Technically Speaking: Bullish Hopes Clash With Bearish Signals

In this past weekend’s missive, I quoted Jeffrey Hirsch, editor of the “StockTrader’s Almanac,” on the entrance of the market into the “seasonally weak” 6-month period for stocks.

“May officially marks the beginning of the ‘Worst Six Months’ for the DJIA and S&P. To wit: ‘Sell in May and go away.’ May has been a tricky month over the years, a well-deserved reputation following the May 6, 2010 ‘flash crash’ and the old ‘May/June disaster area’ from 1965 to 1984. Since 1950, midterm-year Mays rank poorly, #9 DJIA and NASDAQ, #10 S&P 500 and Russell 2000, #8 for Russell 1000. Losses range from 0.1% by Russell 1000 to 1.9% for Russell 2000.

For the near term over the next several weeks the rally may have some legs. But as we get into the summer doldrums and the midterm election campaign battlefront becomes more engaged, we expect the market to soften further during the weakest two-quarter stretch in the 4-year cycle.”

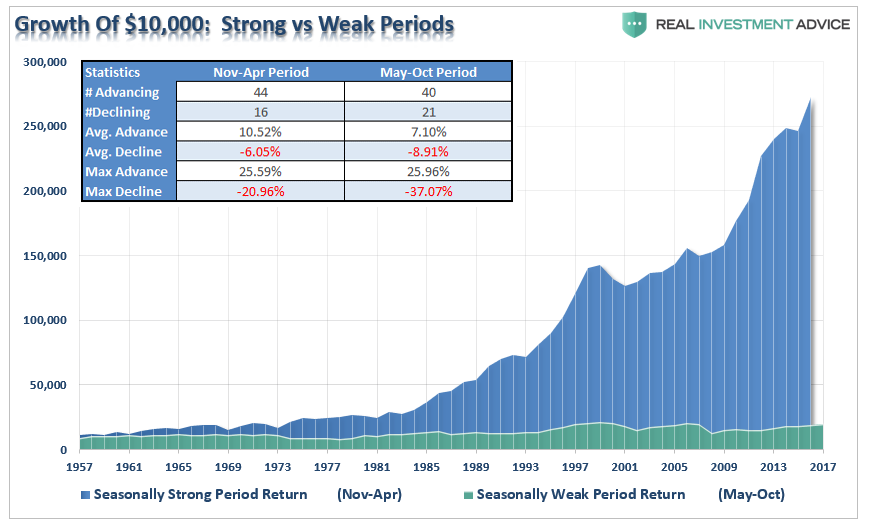

Here is the history of a $10,000 investment.

Despite the weight of evidence to the contrary, the “ever bullishly biased” commentators quickly point out there were many years where the “selling in May” would have left you behind in performance.

But again, the evidence is quite clear.

Nonetheless, as we kick off the month of May, the commentary remains optimistic as earnings have been coming in above already high expectations due to the reduction in corporate tax rates and outstanding float. With the economy still expanding, unemployment rates near lows and consumer confidence near highs – what’s not to love?

From portfolio management viewpoint, it is the disconnect between the “good news” and recent market action that has my full attention.

Warning Signs

While there are many suggesting the recent correction is just a healthy consolidation process within an ongoing “bull market", which so far it has proved to be, there is a difference between today and previous corrections following the “financial crisis.”

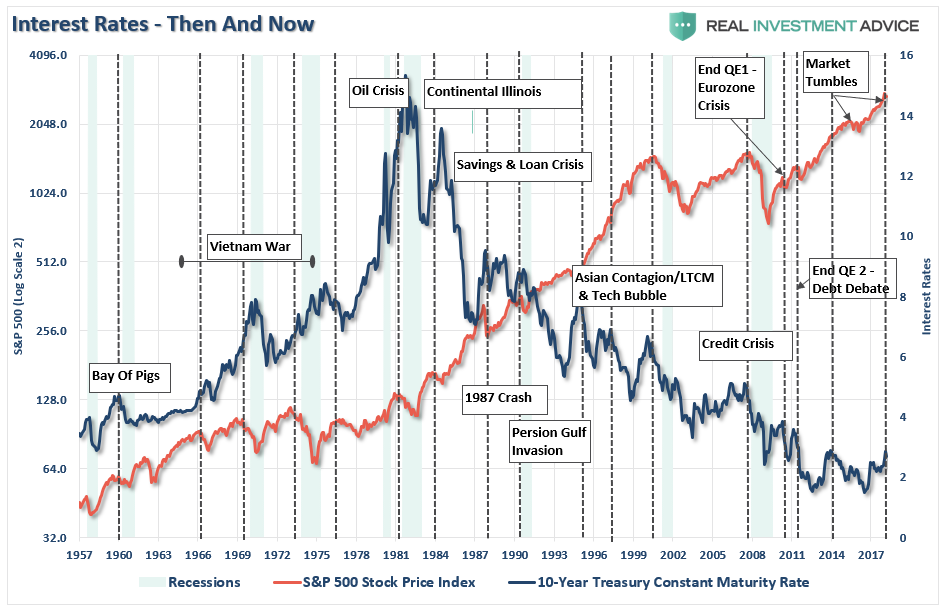

First, The Federal Reserve was still reinvesting proceeds from the bloated $4 Trillion balance sheet, which provided for intermittent pops of liquidity into the financial market. The liquidity is now “running on empty” at a time where interest rates and inflationary pressures are rising.

