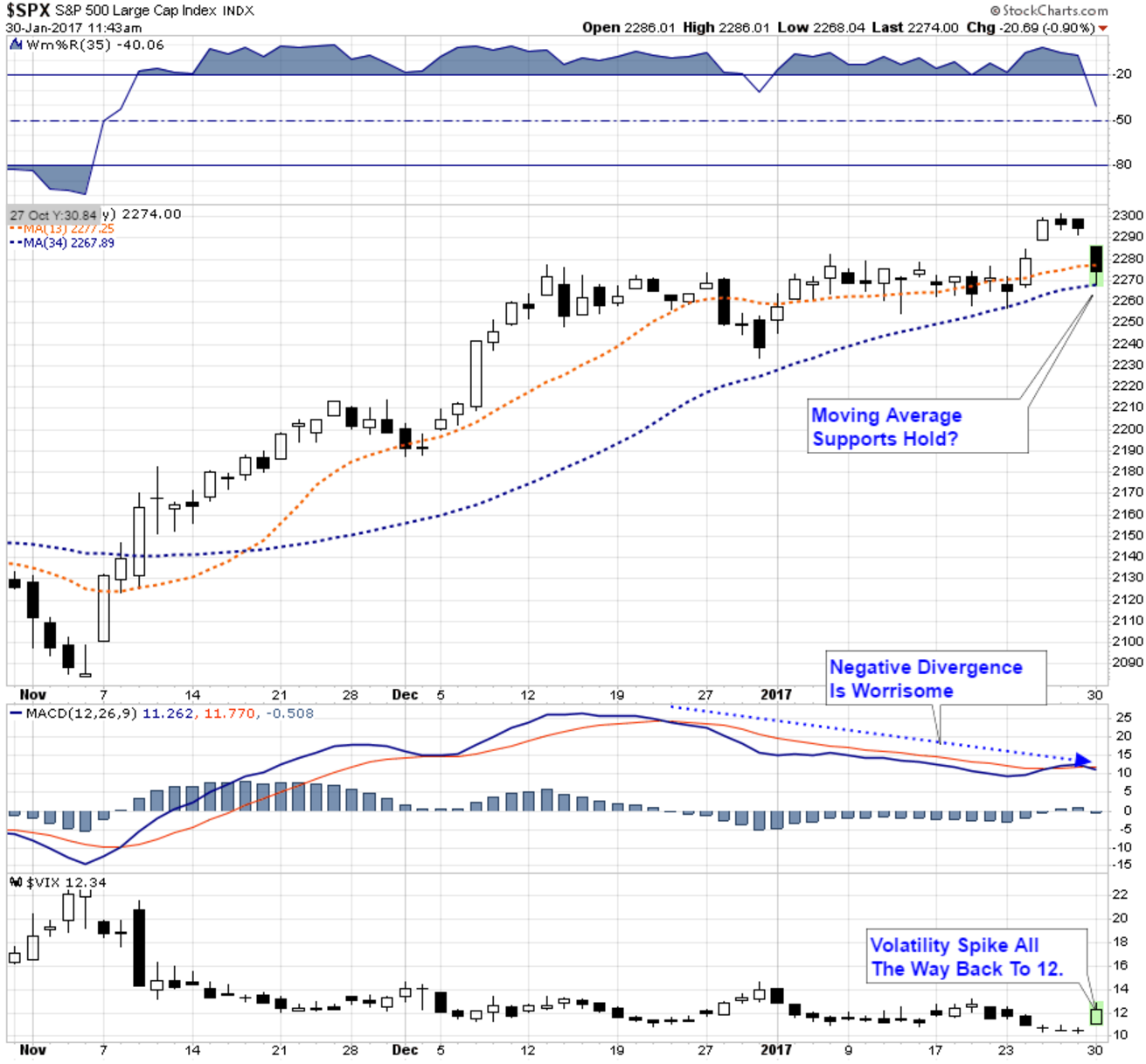

On Monday, the market reversed much of the advance from last week as a spike in volatility pressured stocks lower. Importantly, one of the bigger concerns, from a short-term risk assessment view, has been the negative divergence of the MACD (moving average convergence divergence) with the potential of a short-term sell signal. The combination of these suggests a larger corrective action may be in store.

BUY THE DIP?

Which brings us today’s questions. How big of a correction might we expect and should it be bought?

