Manufacturing, The Dollar And Implications For Monetary Policy

One of the bits of information in the employment release was a decline in manufacturing employment. When added to declining exports and stagnant manufacturing output growth, the case for near-term monetary policy tightening seems more tenuous to me.

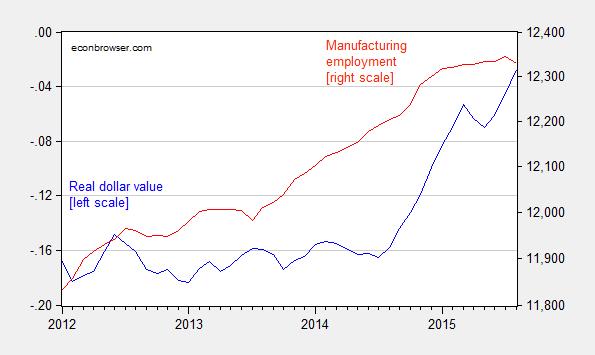

First, manufacturing employment.

Figure 1: Trade weight real value of US dollar against broad basket of currencies, in logs, 1973M03=0 (blue, left scale), and employment in manufacturing, in thousands, seasonally adjusted (red, right logarithmic scale). Source: Federal Reserve Board and BLS via St. Louis Fed FRED, and author’s calculations.

While the decline in August employment might very well be erased in the next revision, what can be said is that manufacturing employment has flattened out several months after the dollar’s ascent began.

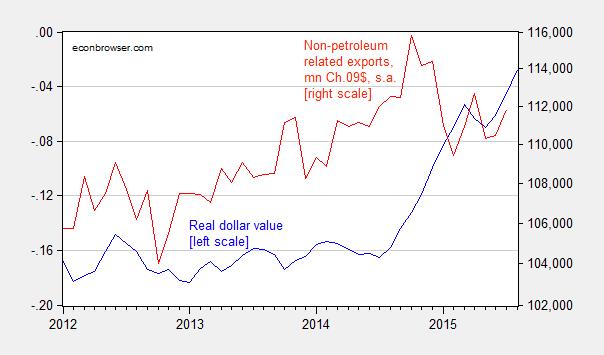

Next up – exports. Thursday’s trade release provided some good news, with the trade deficit shrinking and exports inching up. But what about exports?

Figure 2: Trade weight real value of US dollar against broad basket of currencies, in logs, 1973M03=0 (blue, left scale), and exports of non-petroleum related goods, in millions of Ch.2009$, seasonally adjusted (red, right logarithmic scale). Source: Federal Reserve Board and BEA/Census via St. Louis Fed FRED, and author’s calculations.

Nonetheless, non-petroleum related exports are down slightly relative to a year ago, and down noticeably relative to the 2014M10 peak (since the left scale is log, but with original data reported — as some readers have asked for given their befuddlement with logs — one can’t read directly off the graph the percent decline; it is 3.5% in log terms).

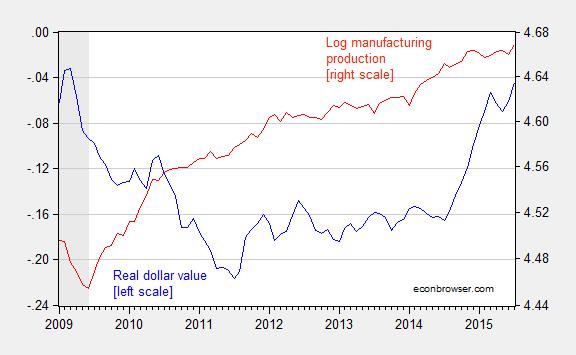

Manufacturing output (a proxy for tradables) ticked up for the last reported month.

Figure 3: Trade weight real value of US dollar against broad basket of currencies, in logs, 1973M03=0 (blue, left scale), and manufacturing output, seasonally adjusted (red, right scale). Source: Federal Reserve Board and BEA/Census via St. Louis Fed FRED, and author’s calculations.

However, the deceleration in manufacturing output growth is marked over the past year. This is the best high frequency indicator for the impact on the tradables sector of the dollar, given the trend decline in manufacturing employment.

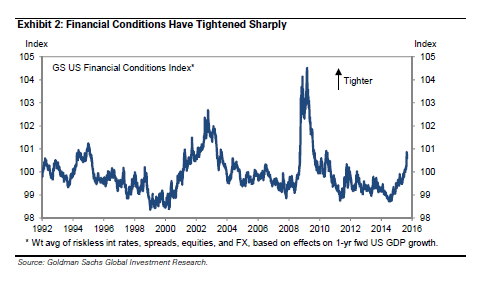

All the foregoing suggest to me we should be wary of tightening, given the tightening has already occurred, based on indicators of financial indicators. Consider the Goldman Sachs indicator, as of yesterday.

Source: Goldman Sachs, “US Economics Analyst: 15/36 – The Drag from China: Many Channels, Limited Impact” (Stehn/Hatzius) [not online].

Disclosure: None.