Analyst’s Estimates Go Parabolic – Is The Market Next?

At the end of February, I discussed the impact of the tax cut and reform legislation as it related to corporate profits.

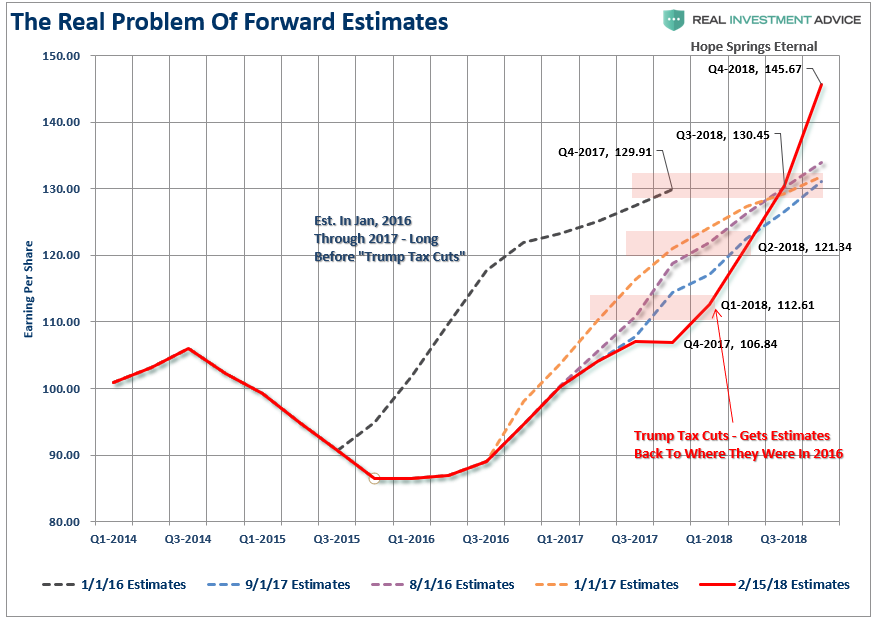

“In October of 2017, the estimates for REPORTED earnings for Q4, 2017 and Q1, 2018 were $116.50 and $119.76. As of February 15th, the numbers are $106.84 and $112.61 or a difference of -$9.66 and -7.15 respectively.

First, while asset prices have surged to record highs, reported earnings estimates through Q3-2018 have already been ratcheted back to a level only slightly above where 2017 was expected to end in 2016. As shown by the red horizontal bars – estimates through Q3 are at the same level they were in January 2017. (Of course, “hope springs eternal that Q4 of this year will see one of the sharpest ramps in earnings in S&P history.)”

That was so yesterday.