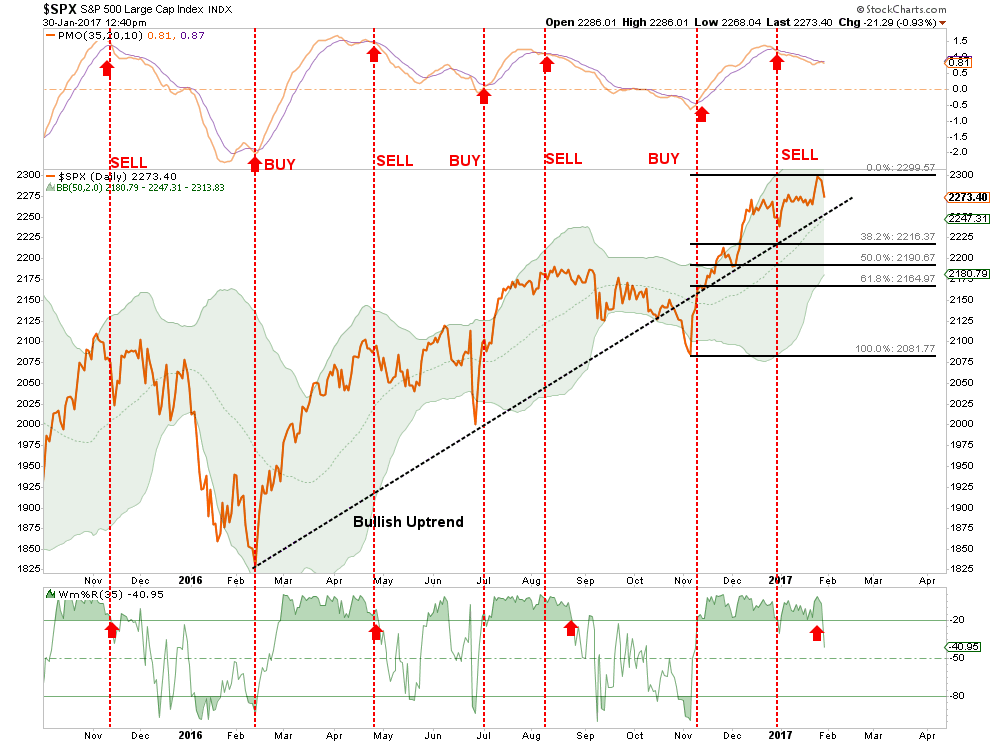

For the answer to the first question, we can review recent support levels and make some educated guesses. The first chart below shows the standard Fibonacci retracement levels for the S&P 500 from the previous lows. Initially, the market should find support at the retest of the bullish trend line from the February 2016 lows. A failure there will be a retracement of 38.2% of the recent advance to roughly 2300.

Importantly, I have noted with vertical dashed red lines the buy and sell indications relative to the markets subsequent direction. In each case, a registered sell signal at the top of the chart, and confirmed by a reversal of the bottom indicator, have led to short and intermediate-term corrections in the market. These two signals should not be ignored.

The next chart attempts to quantify several potential correction levels from the recent highs.

In this analysis, the correction could be as small as 2.7% or potentially as large at 13.2%. This is quite a dispersion of outcomes and one we will only know with certainty after the fact. However, recent history has suggested that similar setups have seen deeper corrections so such risk should not be readily dismissed.

Given the overall optimism of the markets, currently based solely on “hopes” of fiscal policy forcing fundamentals to catch up with price, the most likely outcome is the market finding support between the 4.9% and 6.6% correction levels. This should not be any surprise since the markets have suffered 5% corrections, or more, with regularity over the past couple of years.

Secondly, should you “buy this dip?” Probably. As I quoted in this weekend’s missive:

“So that keeps telling me that the highest probability outcome remains for lower-highs and lower-lows in VIX.

And that keeps happening in a US Equity market that is often called ‘expensive’ (it is), but doesn’t get cheaper. Maybe someone from the orthodoxy of macro ‘valuation’ experts can chime in on why this is happening.

I think it’s because consensus continues to position for a correction that would be deemed “rational”, as opposed to buying all dips in an irrationally profitable position that’s been complimented by prevailing growth and inflation conditions.

Can the U.S. stock market get more expensive? Absolutely.”

