Can The Fed Really Boost Bond Yields?

One of the biggest issues with predictions of rising 10-year bond yields since “bond bears” came out in earnest in 2013, is they have been consistently wrong. For a bit of history, you can read some of my previous posts on why rates can’t rise in the current environment.

- Bond Bears & Why Rates Won’t Rise

- Why Bonds Aren’t Overvalued

- People Buy Payments

- Rates Continue To Defy Logic

- Rates, GDP & Challenges

As we head into 2018, and beyond, there are many reasons why rates will remain subdued all of which are economic and fundamental in nature. However, a recent article by Wolf Richter peaked my attention:

“The Fed’s “balance sheet normalization” will accelerate as 2018 progresses: In Q1, the Fed is scheduled to shed $60 billion in securities, in Q2 $90 billion, in Q3 $120 billion, and in Q4 $150 billion, for a total of $420 billion. This is scheduled to increase to $600 billion in 2019.

And if the Fed wants to spook the markets into jacking up long-term yields, it could accelerate further its ‘balance sheet normalization.’ For the first time in history, the Fed can actually do something that will drive up long-term yields.”

This is an interesting concept and, if Wolf is correct, would be a monumental shift in a market that is 4-times the size of the stock market.

But I am not so sure I agree.

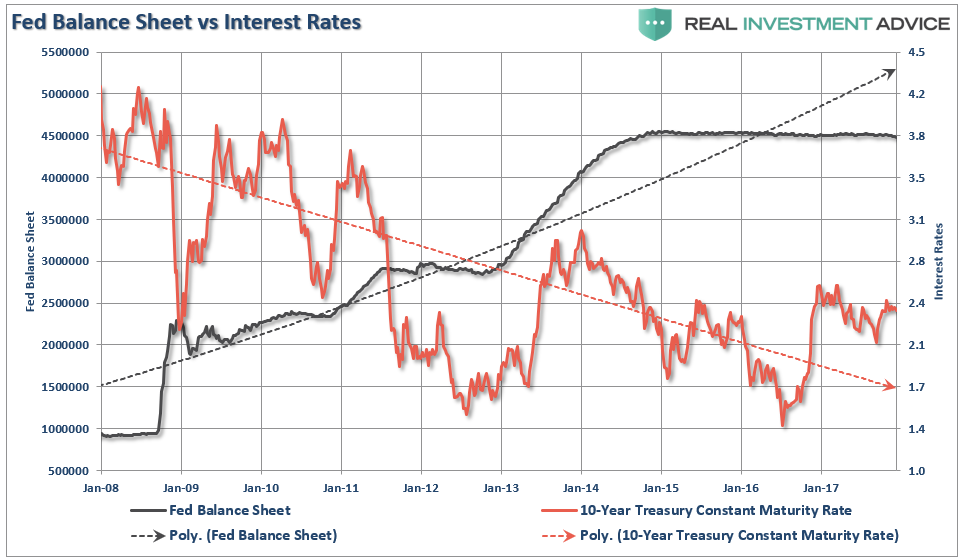

During the Fed’s brief history with unprecedented liquidity injections into the financial markets, there have been previous occasions where the Fed’s balance sheet was reduced as shown in the chart below.

