Bond Bears & Why Rates Won’t Rise

Here we go again…

Since June of 2013, I have been writing about the reasons why rates can’t rise much and why calls for the end of the “bond bull market” remain wrong.

Regardless, about every 3-months or so, there is a tick up in rates and you can almost bet that soon thereafter will be a litany of articles explaining why THIS time the “bond bull market” is really dead. For example, just from this past week:

What is the argument from low rates will rise?

It basically boils down to simply this – rates are so low they MUST go up.

The problem, however, is that interest rates are vastly different than equities. When people go to make a purchase on credit, borrow money for a house, or get a loan for a new car, they don’t ask what the level of the stock market is but rather “how much will this cost me?” The differentiator between making a purchase, or not, is based on the simple outcome of the interest rate effect on the loan payment. If interest rates rise too much, consumption stalls, and along with it economic growth, causing rates to go lower. If economic demand is robust, rates rise to meet the demand for credit.

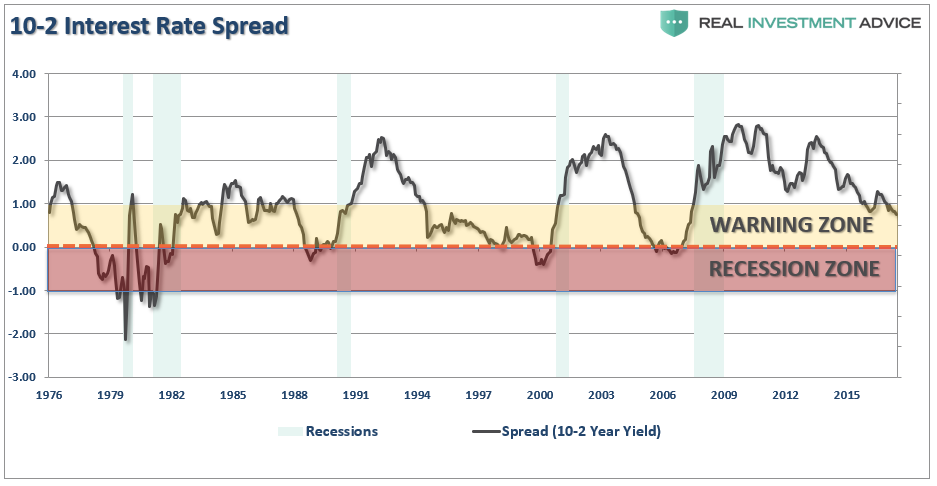

The trend and level of interests are the singular best indicator of economic activity. As Doug Kass recently noted:

“The spread between the two- and ten-year U.S. notes has fallen to 68 basis points — that’s the lowest print in ten years and if history is a guide it is signaling a potential domestic economic slowdown.”

“The flattening in the yield curve is happening despite a likely continued Federal Reserve tightening and a rise back to December levels for overnight index swaps (OIS). It was back in 2004 — as the Fed started its tightening cycle (that concluded in Summer, 2006) — that both the curve flattened and the five year OIS rose. At the conclusion of the tightening in the middle of 2006, a deep recession followed by about fifteen to eighteen months later.”

In other words, “It’s the economy, stupid.”