I don’t disagree with the point. There are TWO very important lessons that should not be forgotten at this late stage of the market’s advance.

“The market can remain irrational, longer than you can remain solvent.” – J. M. Keynes

“In a bull market, you can only be long or neutral.” – D. Gartman

Currently, there is little indication any correction in the short-term will lead to the beginning of a full-blown bear market reversion to the mean.

But, more importantly, there never is.

Last Leg?

There continues to be several warning signs which continue to persist despite ongoing hopes that “Trumponomics” will create the backdrop for a fiscal policy driven continuation of the “bull market” advance.

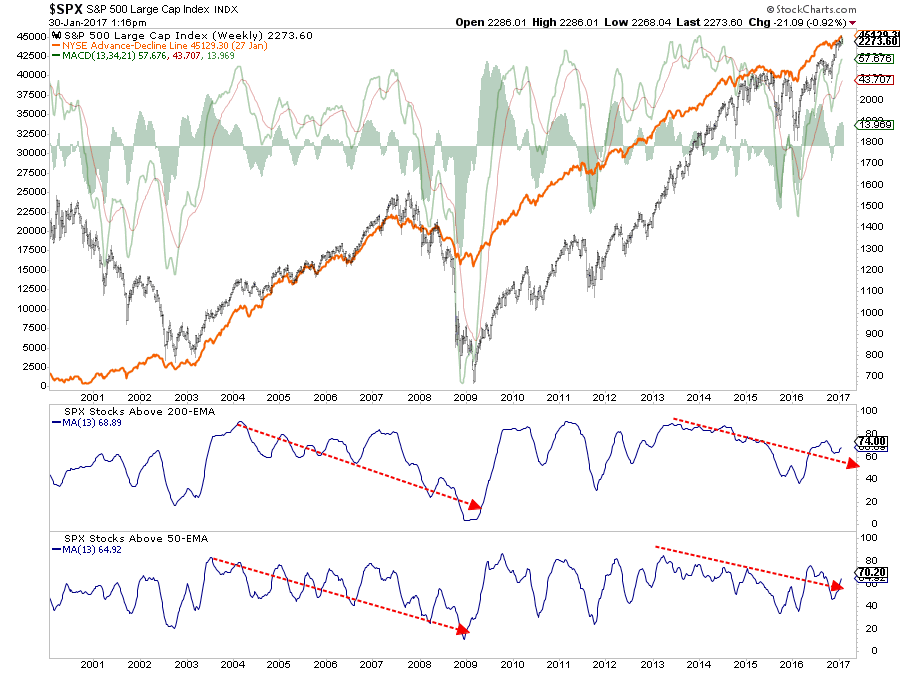

The first is the ongoing negative divergence of stocks above the 50 and 200-day exponential moving average. As shown below, the last time this occurred was heading into the peak of the market in 2007. Look for a sharp decline in both indicators towards the 20-level to confirm a top is most likely in.