Second, despite all of the good news from the earnings front, as I stated previously, the surge in the market from July of 2017 had already incorporated those expectations. With current prices expecting things to get even better, such may not be the case as the benefit from tax cuts will begin to fade in Q3 as noted next.

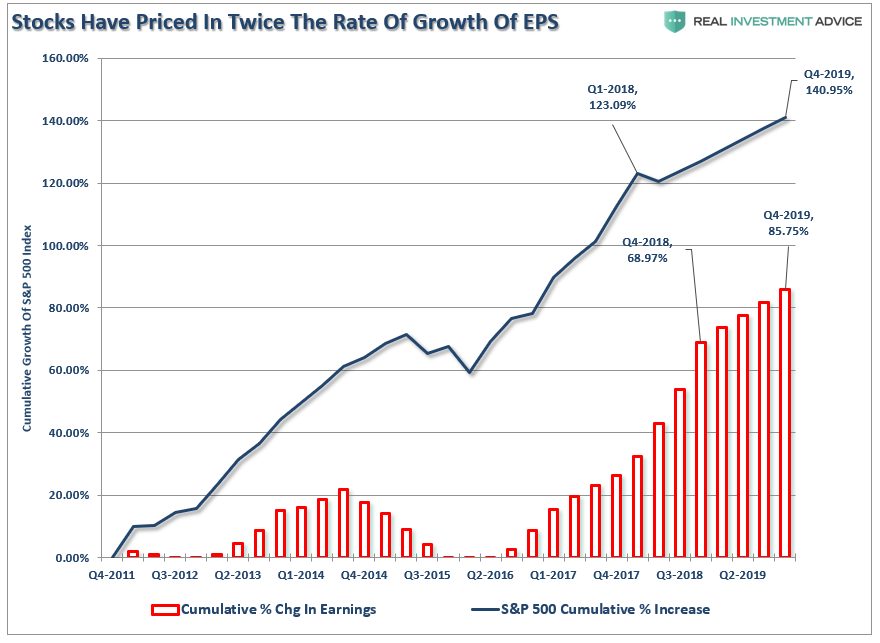

“But even if we give Wall Street the benefit of the doubt, and assume their predictions will be correct for the first time in human history, stock prices have already priced in twice the rate of EPS growth.”

Third, as Doug Kass quoted yesterday from Morgan Stanley:

“Our experience tells us that these leaderless periods typically occur during important transitions in the market. So what is that transition today and how can we harness it to make money? Sticking with our original thesis for 2018, we think the market is digesting the fact that the tax cut last year has created a lower quality increase in US earnings growth that almost guarantees a peak rate of change by 3Q. Furthermore, the second order effects of said tax cuts are not all positive.

Specifically, while an increase in capital spending and wages creates a revenue opportunity for some, it also creates higher costs for most. The net result is lower margins, particularly since the tax benefit is 100 percent ‘below the line.’ Now, with the pricing mechanism for every long duration asset- 10-year Treasury yields-rising beyond 3 percent, we have yet another headwind for risk assets.

Perhaps most importantly for US equity indices, these higher rates are calling into question the leadership of the big tech platform companies-the stocks that may have benefited from the QE era of negative real interest rates more than any area of the market. When capital is free, growth is scarce, and the discount rate is negative in real terms, market participants reward business models that can use that capital to grow. Dividends and returns on that capital today are less important with the discount rate so low. But, with real interest rates rising toward 1 percent, that reward structure may be getting challenged…2018 will mark an important cyclical top for US and global equities, led by a deterioration in credit. Narrowness of breadth and a lack of leadership suggest that this topping process is in the works and will ultimately lead to a fully defensive posture in the market later this year”.

Fourth, rising interest rates are a problem. While in the short-term the economy, and the markets (due to momentum), can SEEM TO DEFY the laws of gravity, ultimately they act as a “brake” on economic activity. This is particularly an issue when tax cuts have boosted bottom line earnings per share for corporations, but higher rates, oil prices, and tariffs will begin to lessen that benefit. This not only applies to corporations, but to already cash-strapped consumers which have seen their tax cut vanish through higher health care, food and energy costs.

