Bull Markets Actually Do Die Of “Old Age”

David Ranson recently endeavored in a long research report to simply declare that “bull markets do not die of old age.”

“The life expectancy of bull markets can be inferred from history. Fourteen bull markets in U.S. stocks have come and gone since 1927, and their mean lifetime is 55 months. But this calculation can be taken further. From the age of one year to the age of eight years, there’s no overall tendency for life expectancy to decline as a market advance gets older. The present stock market advance, which began 105 months ago, is no more likely to end within the next twelve months than it was when it was only twelve months old. Bull markets do not die of old age.”

Think about this for a moment.

This is the equivalent of suggesting that since the average male dies at 88-years of age if he lives to be 100, he has no more chance of dying in the next 12-months than he did when he was 40-years old.

While a 100-year old male will likely expire within a relatively short time frame, it will not just “being old” that leads to death. It is the onset of some outside influence such as pneumonia, infection, organ failure, etc. that leads to the eventual death as the body is simply to weak to defend itself. While we attribute the death to “old age,” it was not just “old age” that killed the host.

This was a point that my friend David Rosenberg made in 2015 before the first rate hike:

“Equity bull markets never die simply of old age. They die of excessive Fed monetary restraint.”

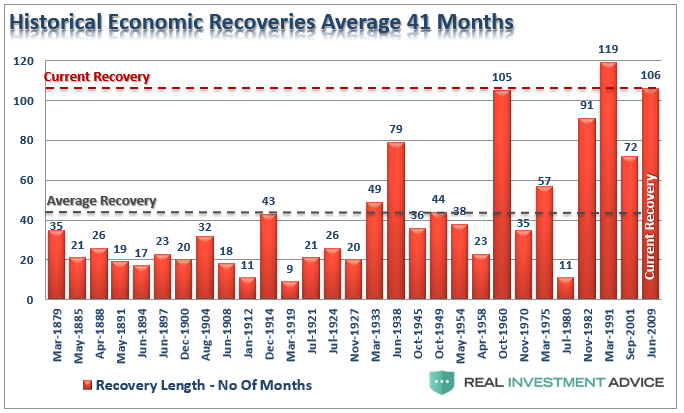

First, averages and medians are great for general analysis but obfuscate the variables of individual cycles. To be sure the last three business cycles (80’s, 90’s and 2000) were extremely long and supported by a massive shift in a financial engineering and credit leveraging cycle. The post-Depression recovery and WWII drove the long economic expansion in the 40’s, and the “space race” supported the 60’s.

(Click on image to enlarge)

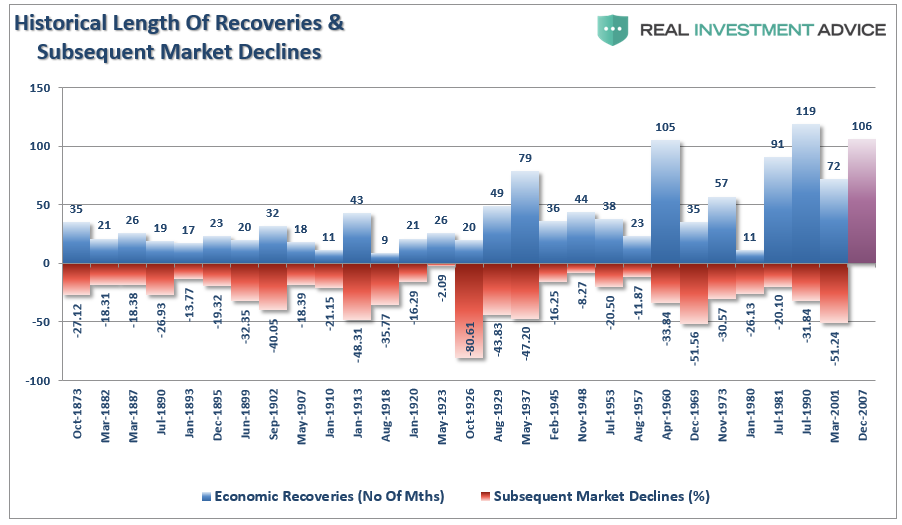

But each of those economic expansions did indeed come to an end. The table below shows each expansion with the subsequent decline in markets.