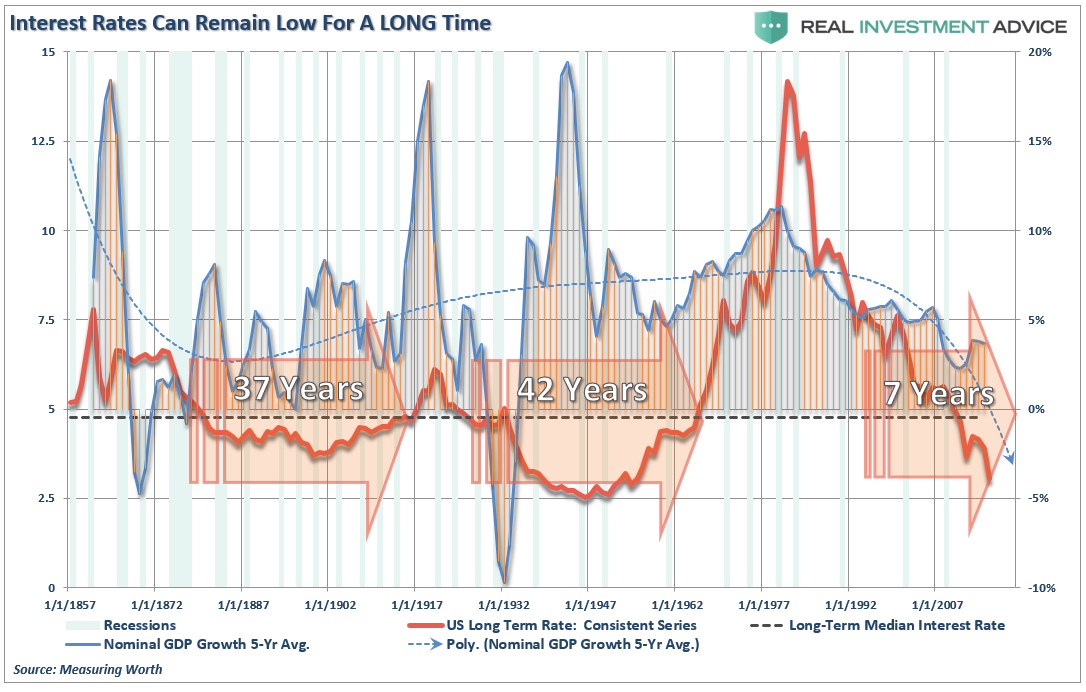

Economic Growth Drives Rates

The chart below is a history of long-term interest rates going back to 1857. The dashed black line is the median interest rate during the entire period. I have compared it to the 5-year nominal GDP growth rate during the same period.

(Note: As shown, interest rates can remain low for a VERY long time.)

Interest rates are a function of strong, organic, economic growth that leads to a rising demand for capital over time. There have been two previous periods in history that have had the necessary ingredients to support rising interest rates. The first was during the turn of the previous century as the country became more accessible via railroads and automobiles, production ramped up for World War I and America began the shift from an agricultural to industrial economy.

The second period occurred post-World War II as America became the “last man standing” as France, England, Russia, Germany, Poland, Japan and others were left devastated. It was here that America found its strongest run of economic growth in its history as the “boys of war” returned home to start rebuilding the countries that they had just destroyed. But that was just the start of it.

Beginning in the late 50’s, America embarked upon its greatest quest in history as man took his first steps into space. The space race that lasted nearly twenty years led to leaps in innovation and technology that paved the wave for the future of America. Combined with the industrial and manufacturing backdrop, America experienced high levels of economic growth and increased savings rates which fostered the required backdrop for higher interest rates.

Currently, the U.S. is no longer the manufacturing powerhouse it once was and globalization has sent jobs to the cheapest sources of labor. Technological advances continue to reduce the need for human labor and suppress wages as productivity increases. Today, the number of workers between the ages of 16 and 54 is at the lowest level relative to that age group since the late 70’s. This is a structural and demographic problem that continues to drag on economic growth as nearly 1/4th of the American population is now dependent on some form of governmental assistance.

This structural employment problem remains the primary driver as to why “everybody” is still wrong in expecting rates to rise.