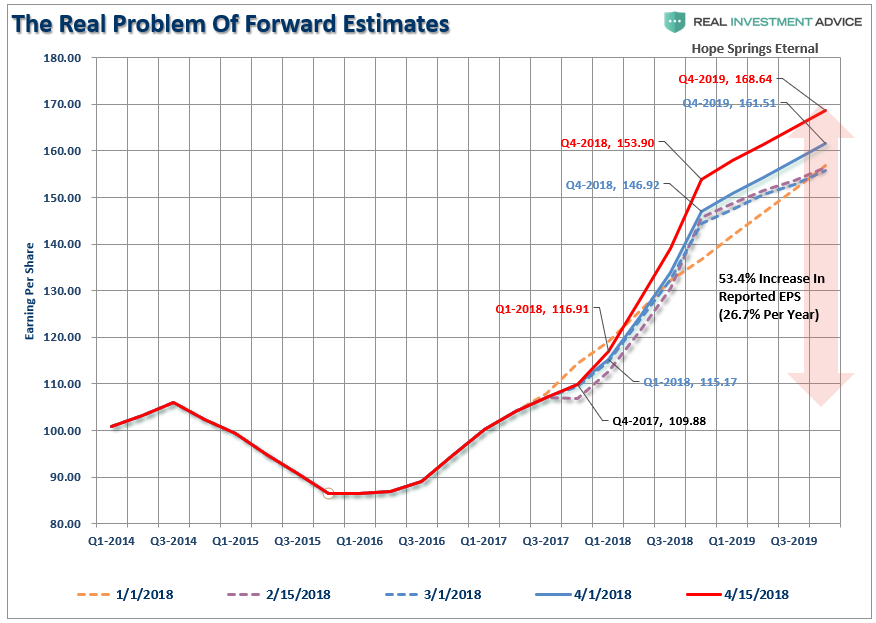

Despite a recent surge in market volatility, combined with the drop in equity prices, analysts have “sharpened their pencils” and ratcheted UP their estimates for the end of 2018 and 2019. Earnings are NOW expected to grow at 26.7% annually over the next two years.

The chart below shows the changes a bit more clearly. It compares where estimates were on January 1st versus March and April. “Optimism” is, well, “exceedingly optimistic” for the end of 2019.

The surge in earnings estimates gives cover for Wall Street analysts to predict surging asset prices. Buy now before you miss out!

“While earnings season has only just gotten started (only 10% of the S&P 500 companies have reported so far), a whopping 84.6% have beaten their earnings estimates, and 78.8% have beaten their revenue estimates. Those are impressive stats. And this earnings season looks like it could be even better than the lofty expectations going into it. This sets the market up for all-time highs just ahead.”

Sure, that could well be the case as a momentum-driven market is a very tough thing to kill. Despite the recent “hiccup” over the last month or so, the market remains above it’s 200-day moving average and there are few signs of investor panic currently.

However, there are two major concerns with the current trajectory of earnings estimates.

The first is that Wall Street has historically over-estimated earnings by about 33% on average.

Yes, 84% of companies have beaten estimates so far, which is literally ALWAYS the case, because analysts are never held to their original estimates. If they were, 100% of companies would be missing estimates currently.

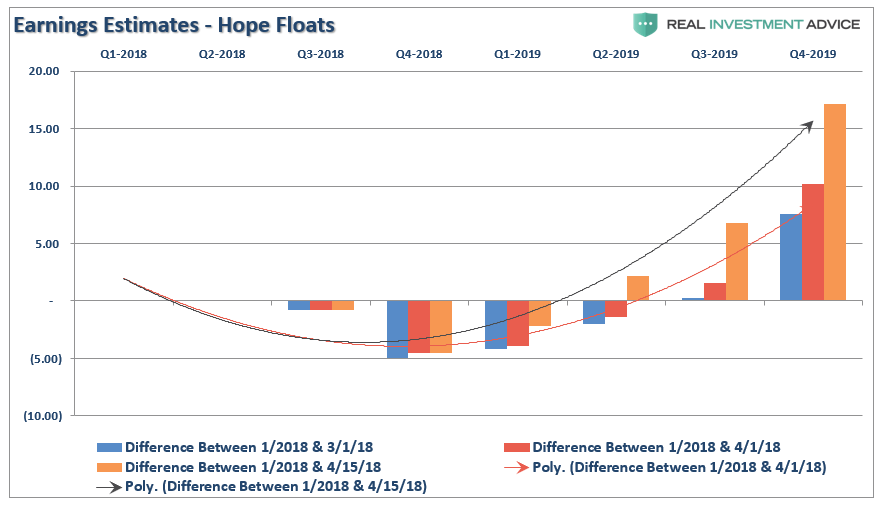

At the beginning of January, analysts overestimated earnings by more than $6/share, reported, versus where they are currently. It’s not surprising volatility has picked up as markets try to reconcile valuations to actual earnings.

Furthermore, the overestimation provides a significant amount of headroom for Wall Street to be disappointed in future, particularly once you factor in the impacts of higher interest rates and slower economic growth.

But economic growth is set to explode. Right?

Most likely not.

