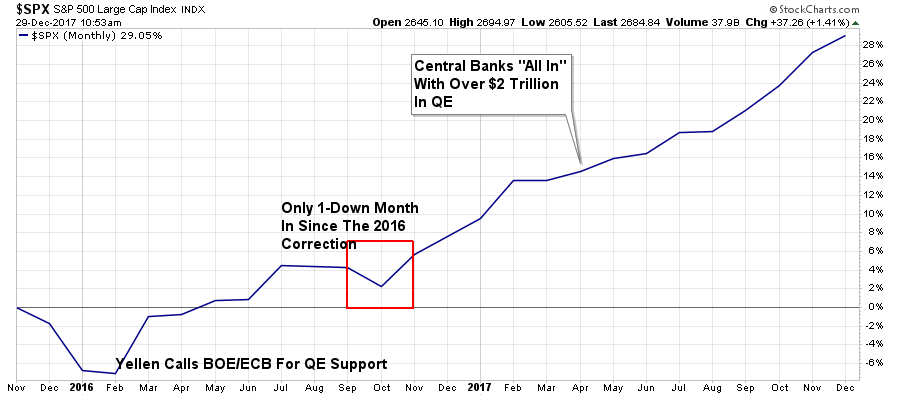

2017 Sets A Record

In just the past year, the markets set a record by going 12 straight months without a loss.

That liquidity driven surge was accompanied by extremely low volatility as noted last week by Dana Lyons:

“Specifically, the average daily closing price of the VIX in 2017 was 11.10 (through 12/26/17). That is the lowest of any year — by more than one and a half points — since the VIX inception in 1986 (by comparison, the ‘average yearly average’ is over 20).”

Of course, with very little volatility, there were very few draw downs along the way as markets continued their advance higher.

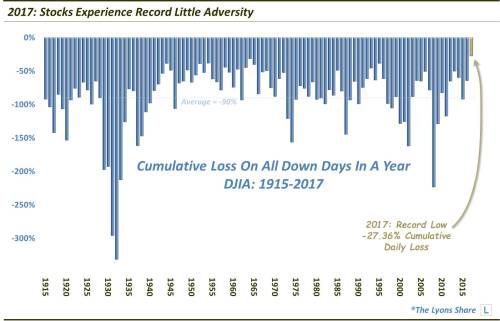

“Accordingly, we took a look at the amount of losses incurred by the stock market during the year as a measure of adversity faced along the way to its solid full-year gains. Specifically, we tabulated the amount of losses incurred during every down day in the market. We used the Dow Jones Industrial Average (DJIA) as it has a longer history than the S&P 500. And based on these calculations, the stock market enjoyed less adversity in 2017 than any other year in history going back over 100 years (our daily DJIA data begins in 1915).”

Not surprisingly, with record low volatility, few losses and a flood of liquidity being pumped into the financial markets – the “bears” finally threw in the towel and capitulated as noted by Sven Henrich(@NorthmanTrader)

“Rydex Bull/Bear ratio at 0.041 the lowest on record. Never have people been more long markets than now.”

Indeed.

