The Myths Of Stocks For The Long Run – Part VI

- Part I – “Buy & Hold” Can Be Hazardous To Your Wealth

- Part II – Why Crashes Matter & The Saving Problem

- Part III – Valuations & Forward Returns

- Part IV – The Math Of Loss

- Part V – Choosing The Right Portfolio Benchmark

Should You Invest Like Warren Buffett?

Whenever we discuss this issue of the fallacies to “buy and hold” investing, invariably there is the comment:

“Then why does Warren Buffett say that the ideal holding period is forever?”

First of all, we have the utmost respect for Warren Buffett. If investing had a “hall of fame,” Warren’s bust would be displayed in the front row along with Benjamin Graham. Through hard work, a grounded set of value principles, and great timing, he has been able to amass a great amount of wealth for himself and his shareholders.

Buffett’s specialty is value investing. That means buying stocks with long-term prospects that are believed (by a value investor) to be undervalued. The unloved underdog, for instance, which has been unfairly cast aside by Wall Street and whose value will be rediscovered in the future.

He articulated this approach succinctly in his 2008 letter to shareholders:

“Long ago, Ben Graham taught me that ‘Price is what you pay; value is what you get.’ Whether we’re talking about socks or stocks, I like buying quality merchandise when it is marked down.”

While there is often a rush in trying to justify “buy and hold” investing by selectively choosing quotes from Warren Buffett as noted above, Mr. Buffett’s most basic premise is that of active asset management:

“Be fearful when others are greedy and greedy when others are fearful.”

Or, as Baron Rothschild once quipped:

“Buy cheap, Sell dear.”

Not only is the most basic tenant of value investing, but it is the most basic premise of investing…period.

Like Buffett, as value-based portfolio managers ourselves, we also prefer extremely long holding periods. However, just because we “prefer” extremely long holding periods, things can and do change which can shorten that holding period immensely.

We also realize there are tremendous differences which we, and other “Buffett” disciples, cannot replicate. Yes, you can buy the same stocks as Buffett, but your outcome is going to be dramatically different from Berkshire Hathaway for several reasons.

There is an old joke that goes:

“The first step in investing like Warren Buffett: start with $1 billion…”

The joke, however, only begins to highlight the incredibly unique position Buffett enjoys in the investing world. Buffett is an anomaly; he is part private-equity deal broker, part investment bank, part Wall Street insider and part activist investor. He is also an investing icon, and as such, many investors copy his actions which lend price support to his investments.

Investors flock to Iowa for his annual shareholder meetings in hopes of glimmering information on how he is able to produce such great returns. Yet, no one has been able to come close to matching his track record. While many think Mr. Buffett has found the secret formula to investing – it is actually a combination of several “special” circumstances which have afforded Mr. Buffett his edge over the years.

Timing Is Everything – we have discussed through this entire series the importance of valuation analysis at the “beginning” of the investing journey. When you start your investing journey is one of the most important facets of long-term investing returns. While Buffett clearly bested the S&P 500 index over the years, he benefited greatly from the luck of catching the greatest bull market run in history in the 80’s and 90’s.

“Timing” and “good luck” are two of the most critical aspects of successful long-term investing. For Buffett, his timing could not have been better as a bulk of his outperformance in the early years came from his nimbleness to capture opportunities as the U.S. emerged from back-to-back recessions, low-valuations, high dividends and falling rates of inflation and interest rates.

As of this writing, those factors no longer exist for investors wishing to replicate his performance going forward. Valuations are elevated, interest rates and inflation are low, and economic growth remains weak. As for Berkshire, the fund has grown to nearly $500 billion and accordingly the opportunities for outsized performance are rarely available in a size which moves the “performance alpha” needle much. As noted by Michelle Perry Higgins

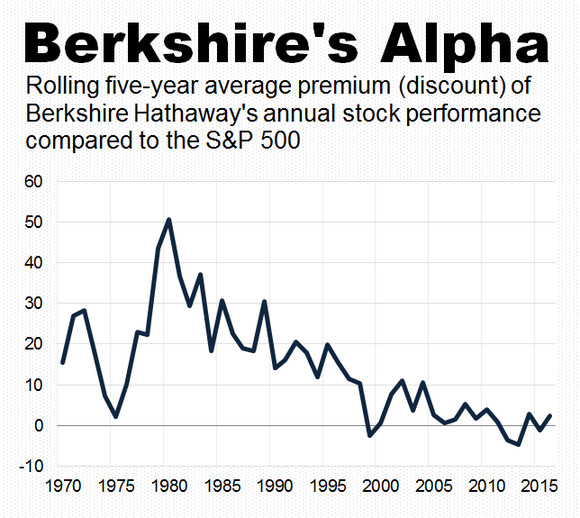

“Buy what I’ve found most insightful is to chart the trend in Berkshire’s annual stock performance compared to the S&P 500. As an example, this is Berkshire’s alpha, for its excess return over the broader market through 2016:”

(Note: Berkshire’s first 5-years were problematic as market valuations were still falling through the 1974 market crash. However, that crash set Buffett up for a spectacular run over the next two decades.)