As I discussed last week, the short-term boost to economic growth in the U.S., driven by a wave of natural disasters, is now beginning to fade. However, the same is seen on a global scale as well. To wit:

“The international slowdown is becoming increasingly obvious from the widely followed economic indicators. The most popular U.S. measures seem to present more of a mixed bag. Yet, as we pointed out late last year, the bond market, following the U.S. Short Leading Index, started sniffing out the U.S. slowdown months ago.”

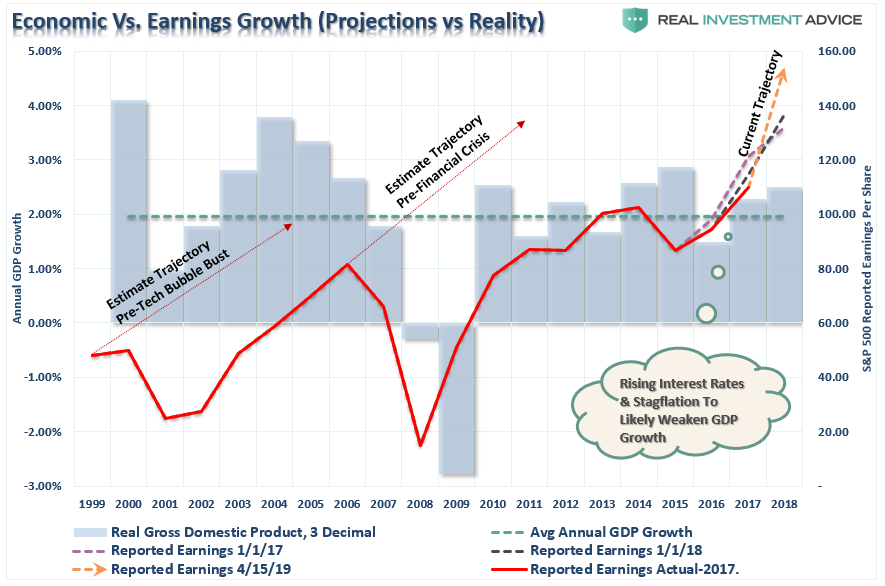

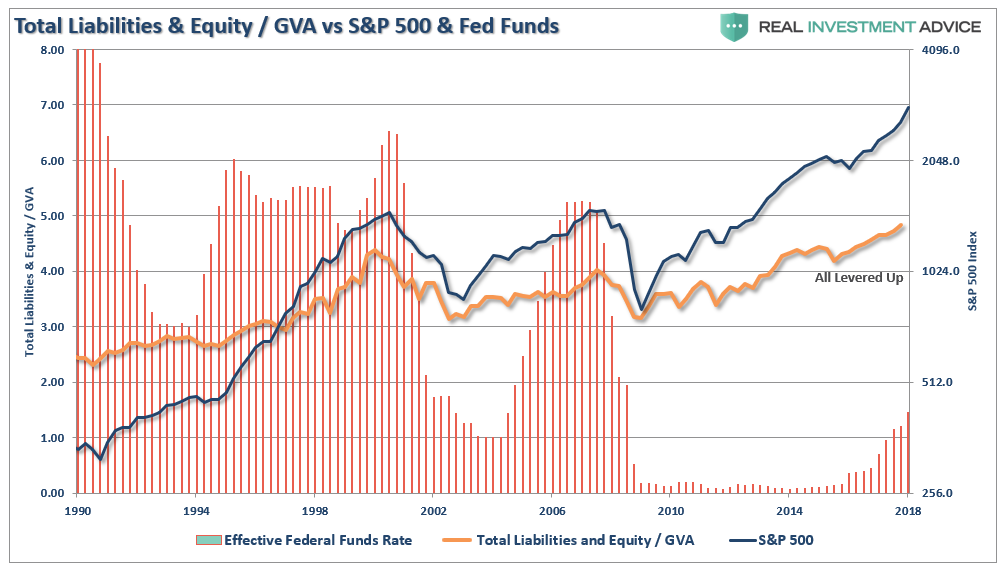

Furthermore, the economy is sensitive to changes in interest rates. This is particularly the case when the consumer, which comprises about 70% of the GDP calculation, is already heavily leveraged. Furthermore, with corporations more highly levered than at any other point n history, and dependent on bond issuance for dividend payments and share buybacks, higher interest rates will quickly stem that source of liquidity. Notice that each previous peak was lower.