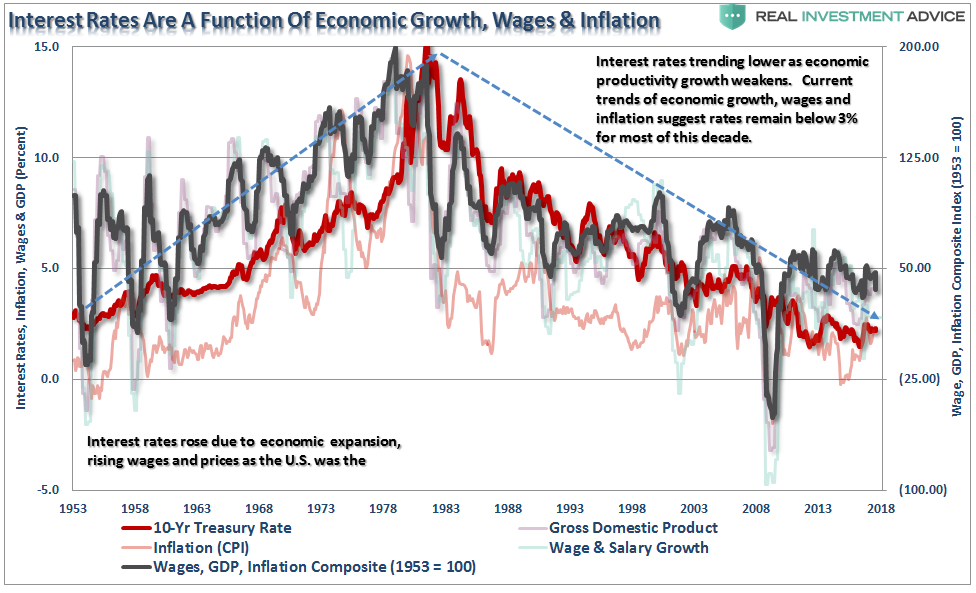

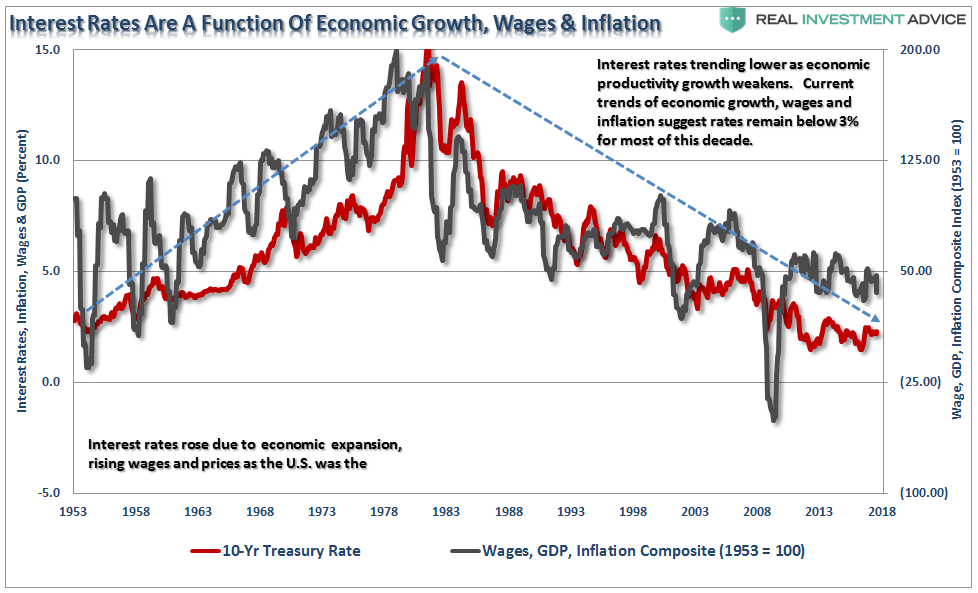

As you can see there is a very high correlation, not surprisingly, between the three major components (inflation, economic and wage growth) and the level of interest rates. Interest rates are not just a function of the investment market, but rather the level of “demand” for capital in the economy. When the economy is expanding organically, the demand for capital rises as businesses expand production to meet rising demand. Increased production leads to higher wages which in turn fosters more aggregate demand. As consumption increases so does the ability for producers to charge higher prices (inflation) and for lenders to increase borrowing costs. (Currently, we do not have the type of inflation that leads to stronger economic growth, just inflation in the costs of living that saps consumer spending – Rent, Insurance, Health Care)

The chart above is a bit busy, but I wanted you to see the trends in the individual subcomponents of the composite index. The chart below shows only the composite index and the 10-year Treasury rate. Not surprisingly, the recent decline in the composite index also coincides with a decline in interest rates.

In the current economic environment, the need for capital remains low, outside of what is needed to absorb incremental demand increases caused by population growth, as demand remains weak. While employment has increased since the recessionary lows, much of that increase has been the absorption of increased population levels.

Many of those jobs remain centered in lower wage paying and temporary jobs which do not foster higher levels of consumption. To offset weaker organic consumption, artificially suppressed interest rates, though monetary policy, gives the appearance of economic growth by dragging forward future consumption which leaves a future “void” that has to be continually refilled.

Currently, there are few economic tailwinds prevalent that could sustain a move higher in interest rates. The reason is that higher interest reduces the flow of capital within the economy. For an economy that remains dependent on the generosity of Central Bankers, rising rates are not the outcome that “stock market bulls” should NOT be rooting for.

The Implications Of A Bond Bust

If there is indeed a bond bubble, a burst would mean bonds decline rapidly in price pushing interest rates markedly higher. This is the worst thing that could possibly happen.

1) The Federal Reserve has been buying bonds for the last 9- years in an attempt to push interest rates lower to support the economy. The recovery in economic growth is still dependent on massive levels of domestic and global interventions. Sharply rising rates will immediately curtail that growth as rising borrowing costs slows consumption.

2) The Federal Reserve currently runs the world’s largest hedge fund with over $4 Trillion in assets. Long Term Capital Mgmt. which managed only $100 billion at the time nearly brought the economy to its knees when rising interest rates caused it to collapse. The Fed is 45x that size.

3) Rising interest rates will immediately kill the housing market, not to mention the loss of the mortgage interest deduction if the GOP tax bill passes, taking that small contribution to the economy away. People buy payments, not houses, and rising rates mean higher payments.