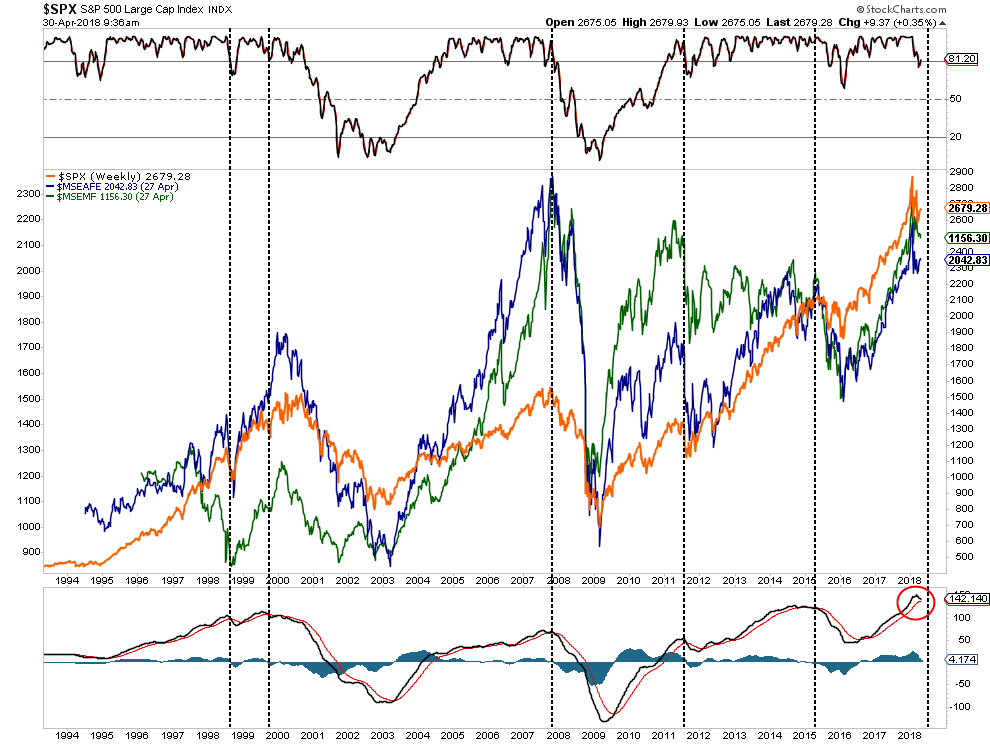

Fifth, It is important to remember that US markets are not an “island". What happens in global financial markets will ultimately impact the U.S. The chart below shows the S&P 500 as compared to the MSCI Emerging Markets and Developed International indices. I have highlighted previous peaks and subsequent bear markets as noted by the sell signals in the lower panel. Currently, the weakness in the international markets is being dismissed by investors, but it most likely should not be.

Lack Of Low Hanging Fruit

As we head into the “seasonally weak” period of the year, it may well provide an opportunity for more seasoned and tactical traders. However, for longer-term investors, like me, there is a lack of “low hanging fruit” to harvest particularly given the current backdrop.