(Click on image to enlarge)

Think about it this way.

- At 104 months of economic expansion in 1960, no one assumed the expansion would end at 105 months.

- At 118 months no one assumed the end of the “dot.com mania” was coming in the next month.

- In December of 2007, no one believed the worst recession since the “Great Depression” had already begun.

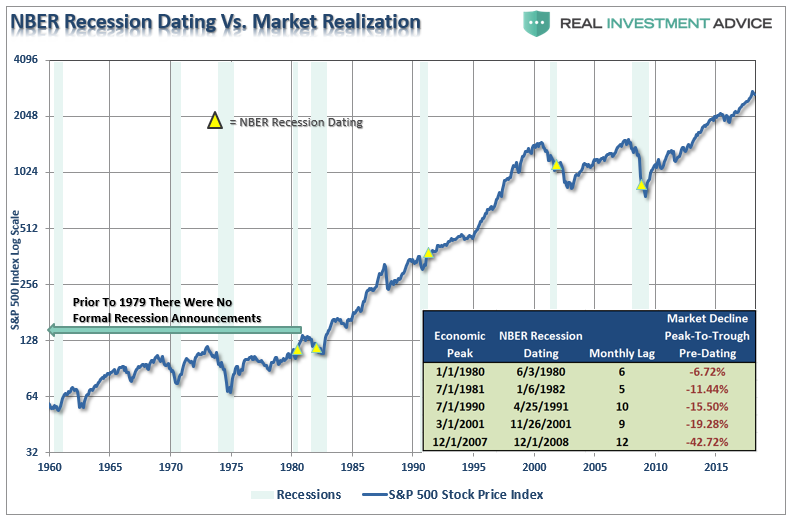

The problem for investors, and the suggestion that “bull markets don’t die of old-age,” is that economic data is always negatively revised in arrears. The chart below shows the recession pronouncements by the National Bureau Of Economic Research (NBER) and when they actually began.

(Click on image to enlarge)

The point here is simple, by the time the economic data is revised to reveal a recession, it will be far too late to do anything about it from an investment perspective. However, the financial market has tended to “sniff” out trouble