4) An increase in interest rates means higher borrowing costs which lead to lower profit margins for corporations. This will negatively impact the stock market given that a bulk of the “share buybacks” have been completed through the issuance of debt.

5) One of the main arguments of stock bulls over the last 9-years has been the stocks are cheap based on low interest rates. When rates rise the market becomes overvalued very quickly.

6) The massive derivatives market will be negatively impacted leading to another potential credit crisis as interest rate spread derivatives go bust.

7) As rates increase so does the variable rate interest payments on credit cards. With the consumer are being impacted by stagnant wages, higher credit card payments will lead to a rapid contraction in income and rising defaults. (Which are already happening as we speak)

8) Rising defaults on debt service will negatively impact banks which are still not adequately capitalized and still burdened by large levels of bad debts.

9) Commodities, which are very sensitive to the direction and strength of the global economy, will plunge in price as recession sets in.

10) The deficit/GDP ratio will begin to soar as borrowing costs rise sharply. The many forecasts for lower future deficits will crumble as new forecasts begin to propel higher.

I could go on but you get the idea.

The problem with most of the forecasts for the end of the bond bubble is the assumption that we are only talking about the isolated case of a shifting of asset classes between stocks and bonds. However, the issue of rising borrowing costs spreads through the entire financial ecosystem like a virus. The rise and fall of stock prices have very little to do with the average American and their participation in the domestic economy. Interest rates, however, are an entirely different matter.

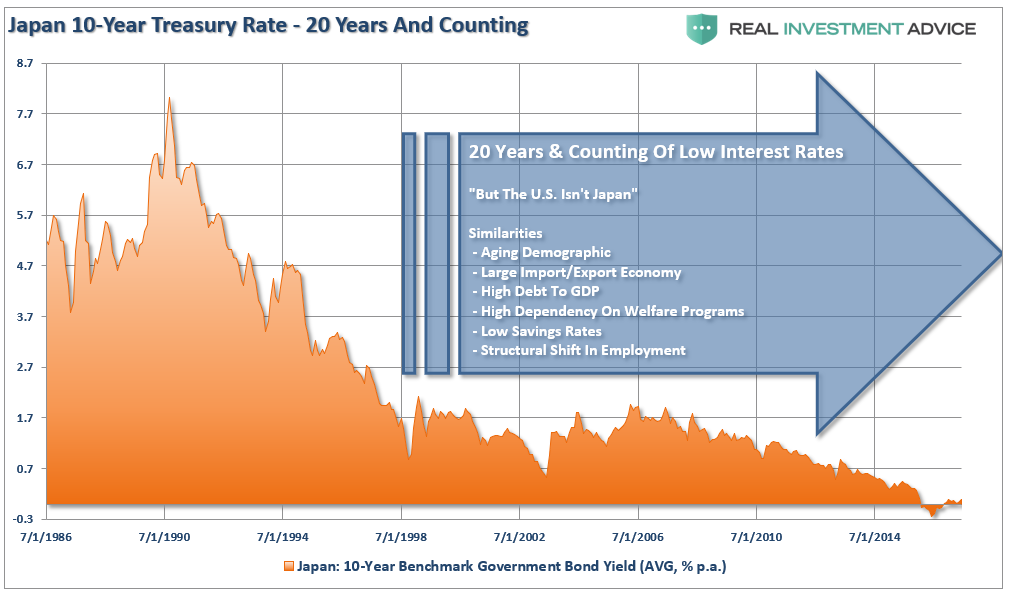

I won’t argue there is much room left for interest rates to fall in the current environment, there is also not a tremendous amount of room for increases. Since interest rates affect “payments,” increases in rates quickly have negative impacts on consumption, housing, and investment. This idea suggests is that there is one other possibility that the majority of analysts and economists ignore which I call the “Japan Syndrome.”

Japan is has been fighting many of the same issues for the past two decades. The “Japan Syndrome” suggests that while interest rates are near lows it is more likely a reflection of the real levels of economic growth, inflation, and wages.

If that is true, then rates are most likely “fairly valued” which implies that the U.S. could remain trapped within the current trading range for years as the economy continues to “muddle” along.

The irrationality of market participants, combined with globally accommodative central bankers, continue to push asset values higher and concentrate investors into the ongoing “chase for yield.” There isn’t much guessing on how this will end, history tells us that such things rarely end well.

Disclosure: The information contained in this article should not be construed as financial or investment advice on any subject matter. Streettalk Advisors, LLC expressly disclaims all liability in ...

more