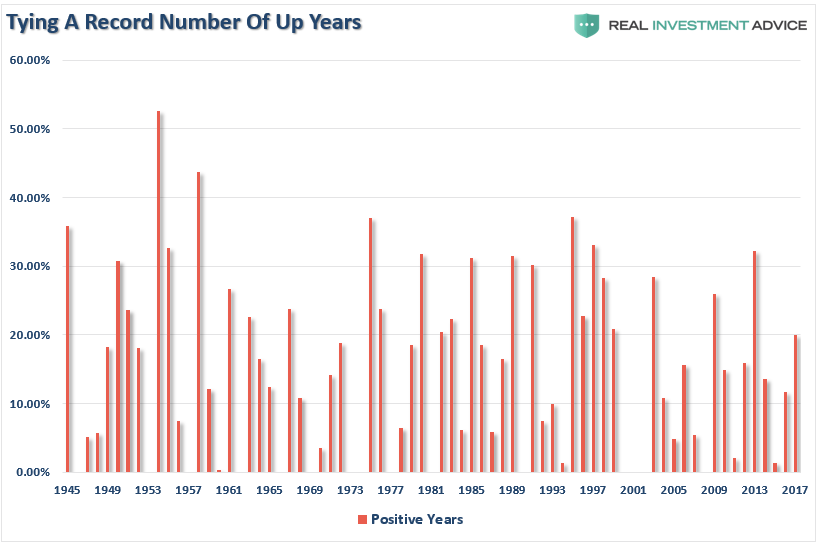

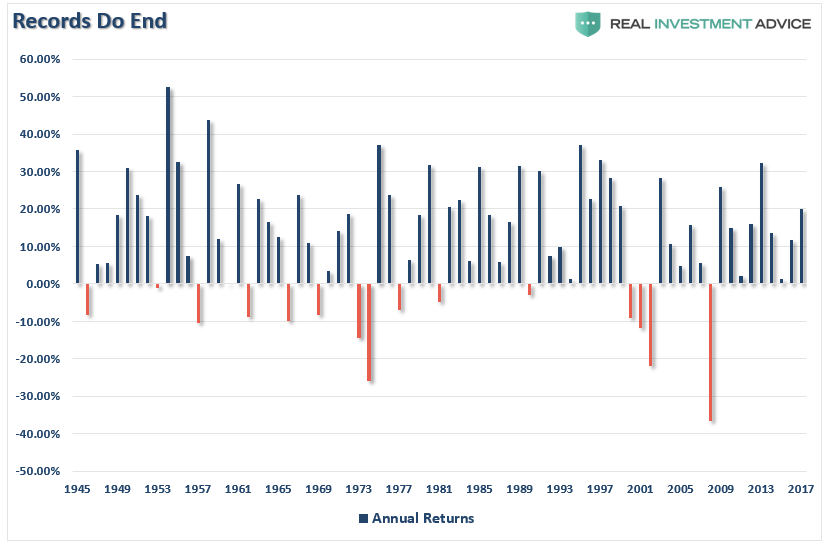

2017 was a record year which tied the 1990’s bull market for the most number of consecutive up years in a row as shown in the chart below.

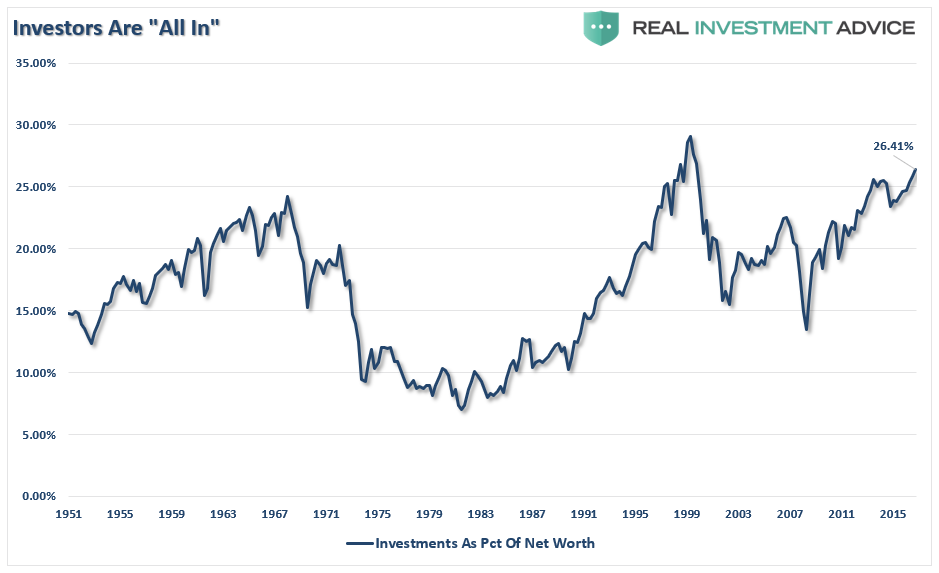

All that exuberance has got Wall Street already prognosticating that next year could be as good, or better, than 2017.

“‘I would expect 2018 to be an almost repeat of 2017,’ said Saut, chief investment strategist at Raymond James. ‘People are still way underinvested. Earnings are starting to come in better than expected. And with the tax reform, and especially the corporate tax cuts, I think earnings are going to continue to surprise on the upside. The professional investors are all in for the most part but the individual investor is not all in.'”

Maybe. But there is more than sufficient evidence that not only professional investors, but individuals, are “all in.”