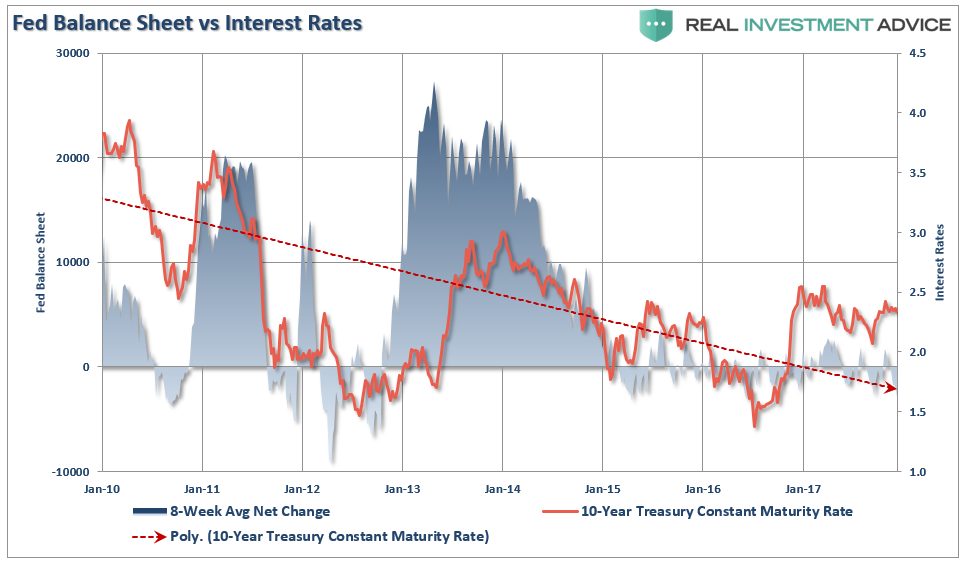

Each time, when liquidity was extracted from the financial markets, the rotations from “risk” to “safety” pushed yields lower. Not higher. The chart below is the 8-rolling average of the Fed’s balance sheet which more clearly shows the correlation.

The correlation makes complete sense when you think about it. When the Fed is expanding their balance sheet, money flows into the equity markets driving “risk” assets higher. With the reduced need for “safety,” money rotates from bonds into stocks on an asset allocation basis. The opposite occurs when the Fed extracts liquidity from the markets.

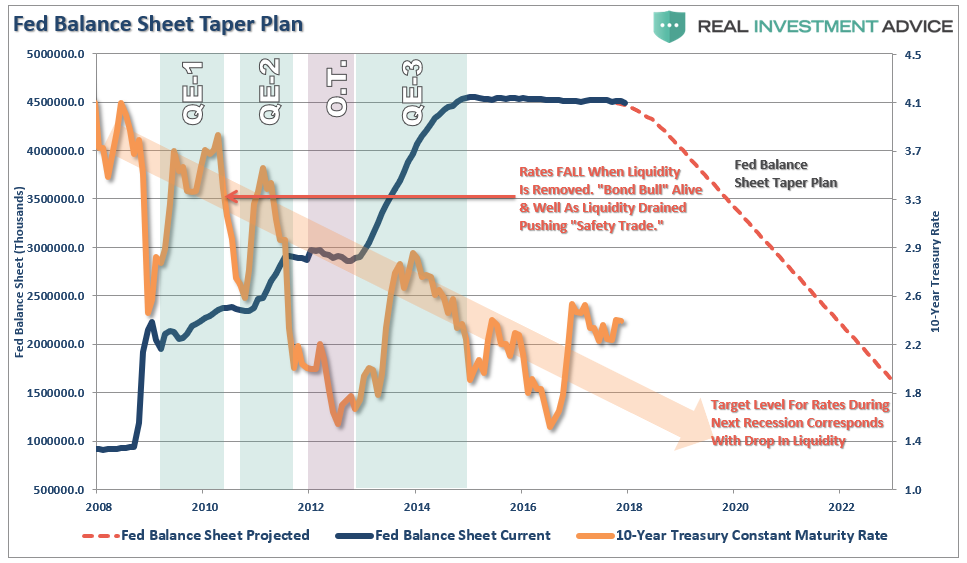

Since 2015, the balance sheet has been fairly stagnant as the Fed continues to “reinvest” proceeds to maintain the size of the balance sheet at current levels. However, as Wolf correctly notes, the Fed is set to embark upon a serious balance sheet “reduction” program over the next couple of years.

Wolf is also right in the fact this is a potential “game changer” for the bond market. Just not in the manner that most expect. The following chart shows the path of the Fed’s balance sheet in accordance with their stated goals of reduction. The trend of rates would be expected to follow.

This reduction in the balance sheet is also occurring at a time when the Fed is lifting the short-end of the yield curve which further tightens monetary conditions.