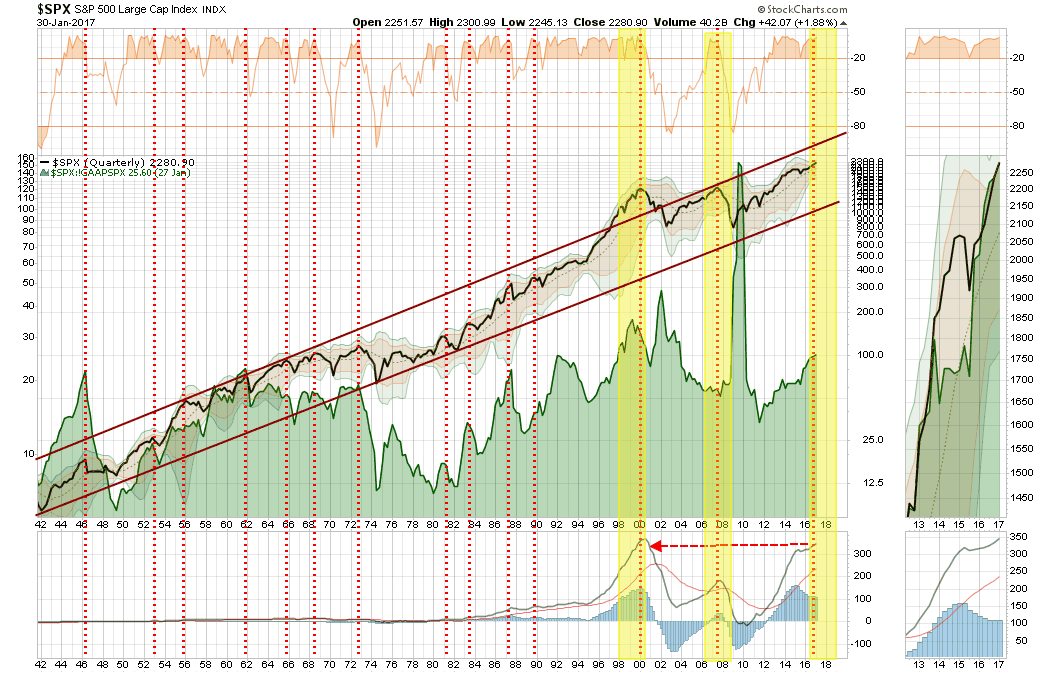

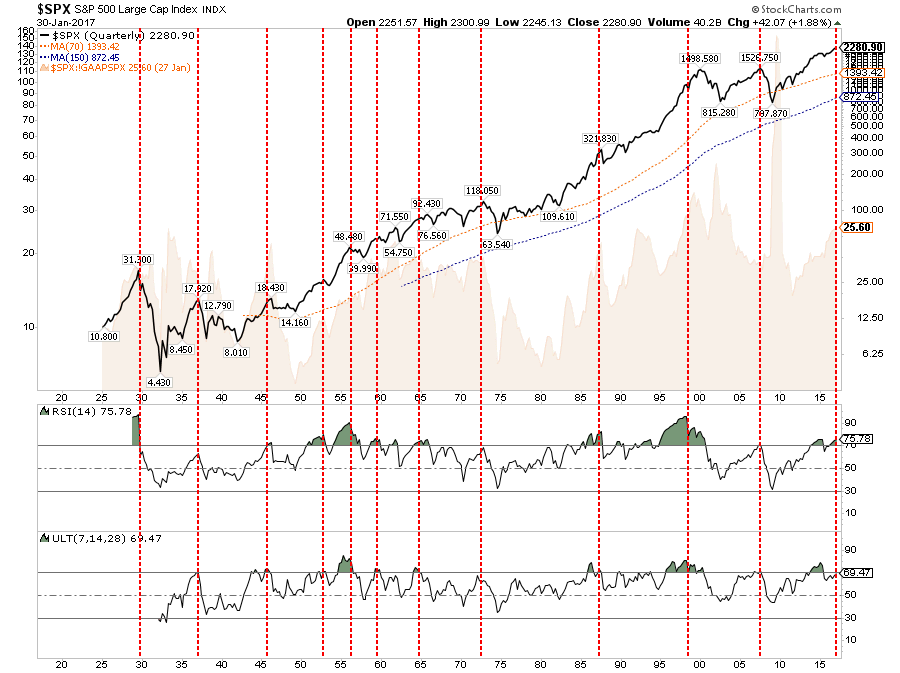

On a long-term scale, the market is now pushing 3-standard deviations of its 3-Year moving average (12-quarters) This is a historical rarity and as always denoted the end, rather than the beginning, of an advance. However, given this is a quarterly indicator, it is extremely slow to move which means the market can get even more extreme first.

Also, as shown below, historically when both the RSI and Ultimate Oscillator have simultaneously reached such high levels on a quarterly basis was also at more important market peaks. Again, this is a very slow-moving indicator but is noteworthy nonetheless.