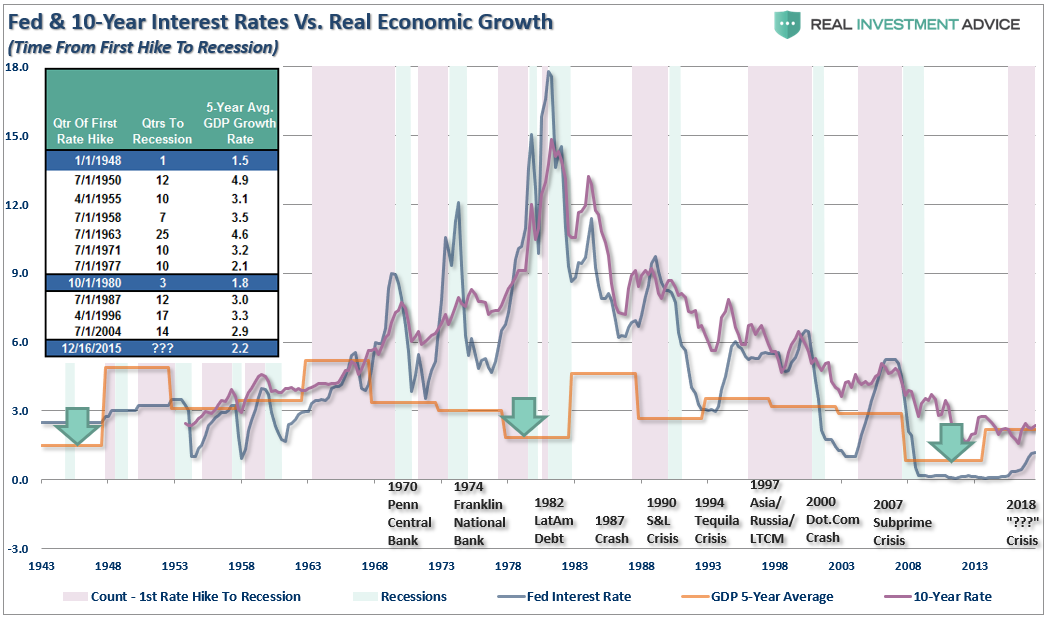

With economic growth running at lower levels of annualized growth rates, the “bang point” for the Fed’s rate hiking campaign is likely substantially lower as well. History suggests this will likely be the case. At every point in history where the Fed has embarked upon a rate hiking campaign since 1980, the “crisis point” has come at steadily lower levels.