The Infections That Kill Old Bull Markets

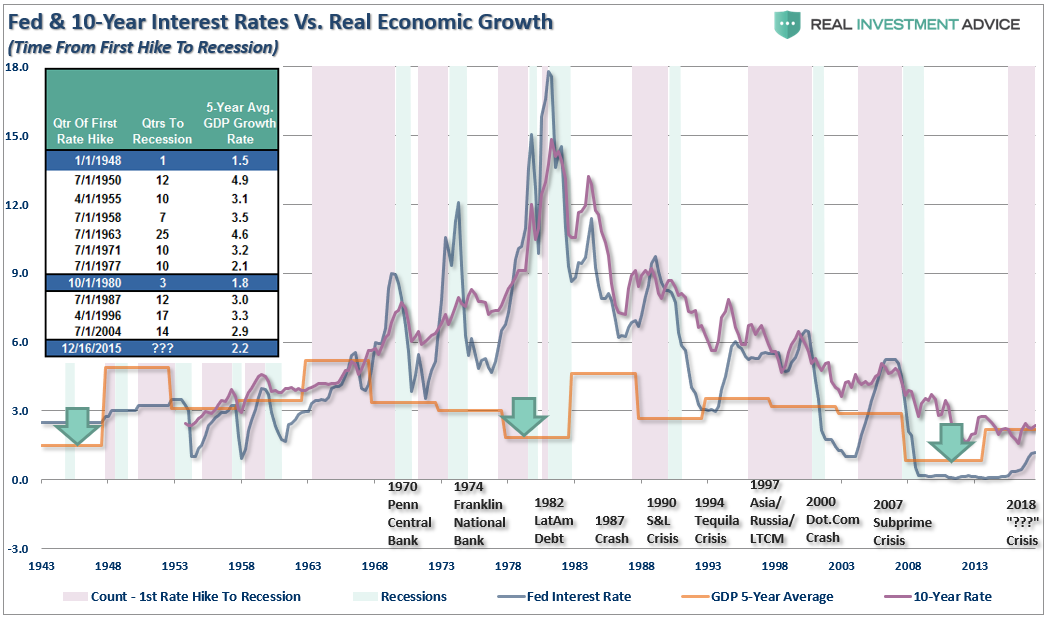

Infection #1: Interest Rates

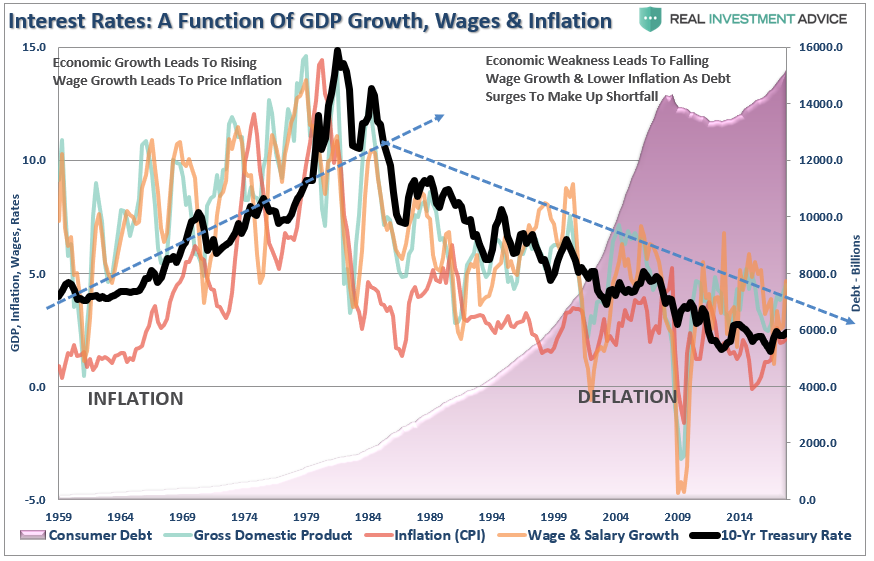

As noted by David Rosenberg, with the Fed continuing to hike rates in the U.S., tightening monetary conditions, the previous 3-year time horizon is now substantially shorter. More importantly, the “average” time frame between an initial rate hike and recession was based on economic growth rates which were substantially higher than they are currently.

(Click on image to enlarge)