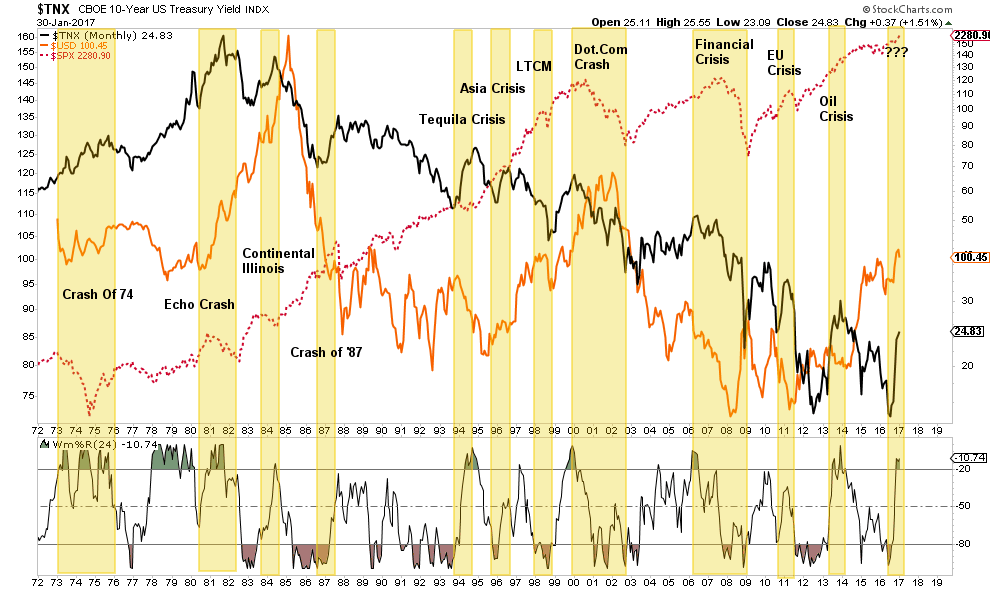

It is also worth noting that sharp rises in interest rates, particularly when combined with an overbought, overbullish and extended market have generally had short to intermediate-term problems.

As David Rosenberg pointed out over the weekend:

“This time around, not only are valuations at 15-year highs but we’re entering it into the eighth year of the expansion of the bull market. You have to respect where were you are in the market cycle in the business expansion and we’re much more mature now than we were in that early stage of Reagan or you can argue the early stage of Bill Clinton or Barrack Obama. I mean the benefit of being elected at the bottom of the cycle, then you can just ride it up and just take credit for it. I think that the challenge for Donald Trump with all deference to the animal spirit rally they were seeing right now is that the multiples are really stretched and that maybe if were not even in the ninth inning of the game here, we’re certainly somewhere in or around the seventh inning stretch. So, the answer is no. It’s not like Ronald Reagan at all in that regard

So basically, I’m supposed to take it at face value because the markets are telling me that this is their view today, and their view today might not be the market’s view 3, 6, 12 months from now or 5 years from now. But the market’s telling me that one man, President Trump is gonna be able to, with fiscal policy, will be able to do what Bernanke and Yellen and Draghi and Trichet and Koroda and Carney, who actually run the printing presses, what they couldn’t do in the past 8 years a president’s gonna be willing to do, or be able to do, on inflation? And the answer is no. That’s just not gonna happen.

What did inflation do during this supply side Reagan era? Went from 12 percent to down below 5 percent over his 8-year term? Why anybody thinks that Trump’s policies themselves are gonna create inflation, I can’t build an inflation view out of that.”