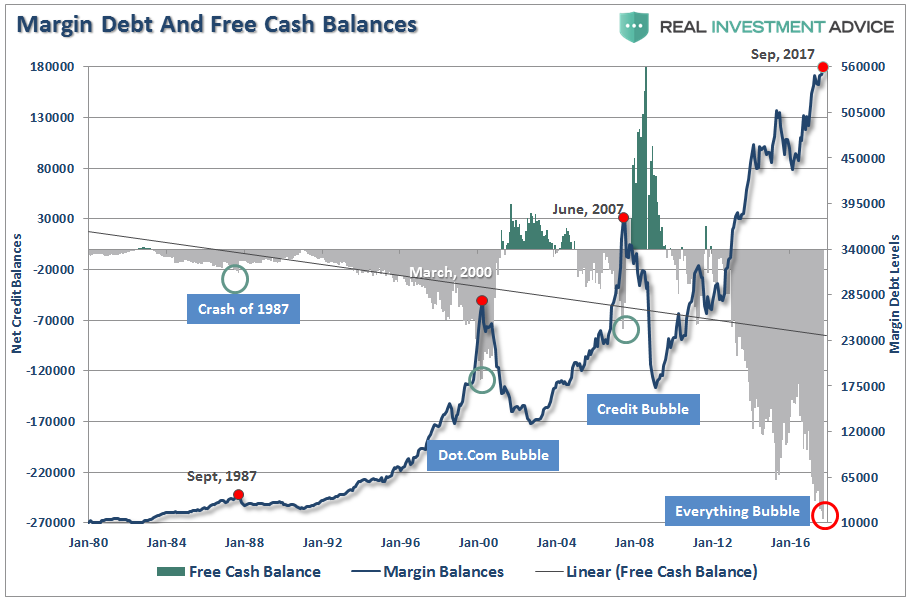

And, not only are they “all in,” they are all in with leverage as I noted previously:

“While investors have been chasing returns in the “can’t lose” market, they have also been piling on leverage in order to increase their return.”

We are currently seeing records every where. Record low volatility, record advances, record leverage, record confidence, etc.

Here is the point I want you to understand.

Records are records for a reason.

Record levels of anything are records for a reason. It is where the point where previous limits were reached. Therefore, when a “record level” is reached it is NOT THE BEGINNING, but rather an indication of the MATURITY of a cycle. While the media has focused on employment, record stock market levels, etc. as a sign of an ongoing economic recovery, history suggests caution.

All good things do eventually come to an end, and generally when they are least expected to do so.

The point here for individuals trying to save for their retirement is that “getting back to even is not an investment strategy.” While the media continues to tout every advance to a previous level as the coming of the next great bull market – keep in mind that this has nothing to do with your money or investing.

So, with this in mind.

Let’s add to our “Rules For The Road” list from last week.

Rules For The Road – Part II

No one knows with certainty what the future holds which is why we must manage portfolio risk accordingly and be prepared to react when conditions change.

While I am often tagged as “bearish” due to my analysis of economic and fundamental data for “what it is” rather than “what I hope it to be,” I am actually neither bullish or bearish. I follow a very simple set of rules which are the core of my portfolio management philosophy which focus on capital preservation and long-term “risk-adjusted” returns.

As such, let me remind you of the 15 Risk Management Rules I have learned over the last 30 years:

- Cut losers short and let winners run. (Be a scale-up buyer into strength.)

- Set goals and be actionable. (Without specific goals, trades become arbitrary and increase overall portfolio risk.)

- Emotionally driven decisions void the investment process. (Buy high/sell low)