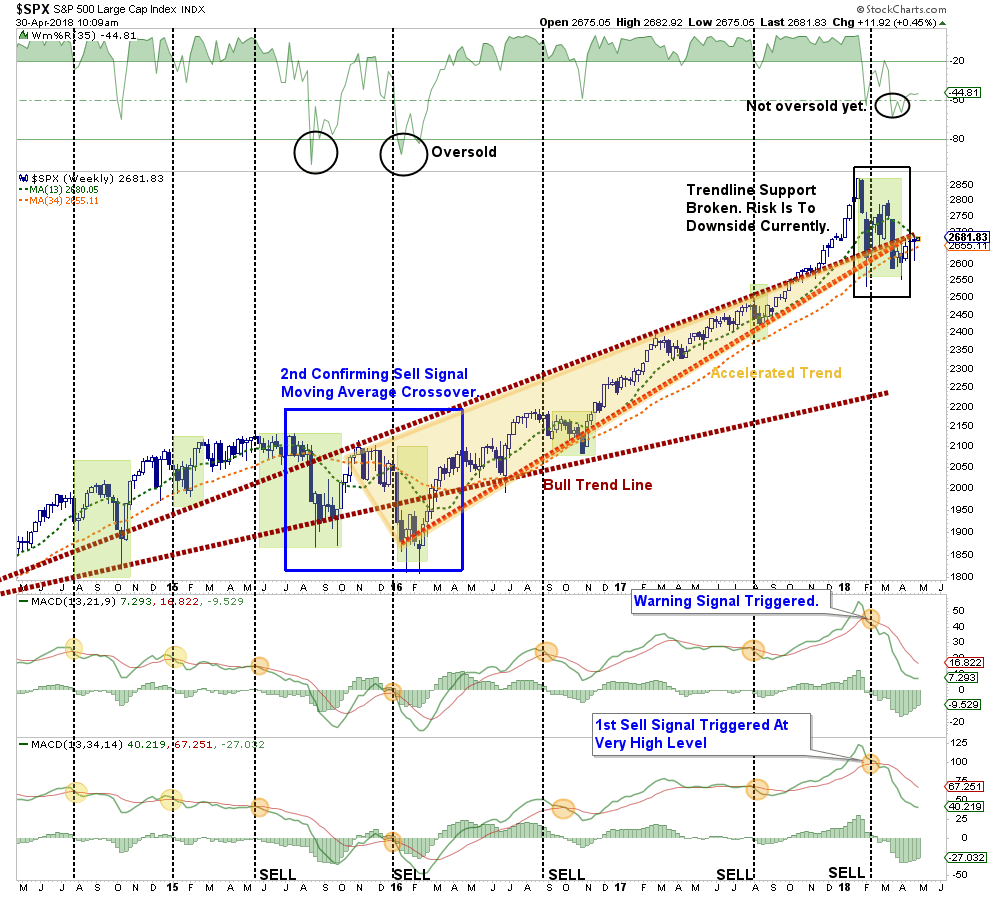

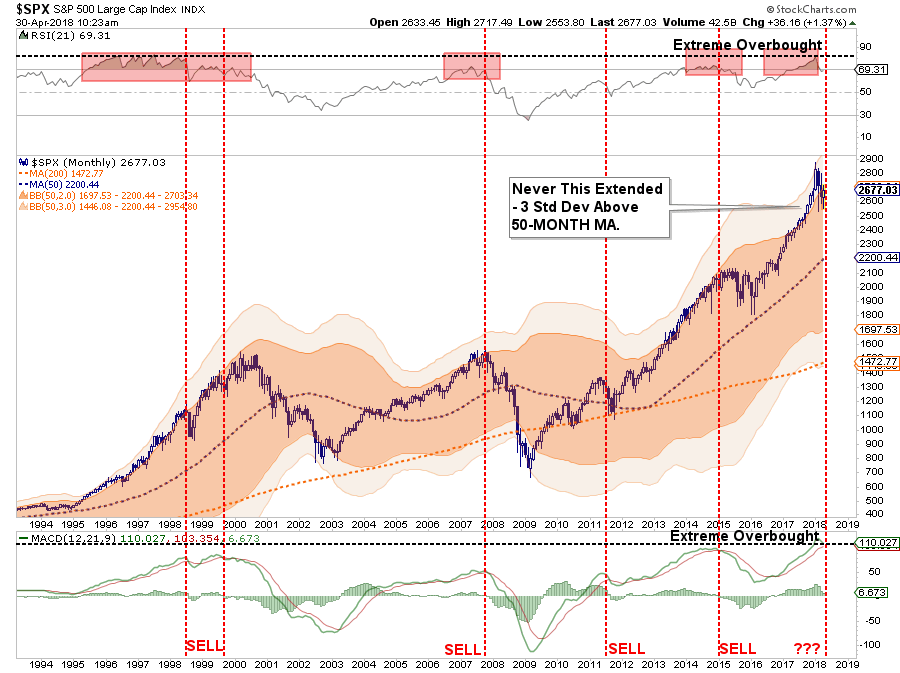

The failure of the markets to rally on Monday continues to reinforce the overhead resistance. As shown below, with confirmed weekly “sell” signals in place, it has historically been a good idea to be a bit more “risk adverse". More importantly, the market currently remains below its previous bullish trend line, and moving averages, which keeps downward pressure on asset prices currently.

With price action still confirming relative weakness, and the recent rally primarily focused in the largest capitalization based companies, the action remains more reminiscent of a market topping process than the beginning of a new leg of the bull market. As shown in the last chart below, the current “topping process”, when combined with underlying “sell signals", is very different than the action witnessed in 2011 or 2015. (I will argue the decline that began in 2015 would have likely been substantially larger had it not been for global coordinated Central Bank interventions.)

While I am not suggesting that the market is on the precipice of the next “financial crisis", I am suggesting that the current market dynamics are not as stable as they were following the correction in 2011 or in 2015. This is particularly the case given the threat of a “tightening” of monetary policy.

The challenge for investors over the next several months will be the navigation of the “seasonally weak” period of the year against a backdrop of warning signals. Importantly, while the “always bullish” media tends to dismiss warning signs as “just being bearish", historically such unheeded warnings have been detrimental. It is my suspicion this time will likely not be much different.

Disclosure: The information contained in this article should not be construed as financial or investment advice on any subject matter. Real Investment Advice is expressly disclaims all liability in ...

more