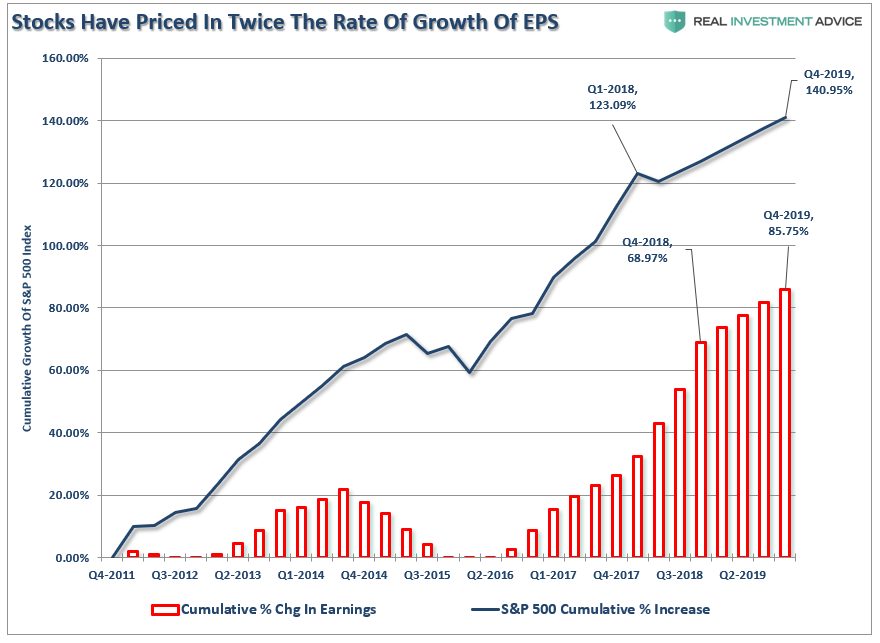

But even if we give Wall Street the benefit of the doubt, and assume their predictions will be correct for the first time in human history, stock prices have already priced in twice the rate of EPS growth.

There are few if any, Wall Street analysts expecting a recession at any point in the future. Unfortunately, it is just a function of time until a recession occurs and earnings fall in tandem.

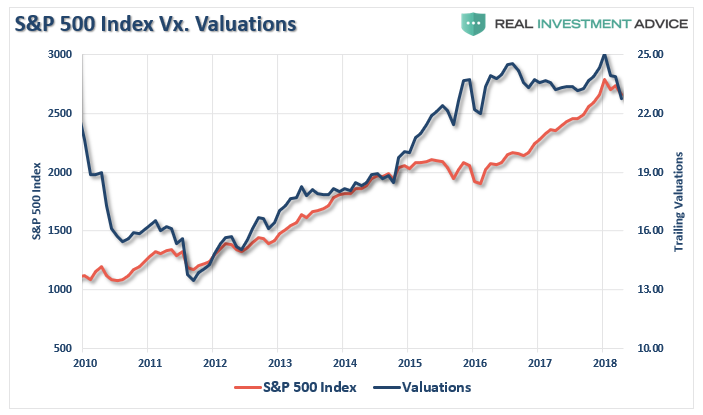

More importantly, the expectation for a profits-driven surge in asset prices fails to conflate with the reality that valuations have been the most important driver of higher stock prices throughout history. Currently, despite surging earnings expectations, market participants are already revaluing equity and high-yield investments.

In our opinion, the biggest mistake that Wall Street is potentially making in their estimates is the differential between “statutory” and “effective” rates. As we addressed previously:

“From 1947 to 1986 the statutory corporate tax rate was 49% and the effective tax rate averaged 36.4% for a difference of 12.6%. From 1987 to present, after the statutory tax rate was reduced to 39%, the effective rate has averaged 28.1%, 10.9% lower than the statutory rate.

In reality, a company that earned $5.00 pretax only paid $1.41 in taxes in 2017 on average, leaving an after-tax profit of $3.59, and not $3.25. Under the new tax law that after-tax profit would come in at the $3.95 as stated in the article and the gain would be 10%, or half, of the gain Wall Street expects.”

There is virtually no “bullish” argument that will currently withstand real scrutiny.

- Yields are rising which deflates equity risk premium analysis,

- Valuations are not cheap,

- The Fed is extracting liquidity, along with other Central Banks slowing bond purchases, and;

- Further increases in interest rates will only act as a further brake on economic growth.

However, because optimistic analysis supports our underlying psychological “greed”, all real scrutiny to the contrary tends to be dismissed. Unfortunately, it is this “willful blindness” that eventually leads to a dislocation in the markets.

Wall Street is notorious for missing the major turning of the markets and leaving investors scrambling for the exits.

This time will likely be no different.

Will tax reform accrue to the bottom lines of corporations? Most assuredly.

However, the bump in earnings growth will only last for one year. Then corporations will be back to year-over-year comparisons and will once again rely on cost-cutting, wage suppression, and stock buybacks to boost earnings to meet Wall Street’s expectations.

Are stocks ready to go parabolic?

Anything is possible, but the risk of disappointment is extremely high.

Disclosure: The information contained in this article should not be construed as financial or investment advice on any subject matter. Real Investment Advice is expressly disclaims all liability in ...

more