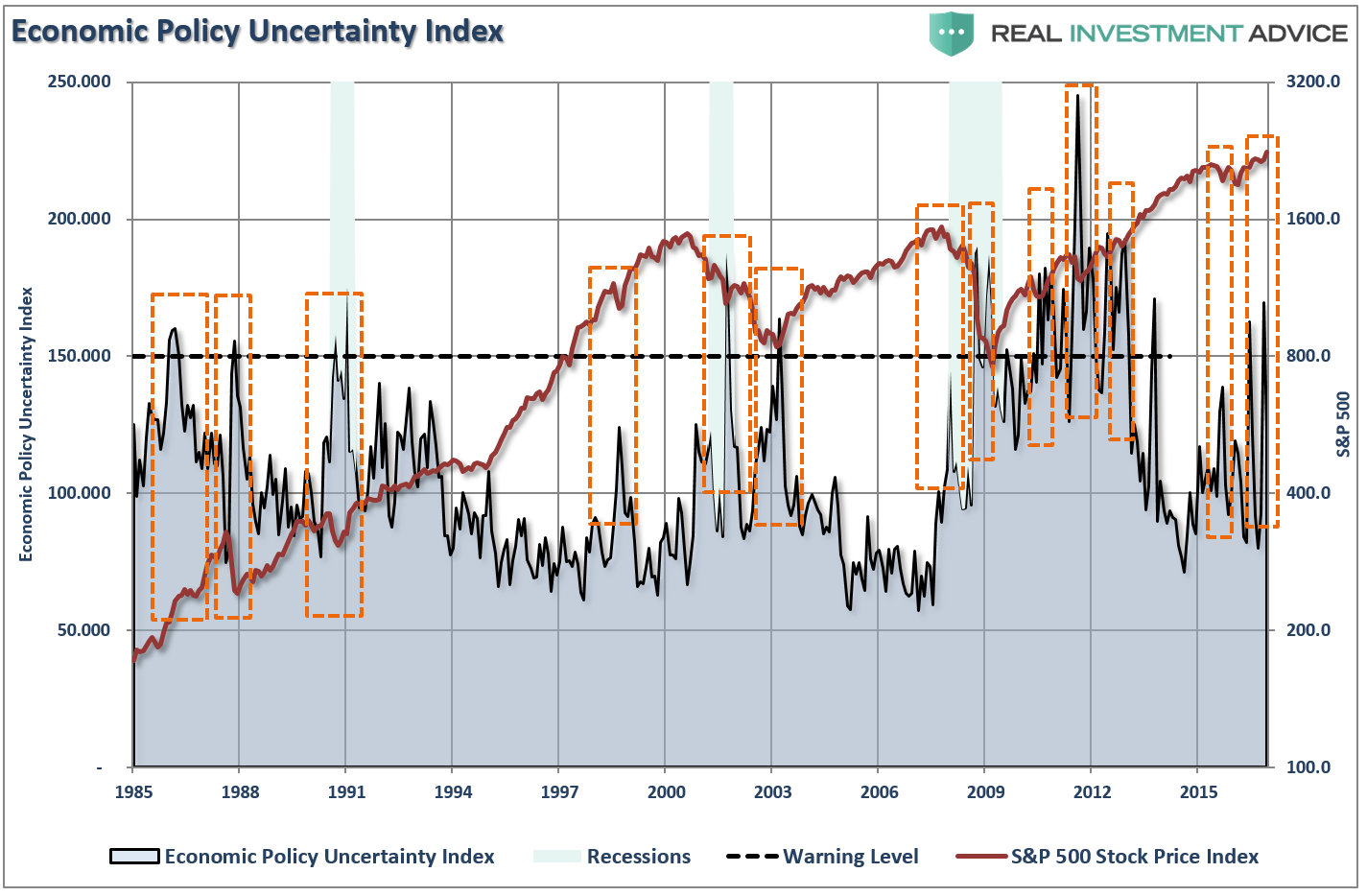

What if he’s right? And maybe that is exactly what the Economic Policy Uncertainty Index is telling us.

Hedging Risk

What I am fairly certain of is that we are unlikely to exit this year without a fairly sharp reversion at some point along the way. What I don’t know is the timing or catalyst of a more meaningful bear market.

Therefore, there are a few actions to take in order to hedge risks in portfolios currently. There is nothing fancy about hedging risk, it is just about taking action to do so.

Keep it simple.

There are many ways to get very complex hedging risk from utilizing options, shorting, etc. The problem is that you are transferring the risk of being wrong, and losing capital, from one side of the balance sheet to the other. As noted above in a “bull market,” which we are clearly in currently, only be “neutral” or “long.” In a “bear market,” when the trend has become negative, then you can be “neutral or short.”

Therefore, hedging risk currently is about taking steps to reduce risk and become more neutral until a better risk/reward opportunity is presented for being long.

Clean Up Your Portfolio – Bull Markets Make Us Lazy

- Tighten up stop-loss levels to current support levels for each position.

- Take profits in positions that have been big winners

- Sell laggards and losers

- Rebalance portfolios to target weightings

- Raise cash and reduce overall equity risk exposure to more conservative levels.

- Look to increase fixed income exposure as part of a “risk off” trade.

The election has injected a huge amount of undue and misplaced optimism in the market. Such periods of exuberance have previously ended badly for investors.

While I am still currently long the market, I remain aware of the risks.

If I am wrong, and the market does indeed somehow manage to launch into a full-fledged, viable bull market, then I will adjust risk exposure higher in portfolios.

But what if I am right? How long will it take you to get back to even this time?

Disclosure: The information contained in this article should not be construed as financial or investment advice on any subject matter. Streettalk Advisors, LLC expressly disclaims all liability in ...

more