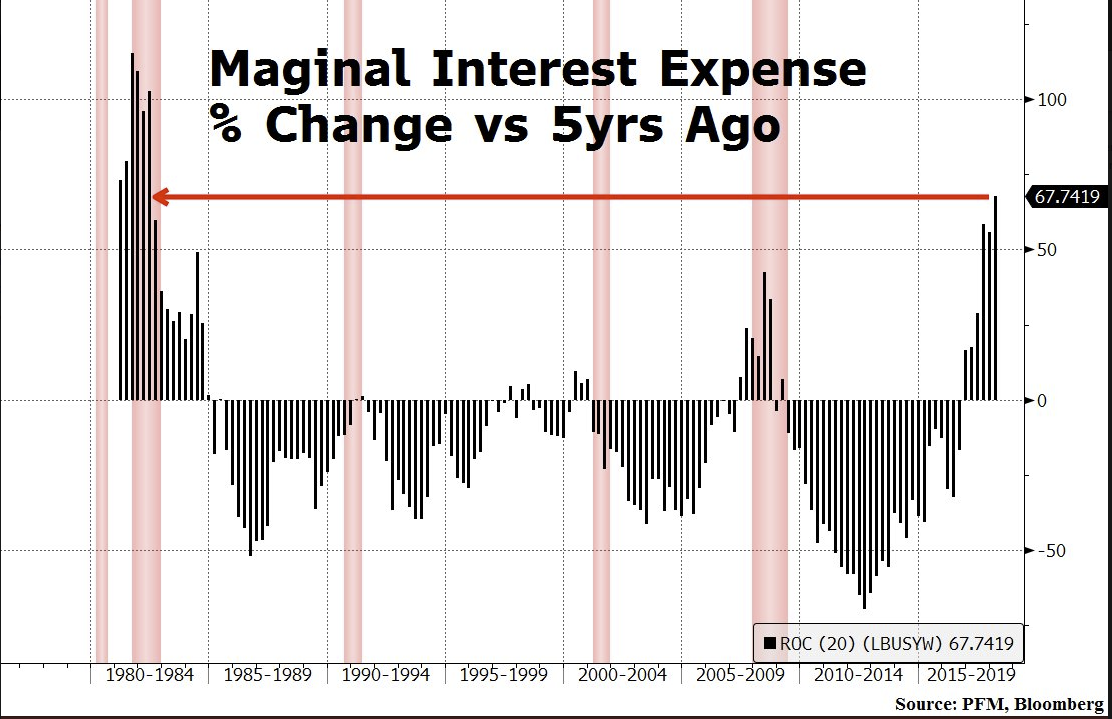

Furthermore, as interest rates rise, so does the cost of capital. In a heavily leveraged economy, the change in interest expense has been a good predictor of economic weakness. As recently noted by Donald Swain, CFA:

“What if marginal interest expense pressures are the true recession signal (cause of economic weakness) and the yield curve is just a correlated input to that process? If so, for the first time, the Fed is hiking into what is already the most hostile refit period in 35-years.”

(Click on image to enlarge)

The point is that in the short-term the economy and the markets (due to momentum) can SEEM TO DEFY the laws of gravity as interest rates begin to rise. However, as rates continue to rise they ultimately act as a “brake” on economic activity. Think about the all of the areas that are NEGATIVELY impacted by rising interest rates:

- Debt servicing requirements reduce future productive investment.

- The housing market. People buy payments, not houses, and rising rates mean higher payments.

- Higher borrowing costs which lead to lower profit margins for corporations.

- Stocks are cheap based on low-interest rates. When rates rise, markets become overvalued very quickly.

- The economic recovery to date has been based on suppressing interest rates to spur growth.

- Variable rate interest payments for consumers

- Corporate share buyback plans, a major driver of asset prices, and dividend issuances have been done through the use of cheap debt.

- Corporate capital expenditures are dependent on borrowing costs.

Infection #2: Spiking Input Costs

When rate hikes are combined with a surge in oil prices, which is a double whammy to consumers, there has been a negative outcome as noted by Peter Cook, CFA last week.

“A better record of predicting recessions is achieved when Fed has hiked rates by 2.00%-2.50%, AND oil prices have at least doubled. The price of money and energy are major financial inputs to financial planning, so when they simultaneously rise sharply, consumers and businesses are forced to retrench. Based on the Fed’s well-communicated strategy, it plans to raise rates another 0.75% during 2018 on top of the previous 1.50% over the past few years. If crude oil stays above $50-60, both conditions for a recession would be met in the second half of 2018.

Yet neither the Fed, or any high-profile economist, is predicting the beginning of a recession during 2019, let alone 2018. Answering the inflation/deflation question correctly is the most important issue of the day for investment portfolios. If recession/deflation arrives before growth/inflation, a major adjustment in expectations, and capital market prices, is coming within the next year.”

This shouldn’t be surprising.

In the past, when Americans wanted to expand their consumption beyond the constraint of incomes they turned to credit in order to leverage their consumptive purchasing power. Steadily declining interest rates, and lax lending standards, put excess credit in the hands of every American. Such is why, during the 80’s and 90’s, as the ease of credit permeated its way through the system, the standard of living seemingly rose in America even while economic growth slowed along with incomes.