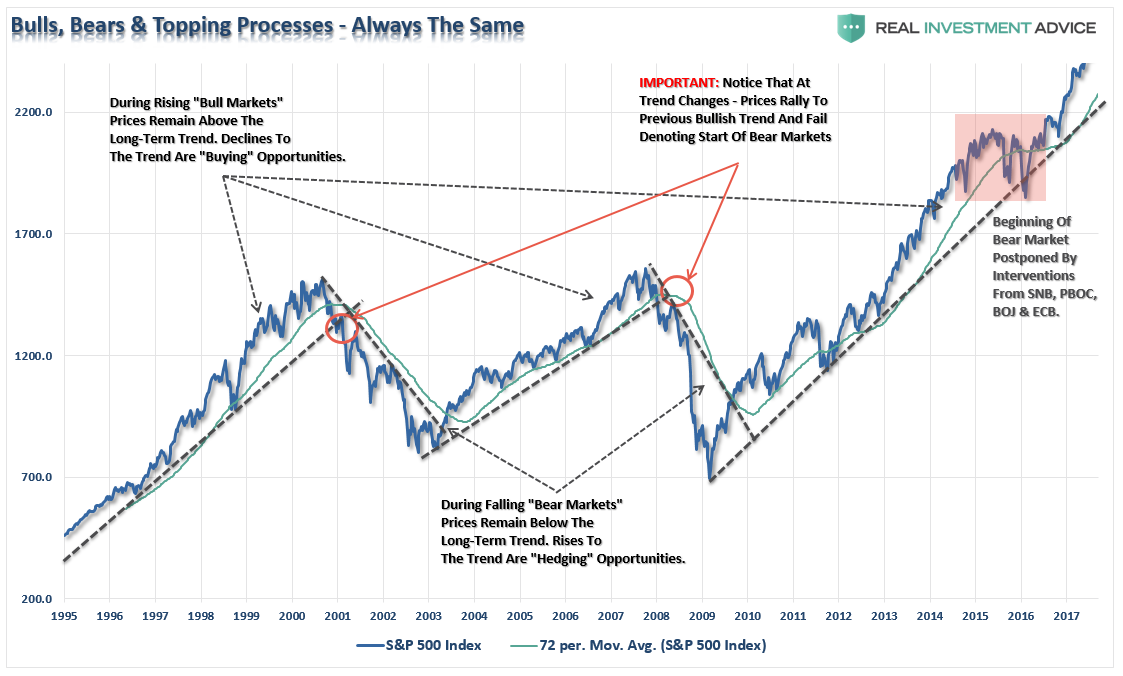

- Follow the trend. (80% of portfolio performance is determined by the long-term, monthly, trend. While a “rising tide lifts all boats,” the opposite is also true.)

- Never let a “trading opportunity” turn into a long-term investment. (Refer to rule #1. All initial purchases are “trades,” until your investment thesis is proved correct.)

- An investment discipline does not work if it is not followed.

- “Losing money” is part of the investment process. (If you are not prepared to take losses when they occur, you should not be investing.)

- The odds of success improve greatly when the fundamental analysis is confirmed by the technical price action. (This applies to both bull and bear markets)

- Never, under any circumstances, add to a losing position. (As Paul Tudor Jones once quipped: “Only losers add to losers.”)

- Market are either “bullish” or “bearish.” During a “bull market” be only long or neutral. During a “bear market”be only neutral or short. (Bull and Bear markets are determined by their long-term trend as shown in the chart below.)

- When markets are trading at, or near, extremes do the opposite of the “herd.”

- Do more of what works and less of what doesn’t. (Traditional rebalancing takes money from winners and adds it to losers. Rebalance by reducing losers and adding to winners.)

- “Buy” and “Sell” signals are only useful if they are implemented. (Managing a portfolio without a “buy/sell” discipline is designed to fail.)

- Strive to be a .700 “at bat” player. (No strategy works 100% of the time. However, being consistent, controlling errors, and capitalizing on opportunity is what wins games.)

- Manage risk and volatility. (Controlling the variables that lead to investment mistakes is what generates returns as a byproduct.)

The current market advance both looks, and feels, like the last leg of a market “melt up” as we previously witnessed at the end of 1999. How long it can last is anyone’s guess. However, importantly, it should be remembered that all good things do come to an end. Sometimes, those endings can be very disastrous to long-term investing objectives. This is why focusing on “risk controls” in the short-term, and avoiding subsequent major draw-downs, the long-term returns tend to take care of themselves.

Everyone approaches money management differently. This is just the way I do it.

All I am suggesting is that you do “something” as the alternative will be much less beneficial.

Portfolio Update

Over the last couple of weeks, I have discussed looking for the right setup to add some hedges to our current long-equity portfolios. That setup occurred last week, and as discussed previously, we have implemented the following:

- Rebalanced overweight positions back to target portfolio weights.

- Added exposure to bonds, utilities and REIT’s bringing allocations up to portfolio weight or slightly overweight.

- Add a tactical trade of a short S&P 500 position to hedge risk.

- Move up stops on all positions to current support levels.

We remain invested but are becoming highly concerned about the underlying risk. Our main goal remains capital preservation.

Disclosure: The information contained in this article should not be construed as financial or investment advice on any subject matter. Streettalk Advisors, LLC expressly disclaims all liability in ...

more