“This shows that Berkshire’s best days were in the late 1970s, a tumultuous decade thanks to wildly fluctuating energy prices and rapidly accelerating inflation. Since then, Berkshire’s performance relative to the S&P 500 has steadily narrowed. The rolling five-year average of Berkshire’s alpha dipped into negative territory in three out of the past five years.

Working against Berkshire is its growing size, a point Buffett has pointed out in the past. It has the fifth largest market capitalization on the S&P 500, behind only Apple, Alphabet, Microsoft, and Facebook. It also owns a vast assortment of subsidiaries, from home builders to car insurers to restaurants.

The net result is that Berkshire’s annual returns theoretically should, and increasingly are, mirroring that of the economy and thus the broader market. Buffett has said this would happen. He’s obviously right.”

Management Control – As individuals, we can buy shares in a company and hope the company makes good decisions which leads to future rates of increased profitability. Buffett, on the other hand, often takes significant positions in companies which allow him direct input into the decisions the company makes.

“Warren Buffett walks into a board meeting, looks at the guy at the head of the table and says ‘excuse me, you’re sitting in my chair.’” – Wall Street humor.

While humorous, it is also true. We make speculative bets in companies by buying ethereal pieces of paper at one price and hoping to sell them at a higher price later to someone else. In every sense of the word, while we wish to fancy ourselves as investors, we are “speculating” on a future outcome.

Buffett, on the other hand, actually “invests” in companies not only through his influx of capital but also through his ability to provide insight, opportunity, and connections. The seat in the boardroom that Buffett is able to acquire helps pick executives, set the future course for the company, and create opportunities that might not have otherwise existed through synergies with other Buffett related holdings. Their direct hand in management also provides them information not available to most shareholders.

Private investments/Special Opportunities – Unlike the vast majority of portfolio managers and individuals, Mr. Buffett is not limited to just publicly traded stocks and other securities available to the public. Their size and clout gives them access to invest in private situations that many investors have no access to.

A good example was in September 2008. Goldman Sachs (GS) offered Buffett a deal which was too good to be true. With GS trading at $123/share and having capital issues due to market illiquidity, they offered Buffett the right to buy $5 billion of preferred stock yielding 10% and an attached warrant allowing Buffett a five-year option to buy the common stock at $115/share. Five years later, GS was trading at $185/share resulting in a 60% return on the warrants. As if 60% was not enough, it was on top of the 10% dividend they received annually. Needless to say, the average investor was never offered such a deal.

Time horizon – Buffett has no time horizon. In other words, while individuals have a set time frame based on retirement goals and life expectancy, which factor heavily into both the accumulation and distribution phases of the wealth building process, Buffett does not. As discussed previously, capital destruction can wreak havoc on financial goals.

Buffett buys companies. As such, he is focused on the long-term growth potential acquisition. Berkshire Hathaway is also a company, with a board of directors, officers, etc., which also provides the portfolio an “eternal” lifespan. As such, Berkshire can truly act as a long-term investor without concern for market volatility, living requirements, or death. As we have continually mentioned throughout this series, you and I will likely fail to meet our retirement goals if we have to endure a 10-20 year period of no gains. For Berkshire, it will simply be a function of economic growth and the resultant net profitability to investors and shareholders.

Leverage – One of the most interesting aspects and one of Berkshire’s biggest advantages is unique in they own an insurance company. The insurance float represents the available reserve, or the amount of funds available for investment once the insurer has collected premiums, but is not yet obligated to pay out in claims. The money is invested for future claims by the insurer.

Here is where Buffett has a huge advantage over every else as explained by Vintage Value:

“During that time, the insurer invests the money. Insurance float is so valuable that insurance companies often operate at an underwriting loss – that is, the premiums received are not enough to cover the eventual losses (hurricanes, car accidents, etc.) that must be paid and the expenses required to resolve those claims, operate the business, etc.

Why would an insurer operate at a loss? Again, because the insurer can invest the insurance float and make even more money. In this sense, insurance float is like a loan and the underwriting loss is like the interest rate on that loan (i.e. cost of capital).

Now, for most insurers the cost of float is usually a few percentage points. Berkshire Hathaway’s insurance operations, however, are so well run that the company’s historical cost of float has actually been positive… meaning Berkshire Hathaway is actually being paid to take other people’s money!”

The ability to leverage portfolios over time provides a huge amount of potential alpha generation to returns. However, for the average investor, leverage can also be extremely destructive when used improperly.