(Click on image to enlarge)

As I recently discussed with Shawn Langlois at MarketWatch:

“With a deficit between the current standard of living and what incomes, savings and debt increases can support, expectations of sustained rates of stronger economic growth, beyond population growth, becomes problematic.

For investors, that poses huge risks in the market.

While accounting gimmicks, wage suppression, tax cuts and stock buybacks may support prices in the short-term, in the long-term the market is a reflection of the strength of the economy. Since the economy is 70% driven by consumption, consumer indebtedness could become problematic.”

Infection #3 – Valuations

Lastly, it isn’t an economic recession that is truly problematic for investors.

If asset prices rose equally with increases in earnings, in other words the price-to-earnings ratio remained flat, then theoretically “bull markets” would last forever.

Unfortunately, since asset prices are a reflection of investor psychology, or “greed,” it is not surprising that economic recessions reveal the mispricing between the premium investors pay for a stream of earnings versus what they are really worth. As I noted just recently:

“Bull markets are born on pessimism, grow on skepticism, and die on euphoria.” -Sir John Templeton

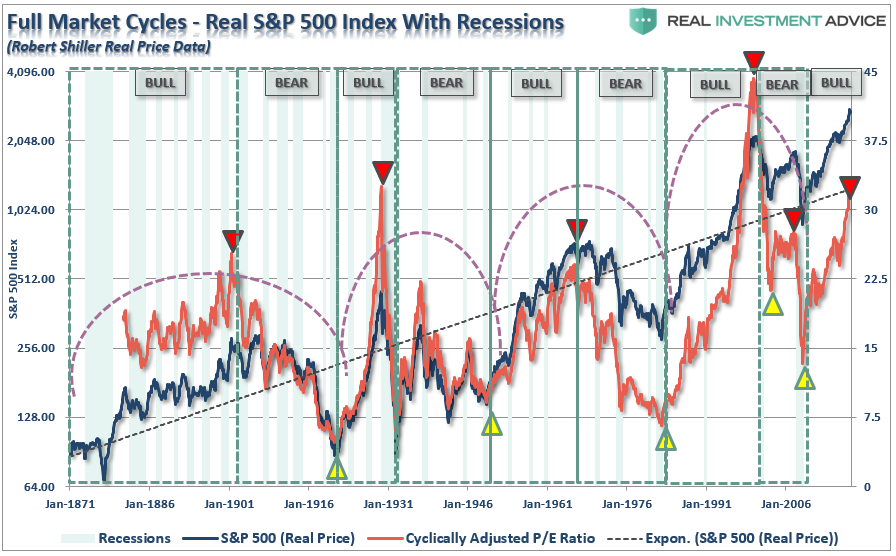

Take a look at the chart below which is Robert Shiller’s monthly data back to 1871. The “yellow” triangles show periods of extreme undervaluation while the “red” triangles denote periods of excess valuation.

(Click on image to enlarge)

Not surprisingly, 1901, 1929, 1965, 1999, and 2007 were periods of extreme “euphoria” where “this time is different” was a commonly uttered phrase.

Conclusion

What the majority of mainstream analysis fails to address is the “full-cycle” of markets. While it may appear that “bull markets do not die of old age,” in reality, it is “old age that leaves the bull defenseless against infections.”

It is the impact of an exogenous event on an over-leveraged, extended and over-valued market that eventually leads to its death. Ignoring the “infections,” and opting for “hope,” has always led to emotionally driven mistakes which account for 50% of investor’s under-performance over a 20-year cycle.

With expectations rising the Fed will further tighten monetary policy, the vulnerabilities of an “aged bull market” will be an issue for investors in the future.

Disclosure: The information contained in this article should not be construed as financial or investment advice on any subject matter. Real Investment Advice is expressly disclaims all liability in ...

more