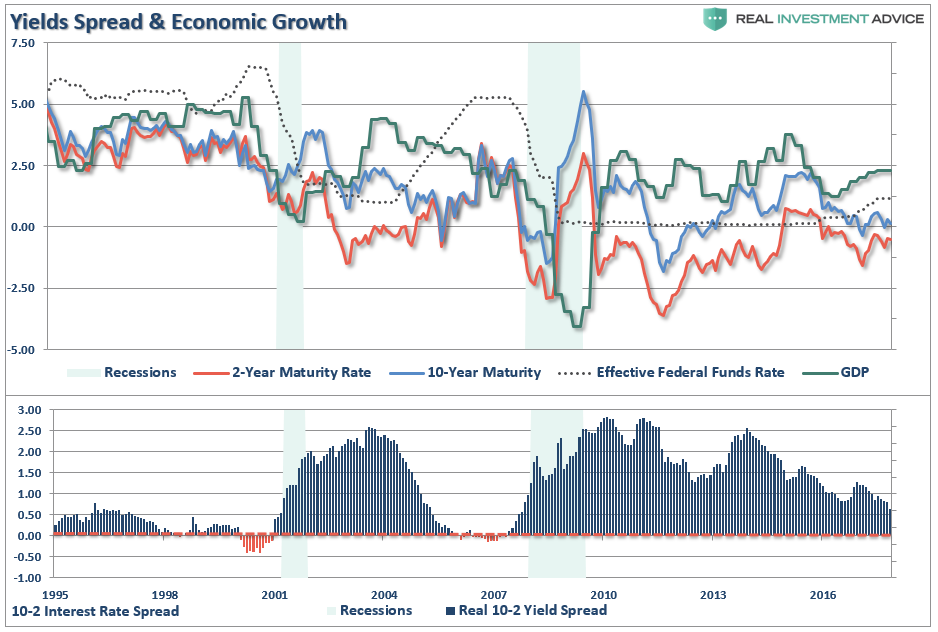

You should notice the longer-term correlation between the yield-spread and the direction of economic growth. Economic growth over the last couple of quarters has indeed diverged from the yield spread. This was due to 2-major fires and 3-devastating Hurricanes which provided a temporary boost to growth, but those supports are only temporary in nature.

If correlations hold, and there is no reason they shouldn’t, as the Fed extracts liquidity from the financial markets by raising short-term rates and reducing their balance sheet, the most likely path for rates will be lower for several reasons.

- Raising the cost of borrowing on individuals and businesses reduces demand for credit. In an economy 70% driven by consumption, and a big chunk of that consumption supported by debt, the negative impact will likely occur faster than many expect.

- The economic boosts provided by natural disasters is short-term in nature. The next several quarters will likely witness a cyclical downturn as the consumption slows.

- Yields in the U.S. are substantially higher than those in many other countries. As stated previously, all rates are relative and money flows to the highest yield.

Of course, this is all subject to the Fed actually reducing their balance sheet. As of the end of 2018, there is little evidence they are doing so and the $15 billion injection of liquidity at the end of the year has helped push asset prices to record levels.

But since these injections are “emergency measures” in order to offset economic / market weakness which might impair the “wealth effect,” the question is exactly what “emergency” are we fighting?

It’s a rhetorical question, but is important to the discussion.

The rise and fall of stock prices have very little to do with the average American and their participation in the domestic economy. Interest rates are an entirely different matter. The issue of rising borrowing costs spreads through the entire financial ecosystem like a virus.

Since interest rates affect “payments,” increases in rates quickly have negative impacts on consumption, housing, and investment which ultimately deters economic growth.

Given the current demographics, debt, pension and valuation headwinds, the future rates of growth are going to be low over the next couple of decades. Even the Fed’s own “long run” economic growth rates currently run below 2%. All of this suggests that rates will continue to low, relative to previous history, as the catalysts to “support” higher interest rates simply doesn’t exist currently.

As my friend, Cullen Roche, recently penned:

“My general view remains somewhat unchanged – I think interest rates are in a structural period of low rates (see here for my 5 big structural reasons for low rates and low growth) with a very low likelihood of higher inflation in the coming decade. The short-term is a bit more cautious on the long end of the curve, but still not nearly as risky as bond permabears would have us believe. The permabearish narratives, which are based largely on bond market myths and misunderstandings, have kept an unfortunate number of investors from being involved in what continues to be a tremendously beneficial and profitable asset class. As stocks and other asset classes rise in value, I think bonds, despite low rates, are becoming an even MORE important diversifying asset class despite their low(ish) returns going forward.”

Disclosure: The information contained in this article should not be construed as financial or investment advice on any subject matter. Streettalk Advisors, LLC expressly disclaims all liability in ...

more