Don’t Get Swept Up By The Crowd

While we are avid Buffett admirers, with a deep respect for value investing and long-term returns, which is why we model our equity portfolios on value and fundamental factors, we also are well aware of the limitations of our client’s portfolio duration, capital needs, and risk tolerance.

As we addressed in Part 2 of this series, simply buying and holding a basket of stocks over long periods will likely map you fairly closely to the S&P 500 index. (Repeated studies show that more than 30-stocks in a portfolio will essentially replicate the return of the S&P 500 index.) However, historically speaking, while over a given 20 to 30-year investing period an investor will make money, there can be huge shortfalls in meeting investment goals.

As Tom Brakke once stated in an interview:

“No name gets dropped quite as much as Warren Buffett’s by those writing about investments, including me.

The infatuation with Mr. Buffett is understandable given his success and his folksy manner. But investors should be aware that he plays a different game than the rest of us. He gets the first call on deals and he gets attractive terms on his investments. We can’t replicate those advantages.

Another thing to keep in mind is how much Mr. Buffett’s strategy has changed over time. Whereas most investors are urged to adopt a plan and stick to it, Mr. Buffett showed that different times and different circumstances mean that core principles should be examined and adapted as necessary.”

Yes, it is true that Buffett prefers long-holding periods, however, it is a mistake to suggest that he is not an “active” portfolio manager. Buffett has regularly sold parts, or all, of the companies he owns when “value” is no longer present. Furthermore, you should not make the mistake of thinking that anything that Mr. Buffett holds is worth owning currently. As Tom concludes:

“Many investors did that in the ’90s, buying Coca-Cola and other stocks because Buffett owned them, even though they were trading at historic levels of overvaluation. The results weren’t good. So, don’t cherry-pick Mr. Buffett’s ideas and expect to do well. That’s not a great way to emulate him.”

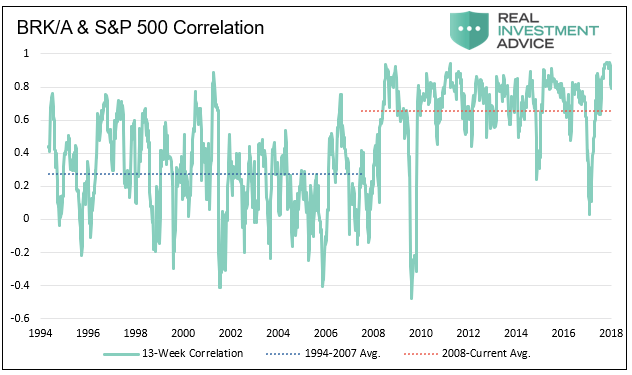

The theme of this series is to avoid these pitfalls as much as possible. Given current valuations the risk/return framework of the market and BRK-A are poor. The graph below highlights this concern. It shows that 90-day rolling correlation of price changes in BRK/A and the S&P 500 are statistically similar. In the market crash of 2008/09 BRK/A’s price was cut in half, similar to the S&P 500. Based on correlations we suspect a similar relationship will hold true for the next big market drawdown.

Be Like Warren

The hardest thing for investors to do is to turn off the media, discount the “buy and hold” mantra, and focus on what matters for long-term investing – valuation. As Tom Brakke concluded:

“The most important lesson that Mr. Buffett can offer anyone: Don’t get swept up by the crowd.

For example, he has been willing to sit on a mountain of cash, even though interest rates are extremely low. Most financial advisers would scoff at that, but Mr. Buffett will wait in cash if there aren’t compelling values available elsewhere.

And he is willing to be out of step for long periods in order to do well in the end. Most of us have a very hard time doing that.”

The patience required to withstand a low return on the cash while the market moves higher is high. To put this concept in a different light, we potentially give up short-term gains in exchange for the opportunity to “buy” when market prices are “cheap” and potential returns are high.

Want to invest like Warren? Then follow his rules:

- “Don’t lose money.”

- Refer to Rule #1

- Buy that which is “cheap”

- Sell that which is “dear”

- Hold excessive levels of cash if necessary

- Do not follow the herd

- Have patience, patience and even more patience

- If you want to beat the market, you cannot look like the market

There is nothing “passive” about Warren Buffett or his investment strategy. But there is one lesson in particular that every long-term investor should remember which is the core staple of our investment philosophy and discipline.

“A patient, long-term value investor is the one that sees the big picture and understands stock-market cycles. He or she will likely not fall into the greed or fear trap. Warren Buffett is a brilliant man and has many lessons that investors should emulate. One of his most valued quotes for me is, ‘We (must) simply attempt to be fearful when others are greedy and to be greedy only when others are fearful.’ That is the epitome of breaking away from the herd.” – Michelle Perry Higgins

Disclosure: The information contained in this article should not be construed as financial or investment advice on any subject matter. Real Investment Advice is expressly disclaims all liability in ...

more